Undiscovered Gems in the US Market for May 2026

Ategrity Specialty Insurance Company Holdings ASIC | 0.00 |

The United States market has shown robust performance, with a 1.5% increase over the last week and a remarkable 26% climb in the past year, supported by expected annual earnings growth of 17%. In such a thriving environment, identifying stocks that are not only poised for growth but also remain under the radar can offer unique opportunities for investors seeking to diversify their portfolios.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 68.27% | 1.25% | -3.09% | ★★★★★★ |

| Cashmere Valley Bank | 31.63% | 5.07% | 1.43% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 12.65% | 41.20% | ★★★★★★ |

| SIFCO Industries | 12.27% | -4.21% | -2.87% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.26% | 11.00% | ★★★★★★ |

| Affinity Bancshares | 41.71% | 1.36% | -0.22% | ★★★★★★ |

| Seneca Foods | 38.64% | 2.39% | -18.65% | ★★★★★☆ |

| Union Bankshares | 406.25% | 1.42% | -7.24% | ★★★★☆☆ |

| Oxford Bank | 12.42% | 13.91% | 2.78% | ★★★★☆☆ |

| High Templar Tech | 13.55% | -66.76% | -26.62% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

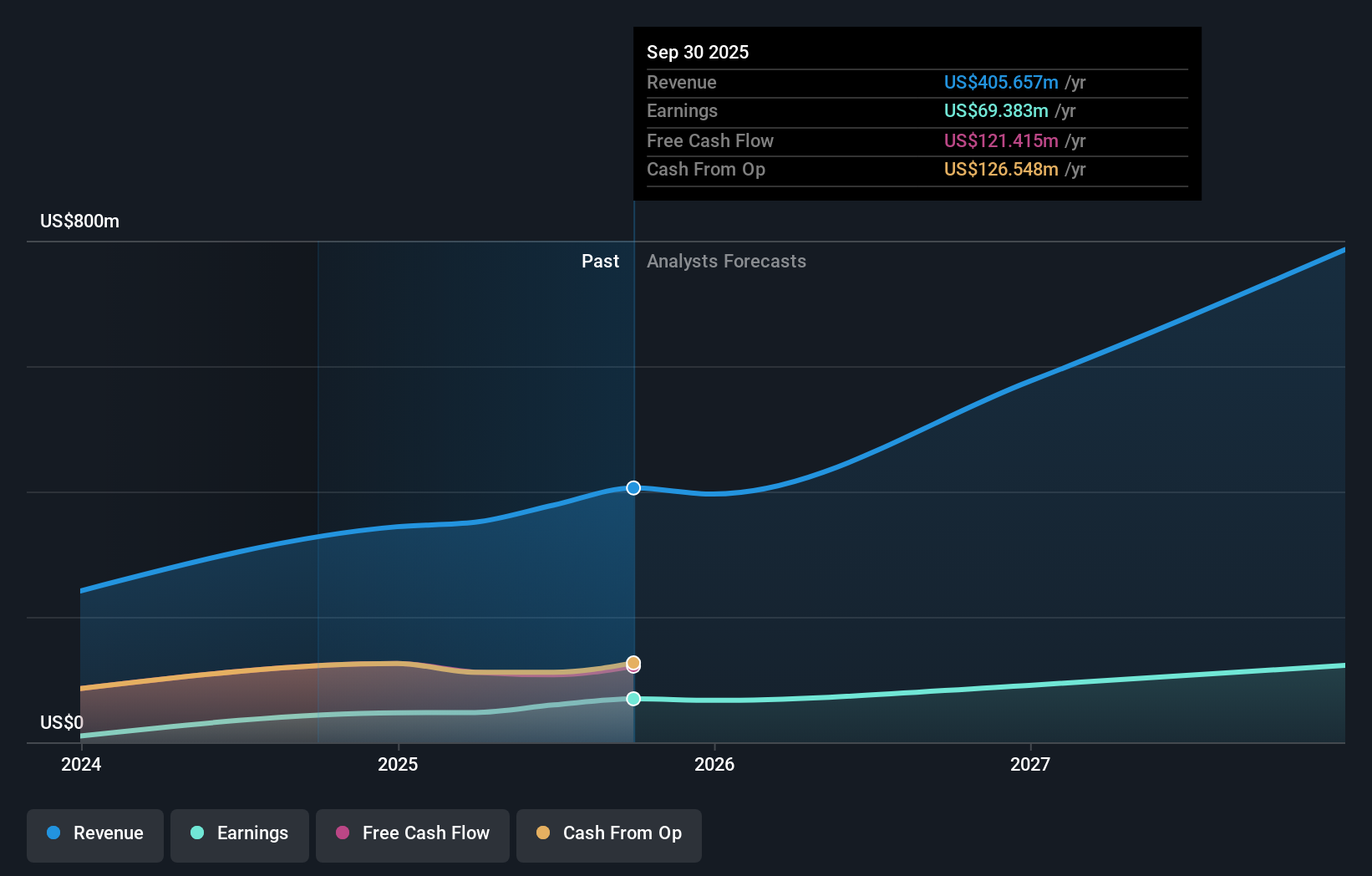

Cricut (CRCT)

Simply Wall St Value Rating: ★★★★★★

Overview: Cricut, Inc. designs, markets, and distributes a creativity platform for crafting professional-looking handmade goods across various global regions, with a market cap of $915.16 million.

Operations: Cricut generates revenue primarily from its platform and products, with the latter contributing $373.44 million and the former $332.18 million.

Cricut, a nimble player in the crafting industry, seems to be trading at a notable 52.5% below its estimated fair value, offering potential upside for investors. Despite being debt-free and boasting high-quality earnings, Cricut has faced challenges with earnings declining by 23% annually over the past five years. However, recent initiatives like AI Project Designer and new cutting machines could bolster growth prospects. The company reported Q1 2026 revenue of US$159 million and net income of US$20 million while repurchasing shares worth US$12 million this year, signaling confidence in its future trajectory.

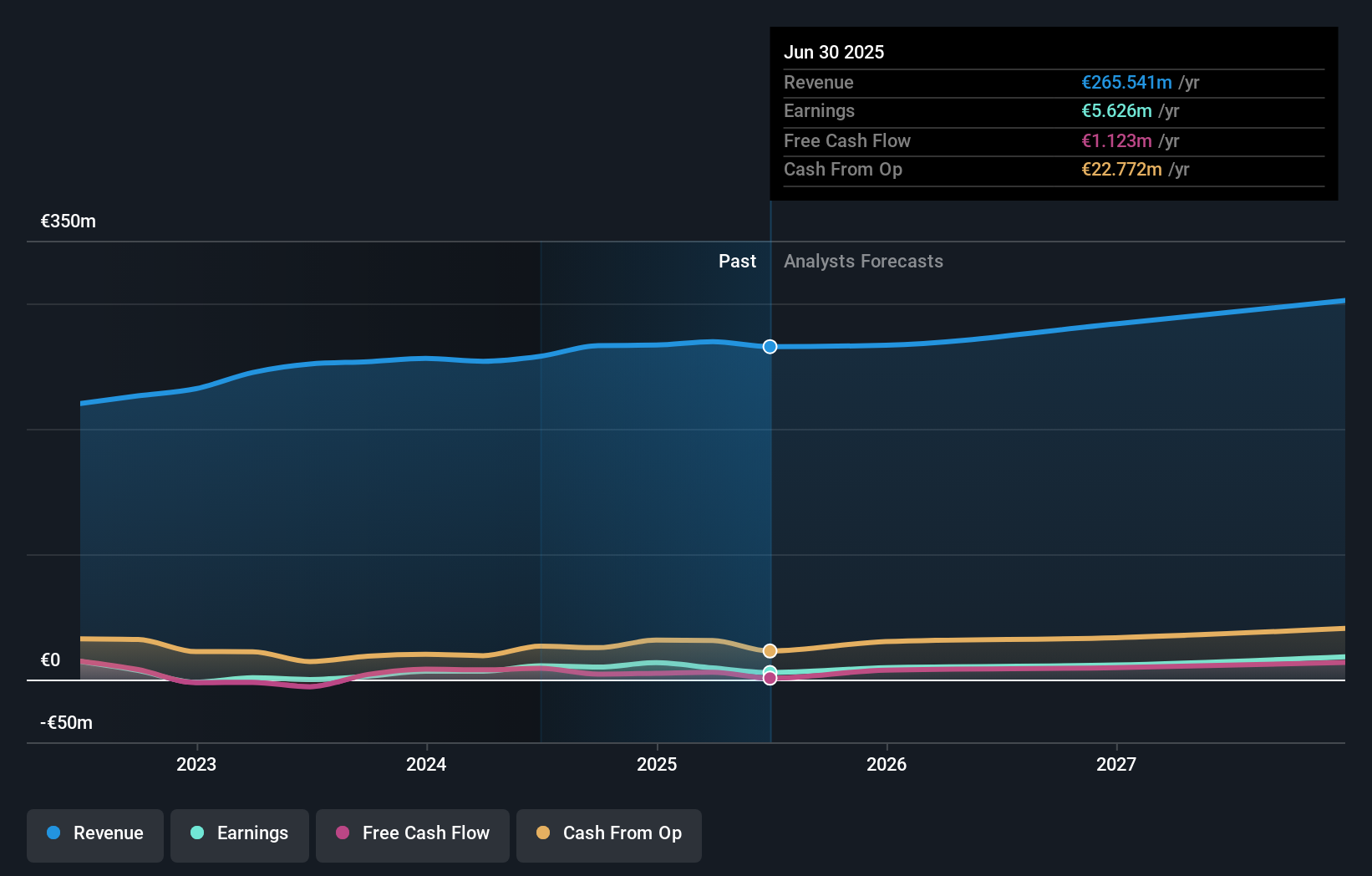

Materialise (MTLS)

Simply Wall St Value Rating: ★★★★★★

Overview: Materialise NV offers additive manufacturing and medical software tools, along with 3D printing services across various regions including the Americas, Europe, Africa, and the Asia-Pacific, with a market capitalization of approximately $319.66 million.

Operations: Materialise generates revenue primarily from its additive manufacturing and medical software tools, as well as 3D printing services. The company's net profit margin is reported at 5.6%.

Materialise, a notable player in the 3D printing sector, has shown resilience with high-quality earnings and a significant reduction in its debt to equity ratio from 77.3% to 21.1% over five years. Despite not outpacing the software industry last year, it achieved an impressive annual earnings growth of 15.1% over five years and is trading at nearly 29% below its estimated fair value. Recent financials reveal net income of €1.82 million for Q1 2026 compared to a loss last year, with EPS improving from a negative €0.01 to €0.03, while actively repurchasing shares worth €2.46 million this year suggests confidence in future prospects.

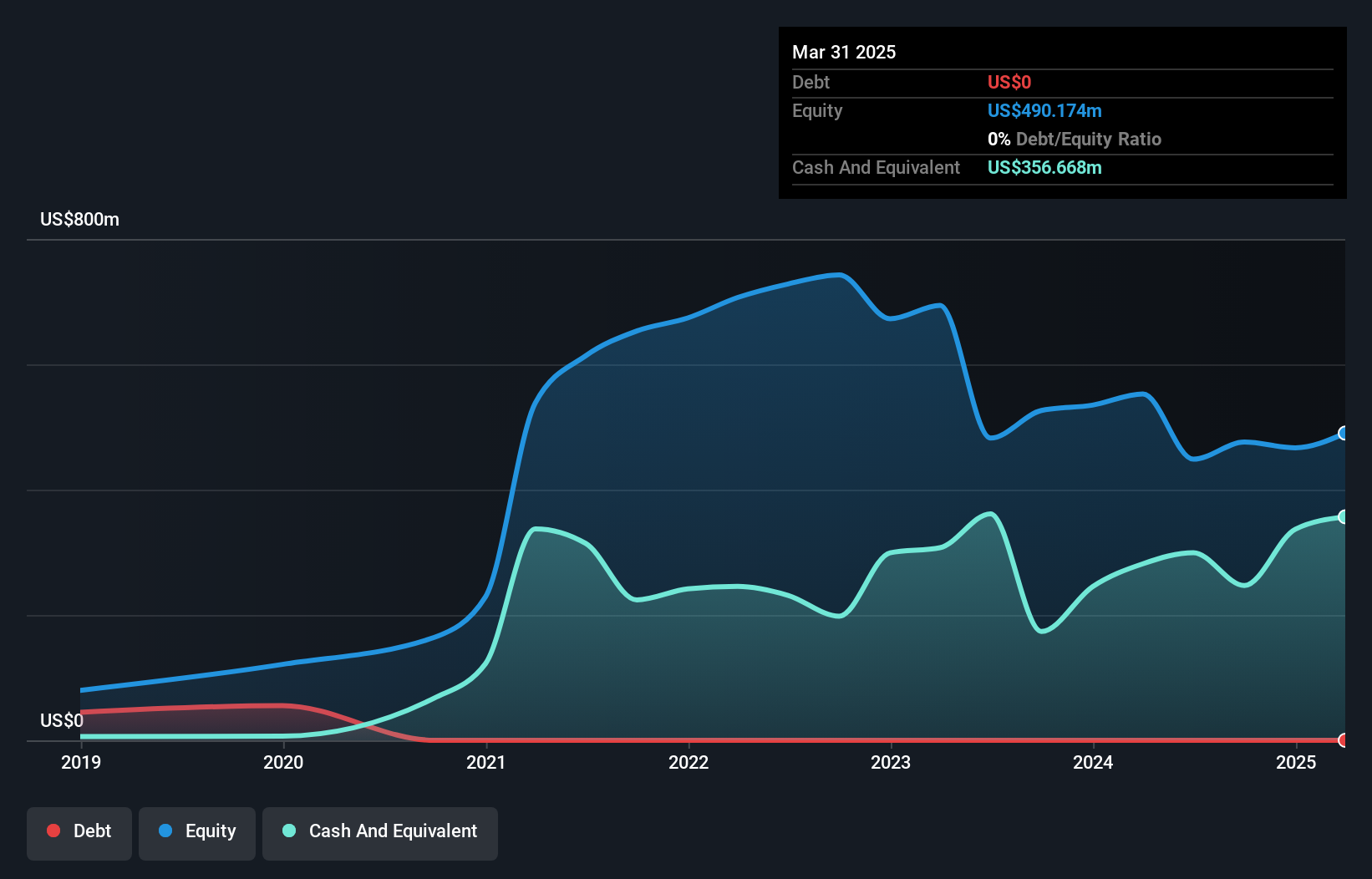

Ategrity Specialty Insurance Company Holdings (ASIC)

Simply Wall St Value Rating: ★★★★★★

Overview: Ategrity Specialty Insurance Company Holdings, with a market cap of $929.43 million, operates through its subsidiaries to offer excess and surplus lines insurance and reinsurance products tailored for small and medium-sized businesses in the United States.

Operations: ASIC generates revenue primarily from its insurance business, totaling $470.18 million. The company's net profit margin shows a notable trend, reflecting the efficiency of its operations in managing costs relative to revenue.

Ategrity Specialty Insurance Company Holdings, a smaller player in the insurance sector, has shown impressive financial performance recently. The company reported a significant rise in revenue to US$128.96 million for Q1 2026 from US$83.12 million the previous year, with net income climbing to US$25.47 million from US$8.46 million. Basic earnings per share increased to US$0.53 from US$0.2, highlighting robust growth momentum. Ategrity operates debt-free and is trading at 51% below its estimated fair value, suggesting potential undervaluation compared to peers and industry standards while maintaining high-quality earnings and strong free cash flow generation capabilities.

Taking Advantage

- Take a closer look at our US Undiscovered Gems With Strong Fundamentals list of 340 companies by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.