UniFirst (UNF) Could Be 3% Undervalued As Earnings And Buyback Completion Draw Focus

UniFirst Corporation UNF | 0.00 |

UniFirst earnings event and completed buyback draw fresh attention

UniFirst (UNF) is back in focus after reporting third quarter and nine month 2026 results, along with an update that it has completed a previously announced share repurchase program.

The company reported third quarter sales of $634.4 million and net income of $19.92 million, with diluted earnings per share from continuing operations of $1.09. For the first nine months of the fiscal year, sales were $1,878.23 million, net income was $74.76 million and diluted earnings per share from continuing operations were $4.11.

Alongside earnings, UniFirst confirmed that between March 1 and May 30, 2026 it repurchased no additional shares, but has fully completed the buyback announced in April 2025, retiring 529,910 shares for a total spend of $91.49 million.

At a share price of $271.78, UniFirst has seen positive momentum build recently, with a 30 day share price return of 2.62%, a year to date share price return of 40.38%, and a 1 year total shareholder return of 53.64%.

If UniFirst’s recent move has you thinking about what else is working in the market, this is a good moment to broaden your search with 18 top founder-led companies

UniFirst looks like a solid uniform and services business, and the stock has just put up a strong run, so the next step is clear: are you paying a fair price for that quality or stretching at today’s level?

Most Popular Narrative: 2.6% Undervalued

On the most followed view of UniFirst, a fair value of $279 sits slightly above the recent $271.78 close, putting the current price almost in line with that narrative.

Significant investments in technology, specifically an ERP system, are anticipated to enhance efficiency, leading to improved profitability and reduced operational costs once fully implemented, which should impact net margins positively in the long run.

Read the complete narrative. Read the complete narrative.

Want to understand why a modest revenue outlook still supports this fair value for UniFirst? The narrative leans heavily on earnings quality, margin rebuilding and a premium future profit multiple tied to those assumptions. The tension between current profitability and longer term targets is where the story gets interesting.

Result: Fair Value of $279 (UNDERVALUED)

However, UniFirst’s narrative still leans on ERP benefits that are not expected until fiscal 2027. At the same time, higher health care costs could pressure margins sooner.

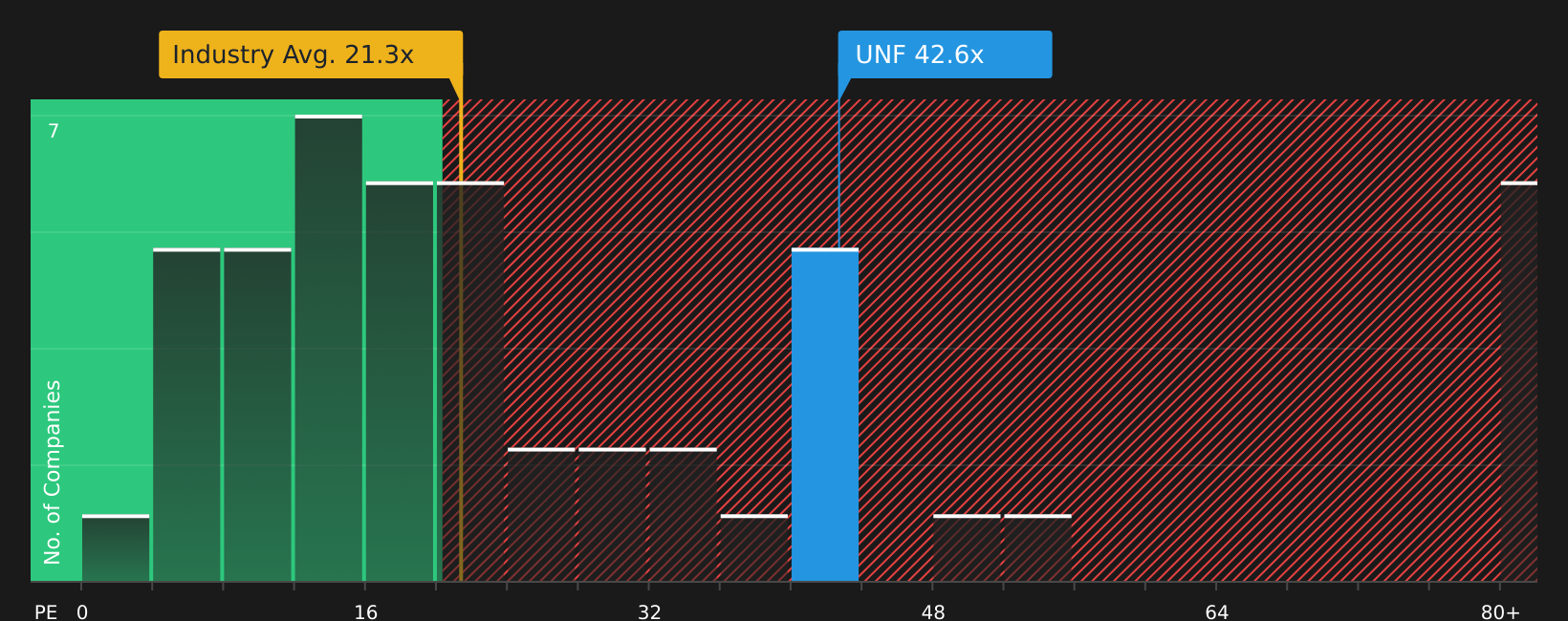

Another View: UniFirst looks expensive on earnings multiples

That 2.6% implied upside for UniFirst contrasts sharply with how the stock looks on simple earnings ratios. At a P/E of 42.4x versus a fair ratio of 21.6x, an industry average of 21.2x and a peer average of 32.6x, the market is paying a clear premium that raises valuation risk.

If you rely more on simple earnings ratios than on narratives, the question becomes whether UniFirst’s quality and merger story are enough to justify paying roughly double that fair ratio, or whether expectations have already run too far ahead of themselves.

Next Steps

With UniFirst’s story pulling in different directions, this is a good time to move quickly and test the headlines against the underlying data for yourself. To see what the optimism is about, take a closer look at the 1 key reward.

Looking for more investment ideas beyond UniFirst?

If UniFirst has sharpened your focus on quality, do not stop there. Broaden your watchlist now so you are not the one catching up later.

- Target potential mispricing opportunities by scanning 45 high quality undervalued stocks that combine solid fundamentals with valuations that may not fully reflect their financial profile.

- Strengthen your income stream by reviewing 9 dividend fortresses that pair higher yields with balance sheets designed to support ongoing payouts.

- Prioritise resilience by checking 79 resilient stocks with low risk scores that score well on stability and financial risk metrics for a smoother ride through market swings.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.