UniFirst (UNF) Stock Could Be 6.5% Undervalued on Its Margin Improvement Narrative

UniFirst Corporation UNF | 0.00 |

UniFirst (UNF) is back in focus after a recent move in its share price, with the stock closing at $261. Investors are weighing this level against the company’s latest business and return metrics.

While UniFirst’s share price slipped 5.3% over the past week and edged down 1.2% over the past month, its year to date share price return of 34.8% and 1 year total shareholder return of 43.4% point to momentum that has been building over a longer horizon.

If UniFirst’s run has you thinking about what else is working in the market, it could be a good time to broaden your search with 20 top founder-led companies.

With UniFirst now at $261 and sitting closer to analysts’ stated price target of $279, the key question is whether current earnings and cash flows justify this level, or if markets are already pricing in future growth.

Most Popular Narrative: 6.5% Undervalued

With UniFirst shares at $261 against a narrative fair value of $279, the current price sits slightly below what this widely followed model implies.

Significant investments in technology, specifically an ERP system, are anticipated to enhance efficiency, leading to improved profitability and reduced operational costs once fully implemented. This is expected to impact net margins positively in the long run. Expansion of the distribution center in Owensboro, Kentucky, is expected to improve speed and efficiency in direct sales of uniforms, potentially influencing revenue through enhanced operational capacity.

Want to understand why a modest revenue outlook still supports a higher value for UniFirst? The narrative focuses on potential changes in future margins, capital efficiency and a richer earnings multiple. The full story is in how these pieces fit together over time.

Result: Fair Value of $279 (UNDERVALUED)

However, UniFirst’s story can change quickly if weaker customer demand persists or if higher health care costs keep eating into the hoped for margin gains.

Another View on UniFirst’s Valuation

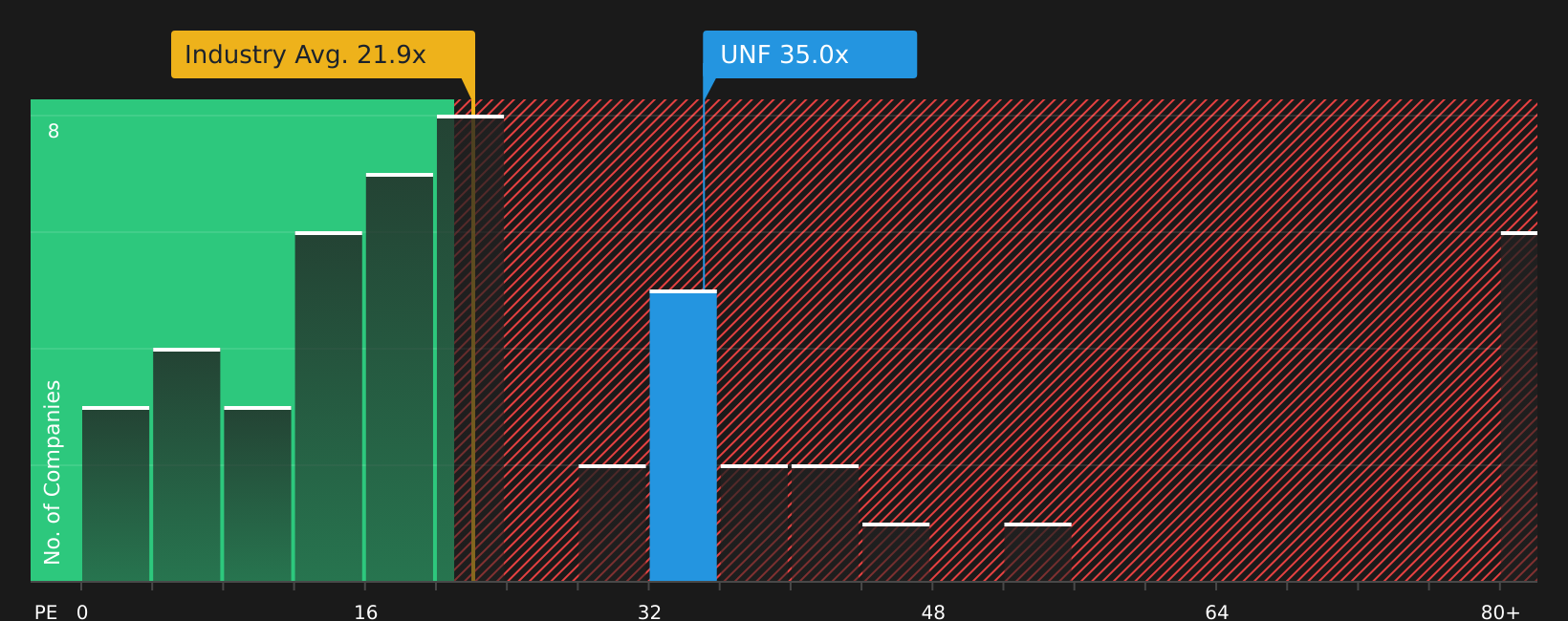

While the narrative fair value suggests UniFirst might be 6.5% undervalued at $261 versus $279, the market’s P/E of 34.8x paints a tighter picture. That multiple sits above peers at 32.8x and well above a fair ratio of 18x, which points to meaningful valuation risk if sentiment cools.

For investors comparing UniFirst with other companies on this basis, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Curious whether the tone of this UniFirst update matches your own read of the numbers and risks? Move quickly, review the data for yourself, then weigh it against the company’s potential strengths in our 1 key reward

Looking for more investment ideas beyond UniFirst?

If UniFirst has sharpened your focus on valuation and quality, do not stop here. Use targeted stock lists to pressure test your next moves before the market does.

- Target potential bargains by scanning companies that combine quality with attractive pricing using the 45 high quality undervalued stocks.

- Prioritise resilience by reviewing companies that score well on financial strength through the solid balance sheet and fundamentals stocks screener (48 results).

- Hunt for future standouts by checking a screener containing 20 high quality undiscovered gems before everyone else is talking about them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.