uniQure (QURE) Stock Could Be 12% Undervalued After FDA Backs AMT 130 Filing Path

uniQure N.V. QURE | 0.00 |

uniQure (NasdaqGS:QURE) is back in focus after the FDA said three year Phase I/II data for its Huntington’s disease gene therapy, AMT-130, can underpin a Biologics License Application for accelerated approval.

The FDA update has arrived after a sharp reset in sentiment around uniQure, with the stock posting a 90 day share price return of 187.69% and a 1 year total shareholder return of 225.76%. This points to strong positive momentum from a much lower base.

If you are looking beyond uniQure for other high impact health related opportunities, this could be a useful moment to check out 40 healthcare AI stocks.

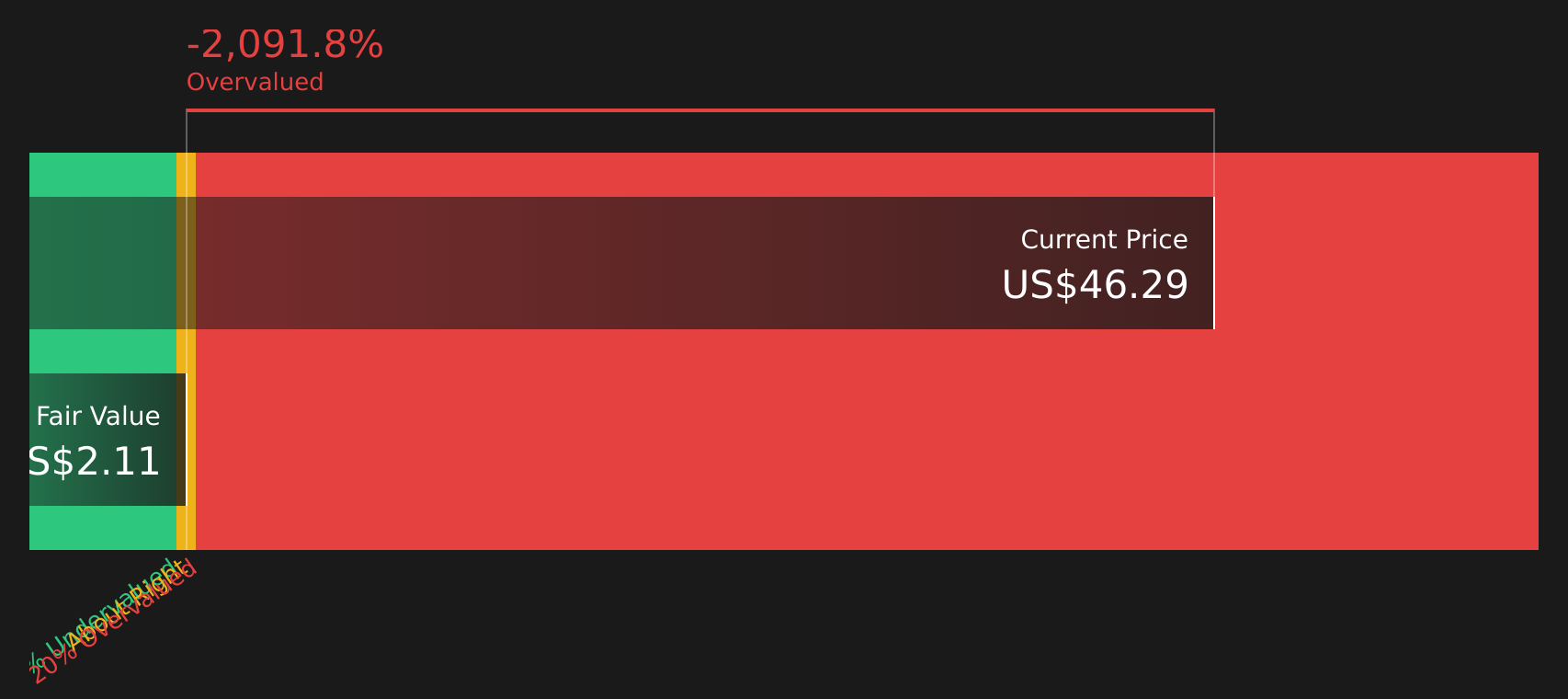

After a move like that, the key question for investors is whether uniQure’s current US$46.29 share price and roughly US$2.9b market cap still leave room for upside, or whether the market is already pricing in future growth and regulatory success.

Most Popular Narrative: 12% Undervalued

On the most followed narrative, uniQure’s estimated fair value of $52.56 sits above the last close at $46.29, which puts a spotlight on what is driving that gap.

The potential accelerated approval for AMT-130 in treating Huntington's disease could significantly boost future revenues as it would be one of the first disease-modifying treatments available for this condition.

Expansion of the clinical pipeline with new studies in refractory temporal lobe epilepsy, Fabry disease, and SOD1-ALS could lead to additional revenue streams if these treatments are successful and commercialized.

Want to see what justifies a higher fair value for uniQure? The narrative leans heavily on steep revenue growth, rising margins and a rich future earnings multiple.

Based on this narrative, analysts fold together rapid top line growth assumptions, unchanged loss making status over the next few years, and a high future P/E multiple applied to potential 2029 earnings. They also apply a 7.4% discount rate to bring those projected cash flows and valuation metrics back to today, which is how they arrive at a fair value that is above the current share price.

Result: Fair Value of $52.56 (UNDERVALUED)

However, the uniQure story still leans heavily on AMT-130 regulatory outcomes and on reversing recent revenue pressure, so setbacks on either front could quickly challenge this upbeat narrative.

Another Take On uniQure’s Valuation

The 12% undervalued fair value hinges on long term growth and high future earnings multiples, but the SWS DCF model tells a very different story. On that view, QURE is trading far above estimated future cash flows. This raises the question of how much regulatory and revenue risk you are really paying for.

Next Steps

Given the mix of optimism and concern around uniQure, this is a moment to move fast and stress test the assumptions that matter most. To review both the potential benefits and key risks in one place, start with the 1 key reward and 4 important warning signs.

Looking for more investment ideas beyond uniQure?

If you want a broader view than uniQure alone, this is a good time to scan the market for other stocks that match your risk and return preferences.

- Target dependable compounding by reviewing companies with strong cash generation and appealing valuations through the 45 high quality undervalued stocks.

- Prioritize resilience by focusing on companies with sturdy finances and prudent leverage using the solid balance sheet and fundamentals stocks screener (48 results).

- Spot potential early movers by scanning the screener containing 19 high quality undiscovered gems before they attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.