United Parcel Service (UPS) Stock After Mixed Multi‑Year Returns Is There An Opportunity Now

United Parcel Service, Inc. Class B UPS | 0.00 |

- If you are wondering whether United Parcel Service stock still offers value at its current price, this article walks through what the numbers are really saying about it.

- United Parcel Service recently closed at US$106.14, with returns of 1.0% over the last week, 5.1% over the last month and year to date, and 14.2% over the past year. The 3 year and 5 year returns show declines of 28.8% and 36.0% respectively.

- These mixed returns have kept interest in United Parcel Service alive as investors reassess how the stock fits into their portfolios. That makes it especially important to set recent price moves against a consistent valuation framework rather than short term sentiment.

- United Parcel Service currently scores 4 out of 6 on Simply Wall St's valuation checks. The next sections break down what that means across different valuation methods, before finishing with a way to interpret valuation that can be even more helpful than the raw numbers alone.

Approach 1: United Parcel Service Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what United Parcel Service stock could be worth by projecting future cash flows and discounting them back to today. It is essentially asking what those future dollars are worth in present terms.

For United Parcel Service, the latest twelve month Free Cash Flow is reported at about $4.0b. Analysts provide Free Cash Flow estimates out to 2029, with Simply Wall St extending those projections further using its 2 Stage Free Cash Flow to Equity model. By 2029, projected Free Cash Flow is $7.5b, with a series of yearly projections in between and beyond that are converted back into today’s dollars using a discount rate.

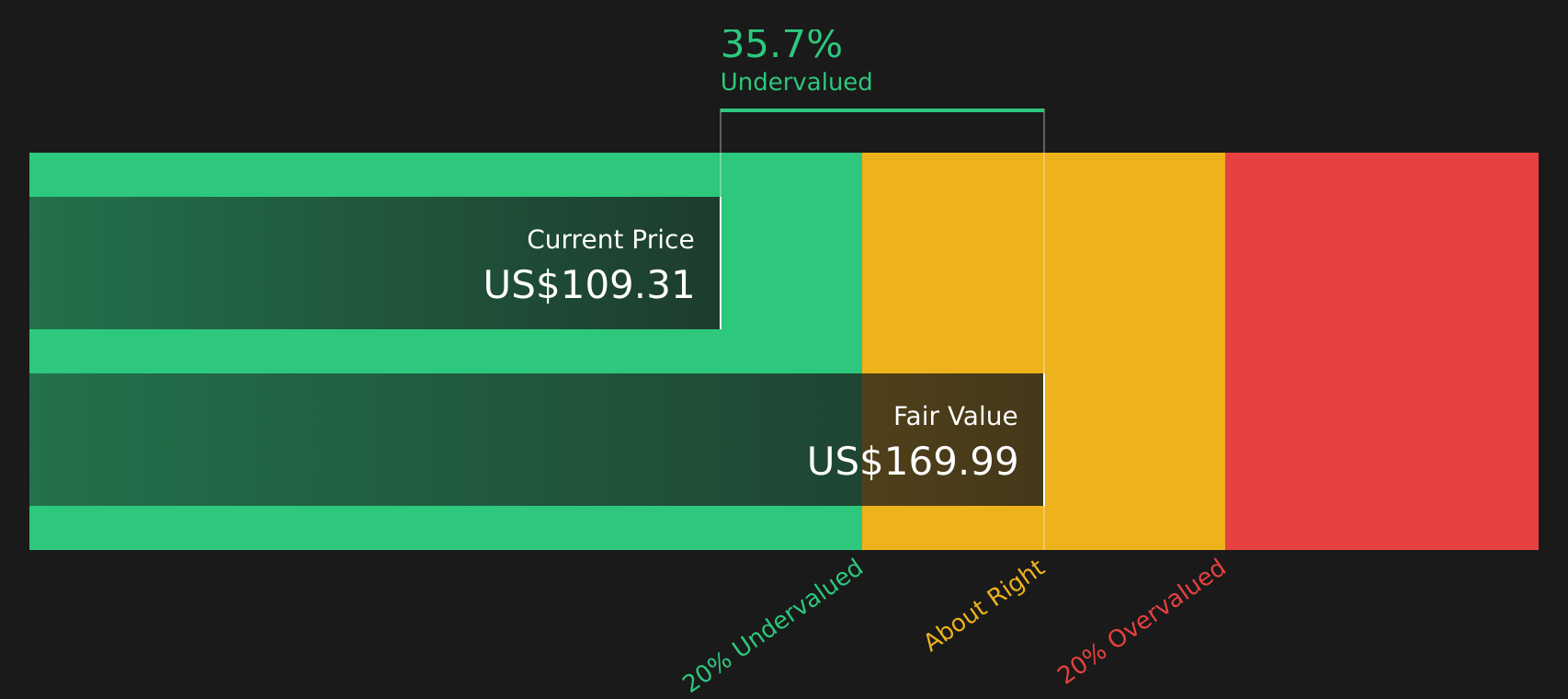

When all those discounted cash flows are added up and divided by the number of shares, the DCF model arrives at an estimated intrinsic value of about $169.93 per share. Against the recent share price of $106.14, this implies the stock is around 37.5% undervalued according to this method.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests United Parcel Service is undervalued by 37.5%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Approach 2: United Parcel Service Price vs Earnings

For profitable companies like United Parcel Service, the P/E ratio is a widely used way to gauge whether the stock price lines up with its earnings power. Investors typically expect higher P/E ratios when they see stronger earnings growth potential and lower perceived risk, and lower P/E ratios when growth expectations are modest or risks are higher.

United Parcel Service currently trades on a P/E of about 17.19x. This sits above the Logistics industry average P/E of roughly 14.62x, and below the wider peer group average of about 22.36x. To provide a more tailored benchmark, Simply Wall St also calculates a Fair Ratio of 23.87x for United Parcel Service, which reflects factors such as its earnings growth profile, industry, profit margins, market capitalization and specific risks.

This Fair Ratio is often more informative than a simple comparison with peers or industry averages because it adjusts for company specific characteristics rather than assuming all logistics stocks deserve similar multiples. Comparing the current P/E of 17.19x with the Fair Ratio of 23.87x suggests United Parcel Service trades below the multiple implied by these fundamentals.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your United Parcel Service Narrative

Earlier it was mentioned that there is an even better way to understand valuation. On Simply Wall St this takes the form of Narratives, where you choose a story for United Parcel Service, link that story to explicit forecasts for revenue, earnings and margins, and arrive at a Fair Value you can compare with the current share price to assess whether the stock looks attractive or stretched.

Each Narrative is available in the Community section of the platform, is easy to read, and updates automatically when new information such as news, earnings or guidance is added, so you are not locked into stale assumptions.

For United Parcel Service, one investor might align with a cautious Narrative that sets Fair Value at about US$82.69, built on modest revenue and margin assumptions. Another might prefer a more optimistic Narrative with Fair Value around US$135.00, reflecting higher growth and profitability estimates. Seeing these side by side helps you choose which story best matches your own expectations before deciding how to respond to the gap between Fair Value and the current price.

For United Parcel Service however we will make it really easy for you with previews of two leading United Parcel Service Narratives:

Each one links today’s share price to a different story about revenue, margins and risk. Use them as reference points rather than answers, and decide which assumptions feel closer to your own view before taking any action.

Fair Value: US$135.00

Implied undervaluation vs last close (US$106.14): about 21.4%

Revenue growth assumption: 5.13% a year

- Focuses on UPS using automation, cost reductions and its Efficiency Reimagined program to improve margins and cash flow.

- Highlights healthcare logistics, cold chain and new trade lanes as sources of higher quality, potentially more resilient revenue.

- Assumes UPS can support a higher future P/E multiple if these changes translate into stronger earnings and returns.

Fair Value: US$95.21

Implied overvaluation vs last close (US$106.14): about 11.4%

Revenue growth assumption: 1.75% a year

- Emphasizes pressure from higher costs, new debt, labor issues and shareholder concerns around governance and sustainability.

- Assumes only modest revenue and margin improvement, with profitability sensitive to the success of Efficiency Reimagined.

- Builds in a lower target P/E multiple than the industry, reflecting caution around execution risk and competitive pressure.

Taken together, these Narratives bracket a range of fair values for United Parcel Service that you can use as a cross check on the DCF and P/E work earlier in the article. The right call for you depends on which story and set of assumptions feels more reasonable given your time horizon, risk tolerance and view of how UPS’s transformation and cost programs will play out.

To see how other investors are framing the story, compare, and even challenge these views directly in the Community section by starting with the full bull and bear Narratives for United Parcel Service, including their detailed forecasts, risks and valuation logic, through See what the community is saying about United Parcel Service.

Do you think there's more to the story for United Parcel Service? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.