UnitedHealth Faces PBM Rule And Medicare Probe With Earnings In Focus

UnitedHealth Group Incorporated UNH | 277.26 | +1.20% |

- UnitedHealth Group (NYSE:UNH) is facing a proposed Department of Labor rule aimed at increasing transparency around Pharmacy Benefit Manager compensation.

- The company is also under Department of Justice investigation regarding its Medicare billing practices.

- These developments introduce regulatory, legal, and reputational risks that could affect parts of UnitedHealth's business model.

UnitedHealth Group operates a broad health care business that includes insurance benefits and pharmacy services, including PBM activities. For investors, closer scrutiny of PBM compensation and Medicare billing involves two important profit pools at a time when regulators are paying more attention to health care costs and program integrity.

The outcomes of the proposed rule and the DOJ investigation may influence how UnitedHealth structures contracts, discloses information, and manages compliance. Investors following NYSE:UNH may want to monitor regulatory updates, company responses, and any new disclosures that clarify financial or operational impact.

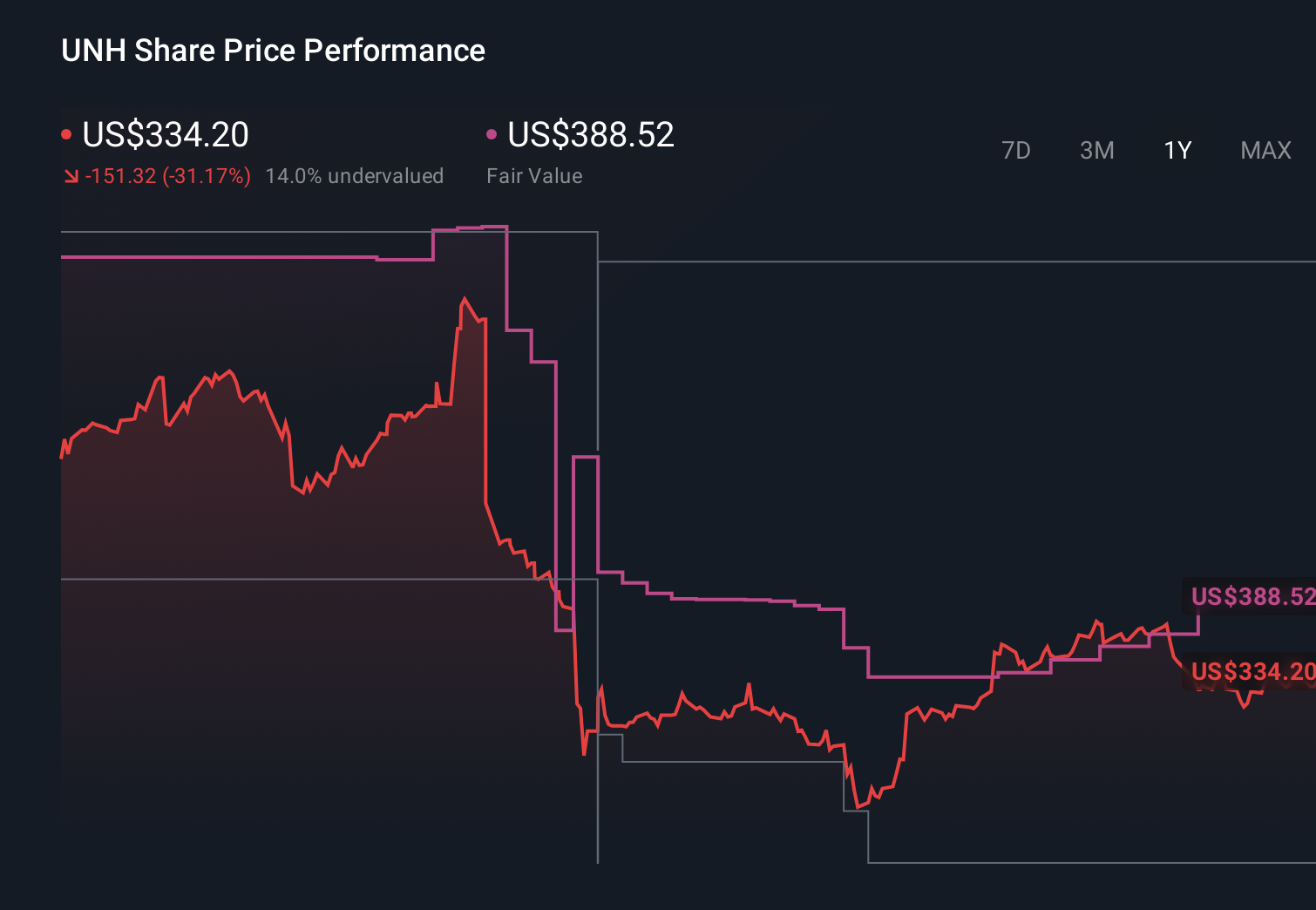

Stay updated on the most important news stories for UnitedHealth Group by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on UnitedHealth Group.

The Department of Labor’s proposed PBM transparency rule and the Department of Justice Medicare billing probe both focus squarely on areas that matter for UnitedHealth’s earnings profile, particularly Optum Rx and its large Medicare Advantage franchise. Greater disclosure of rebates, spread pricing and clawbacks could reduce flexibility in PBM pricing structures, while an adverse outcome from the DOJ investigation could result in fines, repayment obligations or tighter billing rules that weigh on Medicare margins.

How This Fits Into The UnitedHealth Group Narrative

These regulatory threats land at a time when UnitedHealth is already working through higher medical costs, restructuring and a softer outlook, with 2025 net income of US$12.1b versus US$14.4b a year earlier. The existing narratives around Medicare Advantage margin normalization, Optum restructuring and technology investment now have an added layer of uncertainty, because any mandated changes to PBM economics or Medicare billing practices could influence how quickly those improvement efforts show up in reported earnings.

Risks And Rewards Investors Are Weighing

- ⚠️ Regulatory risk that PBM transparency rules compress Optum Rx margins, with read across to peers such as CVS Health and Cigna.

- ⚠️ Legal and financial risk from the DOJ Medicare investigation, which could include penalties, remediation costs or tighter oversight.

- 🎁 Potential long term benefit if clearer PBM economics and compliance upgrades strengthen relationships with employers, regulators and members.

- 🎁 Large, diversified operations and existing earnings guidance for 2026 give investors reference points while assessing how much of the regulatory overhang is already reflected in expectations.

What To Watch Next

From here, it is worth tracking the final form and timing of the PBM rule, disclosures around the DOJ probe, and whether UnitedHealth updates its 2026 guidance if expected impacts become clearer, especially versus competitors like CVS Health and Humana. If you want to see how different investors are framing these risks and opportunities over the long term, take a look at the community views collected in the UnitedHealth Group narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.