UnitedHealth (UNH) Is Up 5.0% After Boosting Dividend Amid Easing Medical Costs - What's Changed

UnitedHealth Group Incorporated UNH | 0.00 |

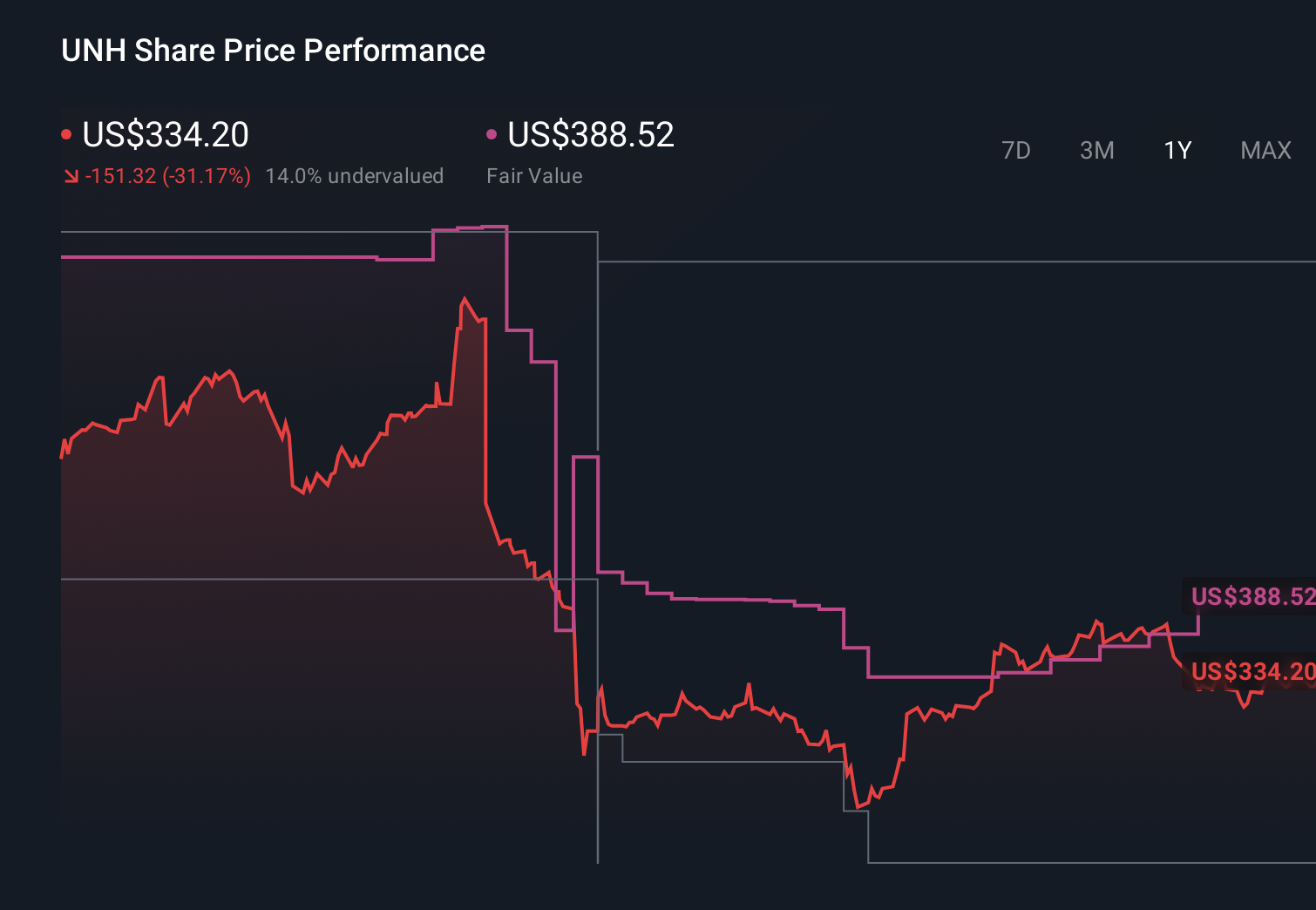

- In early June 2026, UnitedHealth Group’s board approved a higher quarterly cash dividend of US$2.32 per share, payable on June 23 to shareholders of record as of June 15, while analysts highlighted improving medical cost trends and operational execution following past Medicare reimbursement pressures.

- The combination of a 16-year streak of dividend increases, renewed confidence from major Wall Street firms, and ongoing Medicare funding headwinds paints a complex picture of a company balancing shareholder returns with evolving reimbursement and utilization risks.

- Now, we’ll examine how the dividend increase and improving medical cost trends may reshape UnitedHealth Group’s existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

UnitedHealth Group Investment Narrative Recap

To own UnitedHealth Group today, you have to believe its diversified insurance and Optum businesses can keep generating strong cash flow even as Medicare reimbursement rules and utilization trends remain unpredictable. The latest 5% dividend hike and improving medical cost signals support the near term earnings recovery story, but the biggest risk still sits squarely in future Medicare funding decisions and plan design changes, where recent flat 2027 reimbursement guidance underscores that pressure has not gone away.

The most relevant recent development alongside the dividend increase is Bank of America’s upgrade to “Buy,” driven by its view of improving medical cost trends and a more favorable setup into second quarter results. That bullish analyst stance, paired with a 16 year record of dividend growth, strengthens the margin recovery narrative, but it also raises the stakes if upcoming Medicare policy moves or utilization data fail to line up with these more optimistic expectations.

Yet behind the higher dividend and upbeat analyst calls, there is still a meaningful Medicare reimbursement and policy risk that investors should be aware of...

UnitedHealth Group's narrative projects $492.0 billion revenue and $21.4 billion earnings by 2029. This requires 3.0% yearly revenue growth and about a $9.4 billion earnings increase from $12.0 billion today.

Uncover how UnitedHealth Group's forecasts yield a $399.73 fair value, in line with its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were far more cautious, assuming only about US$460.4 billion in revenue and US$20.2 billion in earnings by 2029, reminding you that not everyone shares the same confidence that recent cost trends and dividend news will fully offset long term government program and reimbursement risks.

Explore 62 other fair value estimates on UnitedHealth Group - why the stock might be worth 23% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your UnitedHealth Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free UnitedHealth Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate UnitedHealth Group's overall financial health at a glance.

Searching For A Fresh Perspective?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.