UPS Stock And 2 US Logistics Picks In Focus As Import Rules Change

United Parcel Service, Inc. Class B UPS | 0.00 |

US logistics and warehousing stocks are at the center of a quiet but important shift in how Chinese goods reach American shoppers. The removal of the US de minimis exemption for Chinese imports, and the rise of platforms like Temu and Shein using US-based logistics partners, is reshaping who earns a margin on every parcel and pallet. This article looks at how that news may affect a selection of US logistics and warehousing companies, and highlights 3 stocks from our screener that may be positively exposed to these changing trade and customs patterns.

Ryder System (R)

Overview: Ryder System is a global logistics and transportation company that runs large truck fleets, warehouses, and supply chain operations for businesses, covering everything from vehicle leasing and maintenance to e-commerce fulfillment and last mile delivery.

Operations: Ryder generates most of its US$13.7b revenue from Supply Chain Solutions at about US$5.5b and Fleet Management Solutions at about US$5.9b, with Dedicated Transportation Solutions contributing roughly US$2.3b, and around US$11.8b of total revenue coming from the United States.

Market Cap: US$10.10b

Ryder System sits in the path of shifting trade flows as Chinese platforms push more goods through US-based warehouses. Its mix of fleet management, contract logistics, and e-commerce fulfillment provides multiple ways to participate in domestic demand. The P/E of 20.5x is far below the US Transportation industry average, and recent guidance increases and buybacks show how management is positioning around its outlook, even as margins remain modest and interest coverage is a weak spot. At the same time, competition from asset-light logistics platforms, regulatory changes around imports, and reliance on external borrowing all contribute to the company’s risk profile, which is one reason Ryder can be an interesting stock to study more closely in this new customs regime.

Ryder System’s modest margins, lower P/E and buybacks hint at a story investors may be pricing too cautiously, especially with interest coverage a weak spot that could reshape the 3 key rewards and 2 important warning signs (1 is major!)

United Parcel Service (UPS)

Overview: United Parcel Service is a global delivery and logistics company that moves parcels and freight for businesses and consumers, combining its U.S. ground and air network with international small package operations and supply chain services such as freight forwarding, contract logistics, customs brokerage, and healthcare logistics.

Operations: UPS generates most of its revenue from the U.S. Domestic Package segment at about US$59.2b, with International Package contributing around US$18.7b and Supply Chain Solutions about US$10.4b.

Market Cap: US$91.9b

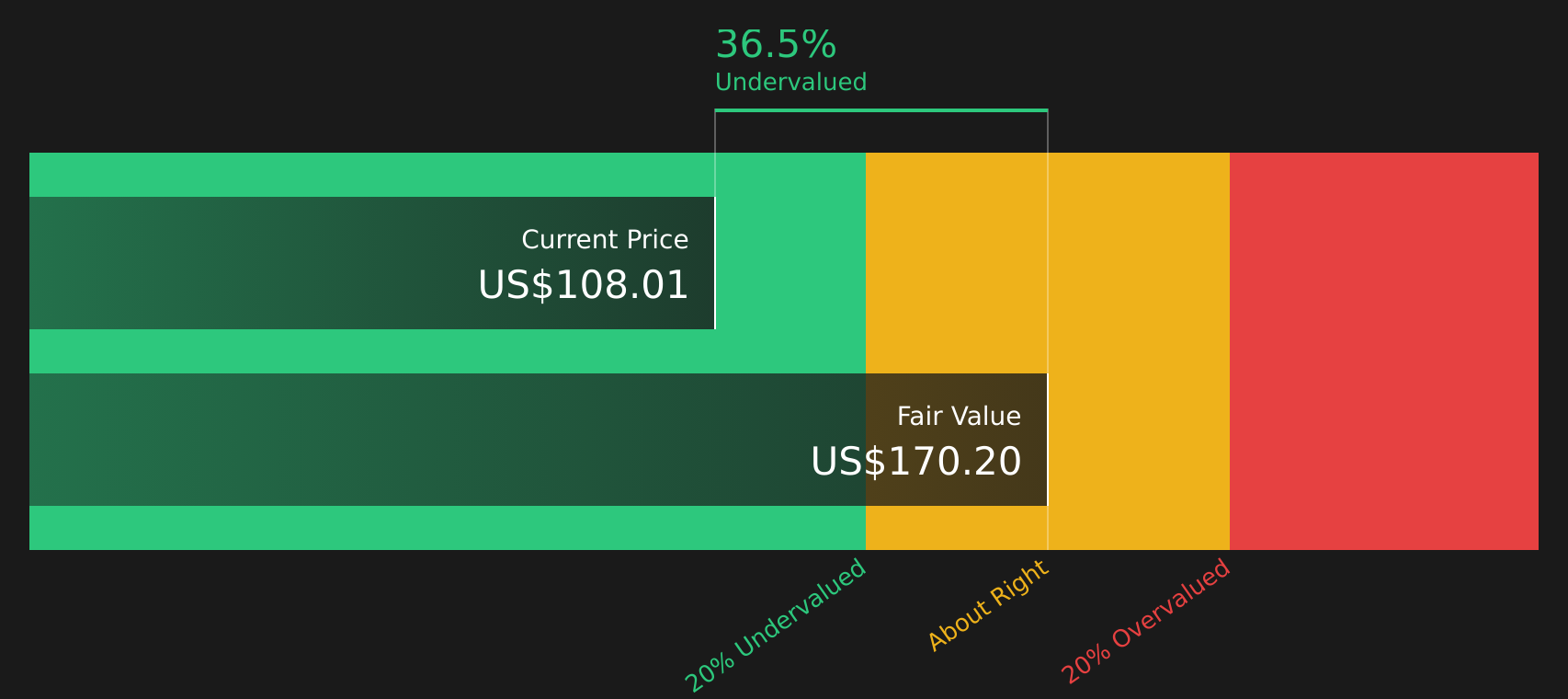

UPS sits squarely at the intersection of tighter customs rules on Chinese imports and rising cross border e-commerce, and its scale, customs brokerage capabilities and technology investments give it tools to handle that complexity as volumes increasingly require formal clearance. At the same time, high leverage, a dividend that is not well covered by earnings or free cash flow, and past declines in revenue and earnings mean investors need to weigh financial risk against what some see as a meaningful gap to fair value. With UPS also pouring money into healthcare cold chain facilities, AI driven network efficiency and return logistics, the key question is how these shifts balance against pressure on margins and funding costs over the next few years.

UPS appears to be a classic case of a large balance sheet raising questions that may be masking a potentially mispriced core business. It is worth reading the 2 key rewards and 2 important warning signs (1 is major!) to see what might be hiding behind the headline numbers.

J.B. Hunt Transport Services (JBHT)

Overview: J.B. Hunt Transport Services is a major US trucking and logistics company that moves freight across road and rail, combining intermodal container shipping, dedicated contract fleets, brokerage, and last mile delivery for a wide range of consumer and industrial goods.

Operations: J.B. Hunt generates most of its US$12.1b revenue from Intermodal at about US$6.0b and Dedicated Contract Services at about US$3.4b, with Integrated Capacity Solutions contributing roughly US$1.2b, Final Mile Services about US$0.8b and Truckload around US$0.8b, almost entirely from the United States.

Market Cap: US$26.4b

J.B. Hunt Transport Services operates where the new customs rules meet real world freight flows, with intermodal and dedicated contract services tied directly to how retailers and platforms move imported goods across the US. Record intermodal volumes, improving profit margins and a high forecast ROE of 23.3% indicate the business is finding ways to use its large asset base more efficiently even as customers rethink sourcing away from China. At the same time, a high P/E, insider selling, reliance on external borrowing and pressure in areas such as Final Mile and truckload pricing mean expectations are elevated, not conservative. The main question for investors is how these strengths and vulnerabilities interact with tighter customs enforcement and the emerging logistics models that e-commerce players are building.

J.B. Hunt’s accelerating intermodal volumes and high forecast ROE make the story look growth heavy, but expectations are already rich and not all segments are firing equally, so the 3 key rewards and 1 important warning sign

The three stocks in this article are just a starting point, and the full US Logistics and Warehousing Stocks screener surfaces 25 more US logistics and warehousing companies with equally compelling narratives around customs shifts, domestic freight, and fulfillment.

Use Simply Wall St to identify and analyze the specific catalysts, financial profiles, and business narratives that matter to you so you can focus on opportunities in this theme that best match your own views and objectives.

Take Control of Your Investment Journey

If J.B. Hunt Transport Services or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Curious About Fresh Investment Alternatives?

Fresh ideas move first, and the stocks with real breakout potential rarely stay under the radar for long. Before the momentum is fully caught by the crowd, consider acting early.

- Spot companies building real cash strength with the curated list of solid balance sheet and fundamentals (48 results) to help you focus on resilient opportunities while it still matters.

- Explore early momentum in high conviction yield plays by scanning the hand picked 8 dividend fortresses before income hunters potentially push valuations higher.

- Track early movers quietly building AI infrastructure with the focused 51 AI infrastructure stocks before these stocks move off many bargain lists.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.