U.S. Bancorp (USB) Launches Comprehensive Cash Flow Platform For Small Businesses

U.S. Bancorp USB | 52.01 | +3.28% |

U.S. Bancorp (USB) launched a new cash flow management platform for small businesses, aiming to enhance financial efficiency for its 1.4 million small business clients. This development is part of USB's continuous efforts to improve its digital solutions. In the last quarter, the company saw an 11% rise in its stock price, aligning with broader market trends. The upbeat economic news, including positive labor market data and potential interest rate cuts, supported a general market uplift. U.S. Bancorp's Q2 earnings report showed strong financial performance, with increased net income and earnings per share, which likely reinforced investor confidence during this period.

The introduction of U.S. Bancorp’s new cash flow management platform for small businesses could bolster its digital banking narrative, aiming to drive sustainable revenue growth and improved efficiencies through technological advancements. This initiative aligns well with the company's ongoing focus on digital solutions, potentially enhancing its revenue prospects by attracting a larger client base looking for streamlined financial management tools.

Over the past five years, U.S. Bancorp has achieved a total shareholder return of 64.72%, which provides a broader context to understand its investment appeal. However, within the last year, the company underperformed both the U.S. market that returned 18.1% and the U.S. Banks industry, which saw a 1-year return of 25.5%. This underperformance highlights a potential area of concern when evaluating the company's competitive positioning.

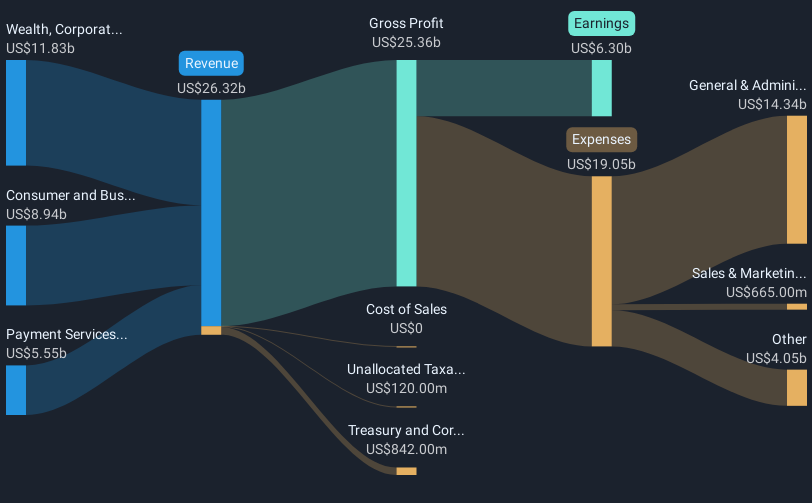

The positive economic developments discussed in the introduction could favorably influence revenue and earnings forecasts by supporting more robust financial activity among U.S. Bancorp's clientele. Analysts see potential for revenue to grow at 8.4% annually over the next three years, while earnings are forecast to reach US$7.4 billion by 2028. The current share price at US$48.54 sits below the consensus analyst price target of US$53.54, indicating a discount and suggesting room for potential upside if the company meets growth expectations. This price movement emphasizes the importance of the company meeting its outlined strategic goals to bridge the gap towards the target.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.