US Bank Stocks With Higher Rate Tailwinds and Stronger Lending Margins

CNB Financial Corporation CCNE | 0.00 |

Higher for longer interest rates, a firm US dollar and stubborn inflation are reshaping the risk and reward profile across US financial stocks exposed to lending margins, funding costs and balance sheet strength. At the same time, geopolitics and softer precious metal sentiment are redirecting attention toward larger, better capitalized institutions that some investors see as relative shelters. This article looks at how that mix of monetary policy signals, currency moves and commodity pressure ties back to our US Financial Sector screener and reveals 3 large bank and non bank financial stocks that appear positively exposed to this news backdrop.

CNB Financial (CCNE)

Overview: CNB Financial is a regional US banking group that offers everyday banking, real estate and commercial lending, private banking, and wealth and asset management services to individuals, businesses, and institutions, as well as distributing annuities and insurance products. Founded in 1865 and headquartered in Clearfield, Pennsylvania, it combines traditional community banking with broader financial services such as trust, estate, and retirement plan administration.

Operations: CNB Financial generates about US$300.3 million in revenue from its core banking operations entirely within the United States.

Market Cap: US$986 million

CNB Financial stands out in the current higher rate backdrop because its core regional lending and deposit franchise can benefit from firmer net interest margins while still offering a 2.26% dividend yield. Recent earnings growth has been strong and analyst forecasts point to growth that is expected to outpace the broader US banks sector. The stock trades on a P/E that is below the peer average, which some readers may see as appealing. At the same time, recent shareholder dilution, a relatively low 9.2% ROE and dependence on continued margin support are real risks to weigh carefully. Recent index inclusion, a live buyback program and conservative executive pay provide additional context that some investors may wish to understand in more detail.

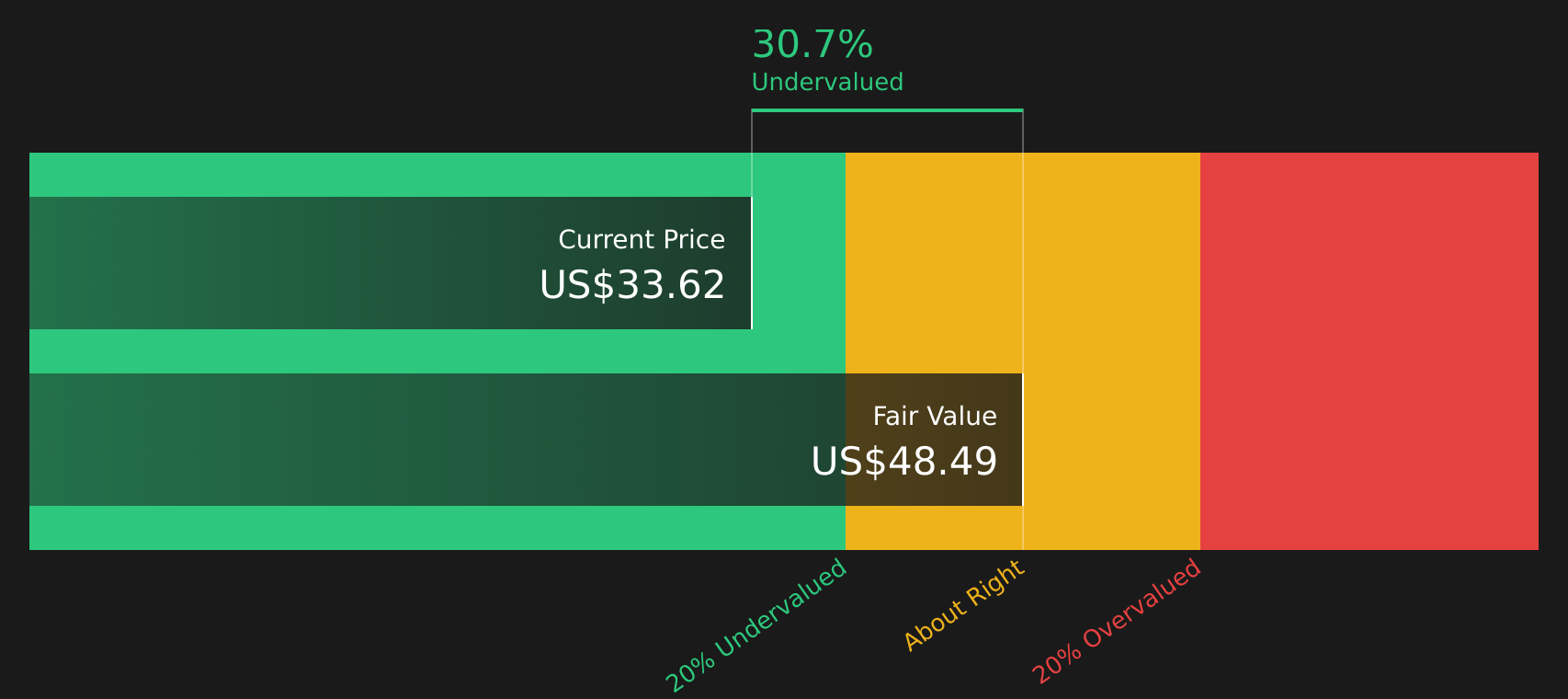

CNB Financial’s mix of regional lending strength, below peer P/E and live buyback raises a key question: how much upside is already priced in, and what the DCF valuation analysis for CNB Financial might be hinting at next

Burke & Herbert Financial Services (BHRB)

Overview: Burke & Herbert Financial Services is a long established US community banking group that offers everyday deposit accounts, digital banking, and a wide range of loans to households and businesses, alongside cash management, treasury, and wealth and trust services. It supports both small businesses and larger commercial clients with solutions that span payments, cash flow tools, and risk management.

Operations: Burke & Herbert Financial Services generates about US$340.9 million in revenue from its community banking operations, all within the United States.

Market Cap: US$1.42b

Burke & Herbert Financial Services is drawing attention because it is a pure play US community bank whose earnings profile appears closely aligned with the higher rate backdrop and core lending margins. Earnings grew very strongly over the past year, margins sit around 34.2%, and analysts expect earnings and revenue to grow at more than 20% a year. The stock trades on a P/E below the broader US market and offers a 3.13% dividend yield. At the same time, a relatively low loan loss allowance, recent shareholder dilution and only mid teens ROE mean the quality of that growth deserves scrutiny, especially as leadership and index membership have recently shifted.

Burke & Herbert Financial Services has accelerating earnings and a 3.13% yield, but the real story could be how growth, loan loss cover and dilution fit together, so unpack the 5 key rewards and 2 important warning signs (1 is major!)

Midland States Bancorp (MSBI)

Overview: Midland States Bancorp is a US financial holding company for Midland States Bank, offering a full range of commercial and real estate lending, equipment leasing, and everyday banking services, alongside trust and wealth management solutions for individuals, businesses, municipalities, and other institutions.

Operations: Midland States Bancorp generates about US$254.7 million from Banking and US$31.8 million from Wealth Management, with small Corporate losses, all within the United States.

Market Cap: US$632.9 million

Midland States Bancorp is firmly tied to traditional lending and deposit banking, which can be attractive when higher for longer US interest rates support wider spreads between what banks earn on loans and pay on deposits. The stock is trading well below some fair value estimates and earnings are forecast to expand quickly, yet recent years have included earnings declines and a low 6.3% ROE, so investors need to weigh improvement against that history. A 4.19% dividend yield and an active buyback program point to shareholder focus, but the dividend is not well covered by current or projected earnings, which raises sustainability questions. What really matters now is how Midland States Bancorp’s profit recovery, credit trends and payout policy hold up if elevated rates persist.

Accelerating profit recovery at Midland States Bancorp, a 4.19% yield and an active buyback raise a bigger question, so walk through the 3 key rewards and 1 important warning sign

The 3 stocks highlighted here are just a starting point, and the full US Financial Sector idea uncovers 33 more companies with similarly detailed stories on lending margins, funding costs and balance sheet strength through the US Financial Sector (Banks & Non-Bank Financials) screener. Use Simply Wall St to identify and analyze the specific catalysts and narratives that matter most to you, so you can focus on the highest conviction opportunities in this corner of the market.

Take Control of Your Investment Journey

If Burke & Herbert Financial Services or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Banks?

Fresh ideas move first, and latecomers get caught chasing momentum while the best entry points are already flying. Scan curated stock sets before the crowd and act now.

- Spot potential breakout value by scanning a curated 45 high quality undervalued stocks that focuses on resilient cash flows and balance sheets while they are still under the radar.

- Ride structural growth trends by zeroing in on 52 AI infrastructure stocks quietly building the digital backbone that supports ongoing AI and data demand.

- Target staying power and income by reviewing a hand picked 9 dividend fortresses list before yields compress and the most dependable payouts become fully priced.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.