US High Growth Tech Stocks To Watch This January 2026

Rumble RUM | 4.98 | -0.60% |

As 2025 comes to a close, the U.S. stock market has seen significant gains despite ending the year with a string of losses, with technology firms driving much of this growth. In this environment, identifying high-growth tech stocks involves looking at companies that are not only innovative but also capable of sustaining momentum in an ever-evolving market landscape.

Top 10 High Growth Tech Companies In The United States

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Marker Therapeutics | 62.86% | 62.39% | ★★★★★★ |

| Sanmina | 31.01% | 33.24% | ★★★★★☆ |

| Palantir Technologies | 26.25% | 30.13% | ★★★★★★ |

| Workday | 11.13% | 32.18% | ★★★★★☆ |

| Circle Internet Group | 20.75% | 84.58% | ★★★★★☆ |

| RenovoRx | 59.12% | 64.21% | ★★★★★☆ |

| Zscaler | 15.85% | 45.93% | ★★★★★☆ |

| Cellebrite DI | 15.29% | 20.24% | ★★★★★☆ |

| Procore Technologies | 11.70% | 116.48% | ★★★★★☆ |

| Duos Technologies Group | 53.76% | 155.11% | ★★★★★☆ |

Underneath we present a selection of stocks filtered out by our screen.

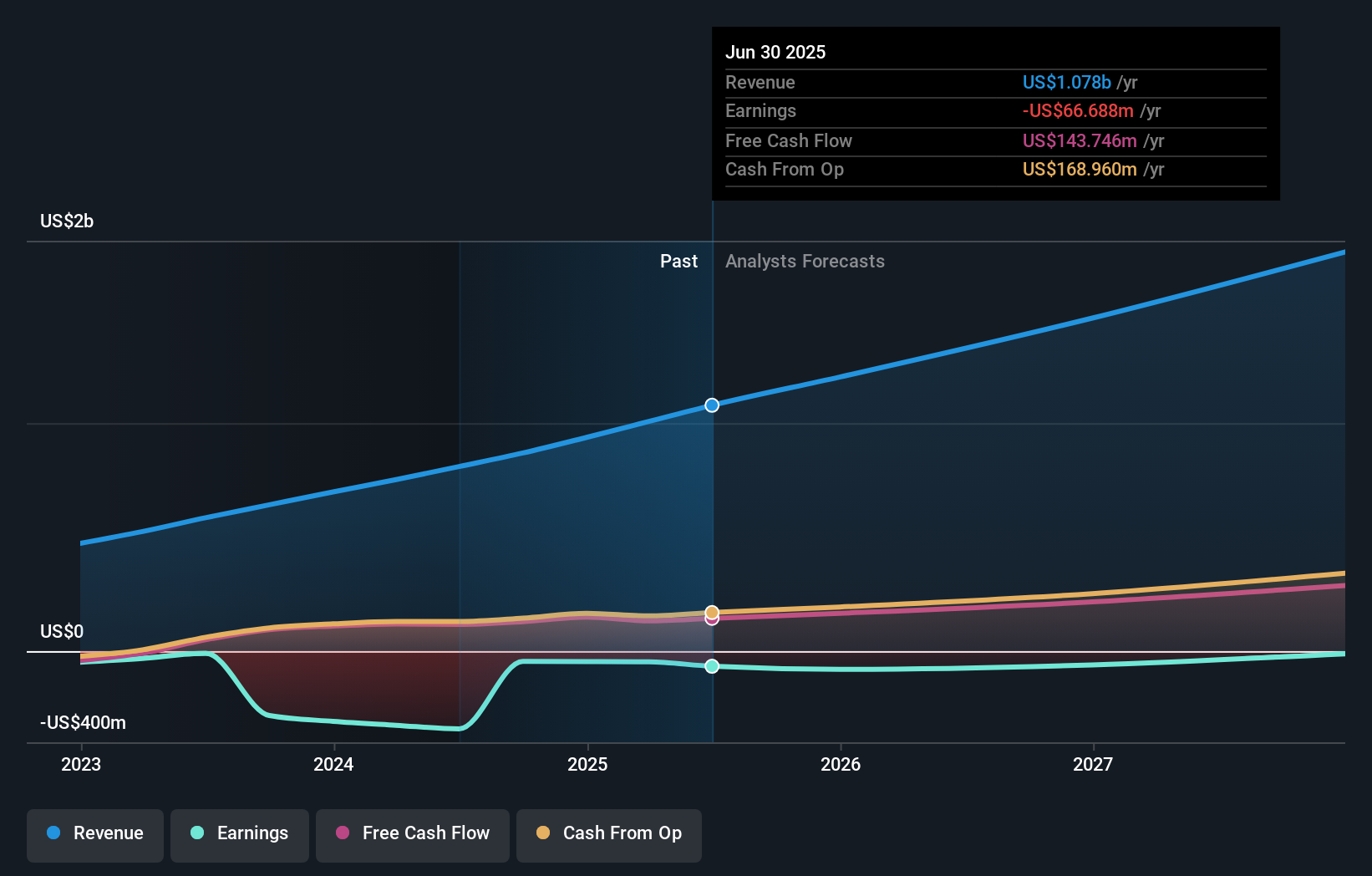

Rumble (RUM)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Rumble Inc. operates video sharing platforms and cloud services across the United States, Canada, and internationally with a market cap of $2.14 billion.

Operations: Rumble generates revenue primarily from its Internet Software & Services segment, which amounts to $103.78 million.

Rumble's strategic moves, including a high-profile exclusive livestreaming event and partnerships for enhanced AI-driven content discoverability, underscore its innovative approach in the competitive digital media space. Despite current unprofitability, Rumble's revenue is projected to surge by 52.5% annually, significantly outpacing the US market average of 10.4%. This growth is complemented by an expected annual earnings increase of 84.27%, positioning it well for future profitability. Recent initiatives like the integration with Perplexity's AI tools not only expand Rumble’s service offerings but also improve user engagement through advanced search functionalities, crucial for sustaining long-term growth in an industry where content relevance and accessibility are key.

Klaviyo (KVYO)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Klaviyo, Inc. is a technology company that offers a software-as-a-service platform across various regions including the United States, other Americas, the Asia-Pacific, Europe, the Middle East, and Africa with a market cap of approximately $9.80 billion.

Operations: Klaviyo generates revenue primarily from its internet software segment, amounting to $1.15 billion. The company operates a software-as-a-service platform across multiple global regions.

Despite being unprofitable, Klaviyo is on a robust upward trajectory with its revenue forecast to grow at 16.3% annually, outpacing the US market average of 10.4%. The company's strategic leadership changes, including the appointment of Chano Fernández as co-CEO, underscore its commitment to innovation and global expansion. Notably, Klaviyo's R&D investments are set to enhance its software solutions further, vital in an industry where staying ahead technologically translates directly into competitive advantage. With a projected shift into profitability within three years and an impressive expected earnings growth rate of 66.5%, Klaviyo is positioning itself as a significant player in the tech landscape.

Zeta Global Holdings (ZETA)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Zeta Global Holdings Corp. operates an omnichannel data-driven cloud platform offering consumer intelligence and marketing automation software to enterprises globally, with a market capitalization of approximately $5 billion.

Operations: The company generates revenue from its Internet Software & Services segment, amounting to $1.22 billion. The platform supports enterprises in enhancing consumer intelligence and automating marketing processes across various channels.

Zeta Global Holdings, despite its current unprofitability, is on a promising trajectory with revenue growth forecasted at 17.4% annually, outpacing the US market average of 10.4%. The company's recent upward revision in revenue and earnings guidance for upcoming quarters highlights its potential turnaround and growth prospects. Notably, Zeta has been actively investing in R&D with expenses growing at a significant rate, which is crucial for maintaining technological competitiveness in the rapidly evolving tech landscape. These strategic investments are expected to drive future innovations and improve profitability as indicated by the projected earnings growth of 143.73% per year.

Taking Advantage

- Get an in-depth perspective on all 71 US High Growth Tech and AI Stocks by using our screener here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.