US Manufacturing Stocks That Could Benefit If North American Trade Rules Tighten

CNH Industrial NV CNH | 0.00 |

The decision by the United States to hold off on renewing the USMCA adds a fresh layer of uncertainty to North American trade, and that can matter a lot for US manufacturers tied to cross border supply chains. Some companies may see risk if trade frictions rise, while others could benefit if production tilts further toward domestic plants and suppliers. This article looks at how that news connects to a focused group of US manufacturing stocks and what that could mean for investors considering exposure to trade sensitive businesses. It will also outline 3 stocks from the screener that have been identified as potential beneficiaries.

CNH Industrial (CNH)

Overview: CNH Industrial is a global equipment company that makes and sells agricultural and construction machinery, from tractors and harvesters to excavators and loaders, as well as offering financing for customers and dealers through its financial services arm.

Operations: CNH Industrial generates most of its revenue from industrial activities, with about US$12.4b from Agriculture, US$2.9b from Construction, and US$2.7b from Financial Services, plus a small contribution from eliminations and other items.

Market Cap: US$13.9b

CNH Industrial sits at the center of US agricultural and construction equipment, which puts it squarely in focus as the US leans harder into domestic manufacturing and tighter North American trade rules. The company is investing heavily in precision agriculture, connectivity and automation, backed by an R&D ecosystem and logistics upgrades that aim to speed product development and parts availability. At the same time, investors have to weigh a thin 2.1% profit margin, weaker recent earnings and funding risk from reliance on external borrowing. With analysts expecting faster earnings growth than revenue and regulators reshaping tariffs and trade, the real question is how this mix of tech ambitions, trade exposure and balance sheet pressure could reshape CNH Industrial’s long term profile for investors.

CNH Industrial’s push into precision agriculture and automation could matter more than the thin 2.1% margin suggests, especially with trade rules in flux, so it may be worth reviewing the 1 key reward and 2 important warning signs (1 is major!)

Dongfeng Motor Group (DNFG.F)

Overview: Dongfeng Motor Group is a major Chinese auto manufacturer that designs and builds a wide range of commercial trucks, buses and passenger cars, including electric and new energy vehicles, and supports these products with financing, leasing, logistics and other auto related services.

Operations: Dongfeng Motor Group generates essentially all of its revenue in the People’s Republic of China, with about CN¥121.3b coming from its domestic market.

Market Cap: US$8.7b

Dongfeng Motor Group provides exposure to China’s auto market, growing new energy vehicle partnerships and export potential at a time when Western trade policy is in flux and European partners like Stellantis are working more closely with the company on future models and production. Recent full year and Q1 results show higher sales but continuing losses, so the stock combines growth potential with clear execution risk around turning revenue into profit and managing high reliance on external borrowing. For investors tracking US friendly or diversified manufacturing supply chains, the mix of expanding international alliances, low P/S ratio and unprofitable results raises an important question about whether the current set up is an early stage opportunity or a value trap in the making.

Dongfeng Motor Group’s growing new energy vehicle footprint and export ties could be masking a far more interesting setup, so it may be worth reviewing the 1 key reward and 1 important major warning sign

ESCO Technologies (ESE)

Overview: ESCO Technologies is a US based manufacturer that supplies highly engineered filtration, testing and diagnostic equipment to aerospace and defense customers, electric utilities, renewable energy projects and industrial clients that need reliable power and electromagnetic management.

Operations: ESCO Technologies generates most of its revenue from Aerospace & Defense at about US$600.8m, followed by Utility Solutions Group at roughly US$383.6m and Test at about US$263.6m.

Market Cap: US$9.1b

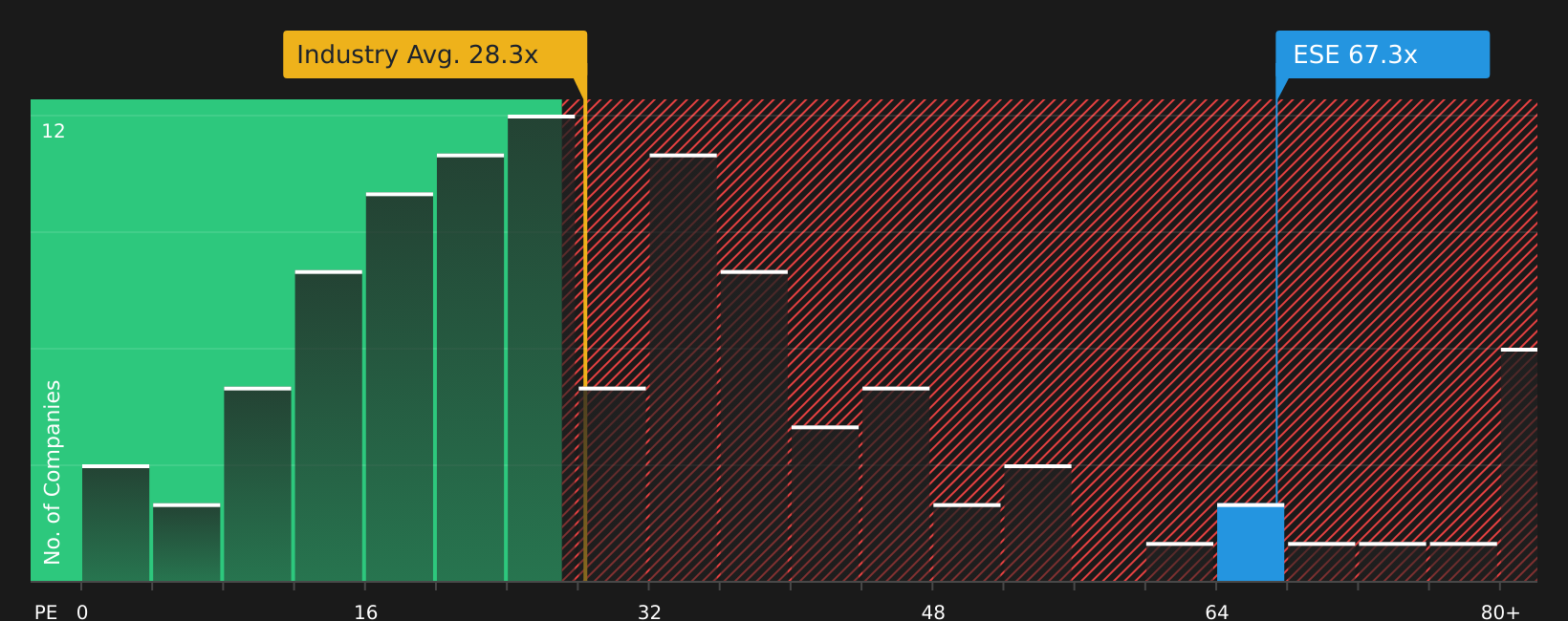

ESCO Technologies stands out in this US manufacturing screener because it ties together several powerful themes, including grid reliability, defense spending and onshoring of critical components, while keeping a strong base of US operations that are less exposed to USMCA trade friction. Its Utility Solutions and RF Test tools sit directly in the path of spending on power quality, renewables and compliance, and the aerospace and maritime businesses give it multi year backlog visibility. On the other hand, the company trades at a high P/E multiple, faces funding risk from reliance on external borrowing and has integration work around a large acquisition, so investors need to weigh quality earnings and momentum against valuation stretch and execution risk.

ESCO Technologies’ momentum story is tied to grid reliability and defense spend, but the valuation debate is only half the picture. As a result, it may be worth reviewing the analyst forecasts for ESCO Technologies

The stocks covered here are only a starting point, and the full US Domestic Manufacturing screener highlights 27 more US headquartered manufacturers with equally compelling stories tied to domestic production and supply chains. Use Simply Wall St to identify, analyze and filter for the specific catalysts and narratives that matter most to you so you can focus on the highest conviction opportunities in this theme.

Take Control of Your Investment Journey

If CNH Industrial or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Others Do

Markets move fast and the best breakout stories rarely stay under the radar for long. Spot fresh momentum before the crowd catches on and ideal entry points start dropping, act now.

- Target resilient compounding potential with a curated 73 resilient stocks with low risk scores that aims to keep volatility in check while you focus on building long term wealth.

- Hunt for under the radar growth stories using a carefully filtered 19 high quality undiscovered gems that spotlights quality businesses still flying beneath most investors' screens.

- Position around powerful secular themes through a focused 53 AI infrastructure stocks that zeroes in on companies building the backbone of future computing demand.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.