US Onshoring Stocks That Could Benefit If Tariffs Reshape Apparel Sourcing

Jerash Holdings (US), Inc. JRSH | 0.00 |

New US tariff proposals on Bangladeshi exports are putting fresh attention on companies that make more of their products at home. Higher trade costs for overseas apparel and consumer goods suppliers could shift some demand toward US-based manufacturers, particularly those tied to textiles and related products. For investors, that creates a focused theme, not a guarantee, around domestic production and onshoring. This article looks at how the news might affect three US-listed stocks and why each could be positively exposed to these tariff discussions, helping you decide whether they deserve a closer look in your own research.

Unifi (UFI)

Overview: Unifi is a Greensboro based textile manufacturer that makes recycled and synthetic polyester and nylon yarns, selling them mainly to yarn makers, knitters, and weavers for use in apparel, automotive, home furnishings, industrial, and medical fabrics under its REPREVE brand.

Operations: Unifi generates about US$525.6m in revenue, primarily from the Americas segment at US$325.8m, with additional contributions from Brazil at US$110.0m and Asia at US$89.8m.

Market Cap: US$97.6m

Unifi sits at the intersection of two themes many investors are watching closely: onshoring and recycled materials. The company is unprofitable today and has reported recent losses, so this is not a low risk story. Tariffs that make imported textiles more expensive could improve the appeal of its US based operations if brands reassess sourcing away from parts of Asia. Management has highlighted that its Americas footprint is positioned to pick up demand if trade barriers persist. The stock trades on a low P/S multiple and close to an internally assessed fair value, leaving investors to weigh whether a potential shift in apparel supply chains can help turn operational progress into a more durable recovery.

Unifi’s mix of onshoring and recycled yarns could be masking a more interesting risk reward trade off than the headline losses suggest, so review the DCF valuation analysis for Unifi to see what the market might be missing.

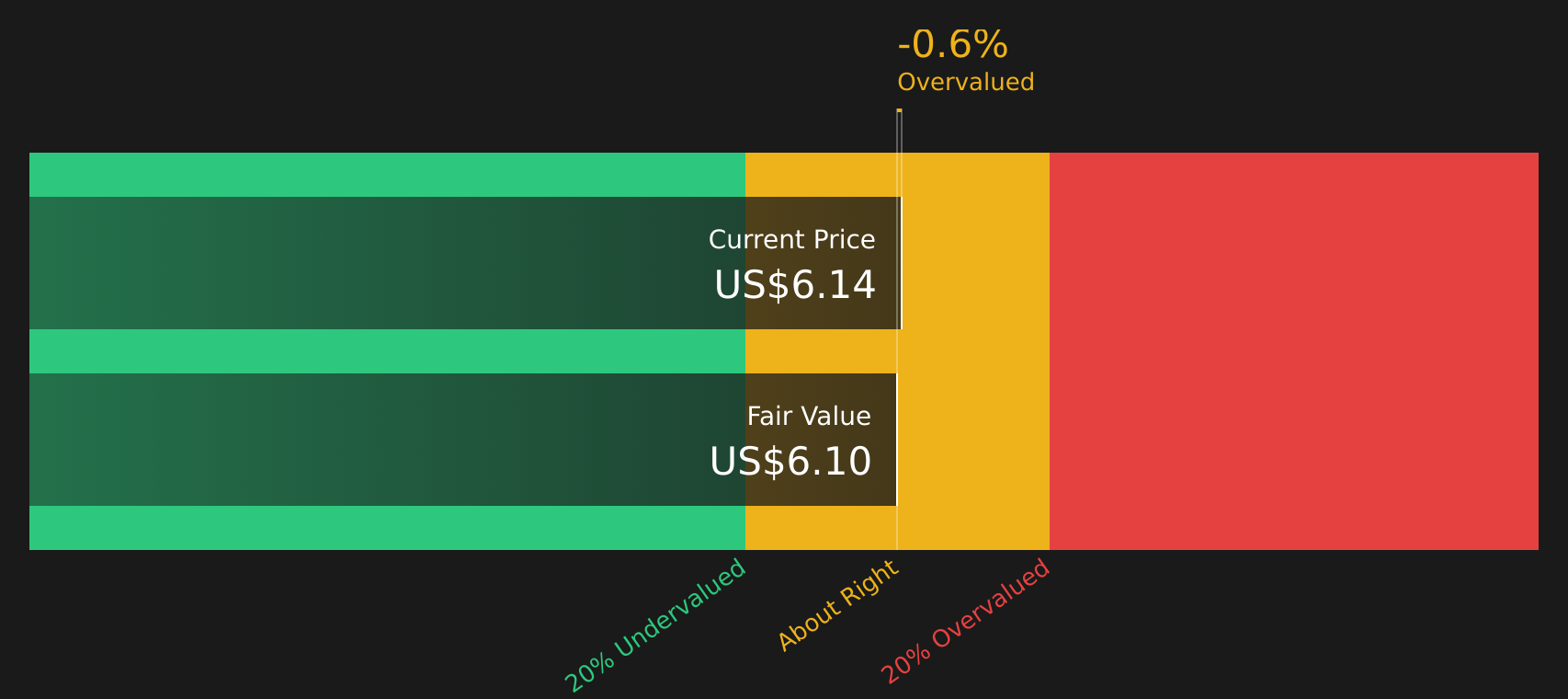

Jerash Holdings (US) (JRSH)

Overview: Jerash Holdings (US) is an apparel manufacturer that produces customized sportswear and outerwear, including t-shirts, jackets, vests, pants, shorts, polo shirts and personal protective equipment, supplying major brands and retailers across the United States, Europe, Asia and the Middle East from its Jordan based facilities.

Operations: Jerash Holdings (US) generates about US$166.3m in revenue from apparel, with the United States contributing roughly US$138.2m and meaningful additional sales to China including Hong Kong, the Republic of Korea, Jordan and other markets.

Market Cap: US$57.0m

Jerash Holdings (US) sits squarely in the tariff and onshoring story, with production in Jordan benefiting from lower effective US import duties than competitors in Bangladesh, India and other Asian hubs at a time when proposed Section 301 changes could raise costs for those rivals. The company has recently moved from losses to profitability, pays a dividend, and is tied into global brands that are actively diversifying away from higher tariff regions. It still carries risks around dependence on favorable trade agreements, working capital pressure and concentrated operations in Jordan. For investors tracking how supply chains and tariffs are reshaping apparel sourcing, the full Jerash picture is more nuanced than the headline numbers suggest and may warrant closer inspection.

Jerash Holdings (US) looks like an onshoring beneficiary hiding in plain sight, with US linked apparel demand and tariff advantages that many investors may be underestimating, so review the 4 key rewards and 1 important warning sign

FIGS (FIGS)

Overview: FIGS is a direct to consumer healthcare apparel company that designs and sells scrubs and related lifestyle clothing and accessories for medical professionals through its website, app, B2B channel, and a growing retail presence in the US and internationally.

Operations: FIGS generates about US$666.1m in revenue almost entirely from online retailers, with around US$553.0m from the United States and US$113.1m from the rest of the world.

Market Cap: US$1.7b

FIGS gives investors a focused way to gain exposure to US onshoring and premium healthcare workwear, with a direct to consumer model that supports margins and a brand that many clinicians actively seek out. Earnings are described as high quality, margins have improved alongside a 6.1% net margin, and management is still reinvesting in growth levers such as TEAMS bulk orders, product extensions and selective retail. At the same time, FIGS carries a relatively high P/E, relies on external funding and faces tariff and FX headwinds as sourcing and global trade rules evolve. That mix of strong brand equity, improving profitability and real execution risk makes FIGS a stock where the potential upside case is notable but accompanied by meaningful risk.

FIGS appears to be premium healthcare workwear with earnings quality and a growing TEAMS and retail push that many investors may be underpricing, so walk through the analyst forecasts for FIGS to see what might be quietly building under the surface.

The three stocks in this article are only a starting point, and the full US Domestic Manufacturing & Onshoring screener highlights 7 more US focused manufacturers with potential onshoring angles and equally compelling company narratives. Use Simply Wall St to identify, analyze and filter for the specific catalysts and storylines around tariffs, domestic production and supply chain shifts so you can focus on the highest conviction ideas in this theme.

Take Control of Your Investment Journey

If FIGS or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Others Catch On

Some stocks can move from quiet to crowded quickly as momentum builds and prices start to move. Review these ideas early, before the window narrows.

- Spot under-the-radar quality by reviewing a curated 19 high quality undiscovered gems that could become harder to access once there is broader attention.

- Target resilient cash flows with a focused 9 dividend fortresses before additional demand affects yields and entry points.

- Track real business traction through a refined 63 profitable AI stocks that aren't just burning cash while these cash-generating AI stocks are still priced as secondary stories rather than central ones.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.