US Undiscovered Gems to Explore This May 2026

Power Solutions International PSIX | 0.00 |

The United States market has experienced a notable uptrend, climbing 1.2% in the last week and an impressive 29% over the past year, with earnings forecasted to grow by 17% annually. In this robust environment, identifying stocks that are not only poised for growth but also remain under the radar can offer unique opportunities for investors seeking to capitalize on these favorable conditions.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 69.86% | 1.25% | -3.09% | ★★★★★★ |

| Security Federal | 18.41% | 5.46% | -0.53% | ★★★★★★ |

| Tri-County Financial Group | 54.21% | -0.70% | -10.52% | ★★★★★★ |

| Southern Michigan Bancorp | 108.80% | 7.38% | 0.84% | ★★★★★★ |

| Cashmere Valley Bank | 31.63% | 5.07% | 1.43% | ★★★★★★ |

| Sound Financial Bancorp | 16.13% | 0.44% | -12.60% | ★★★★★★ |

| Teekay | 2.14% | 10.67% | 57.58% | ★★★★★★ |

| SIFCO Industries | 12.27% | -4.21% | -2.87% | ★★★★★★ |

| NameSilo Technologies | 3.13% | 14.25% | 15.06% | ★★★★★☆ |

| High Templar Tech | 13.55% | -66.76% | -26.62% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

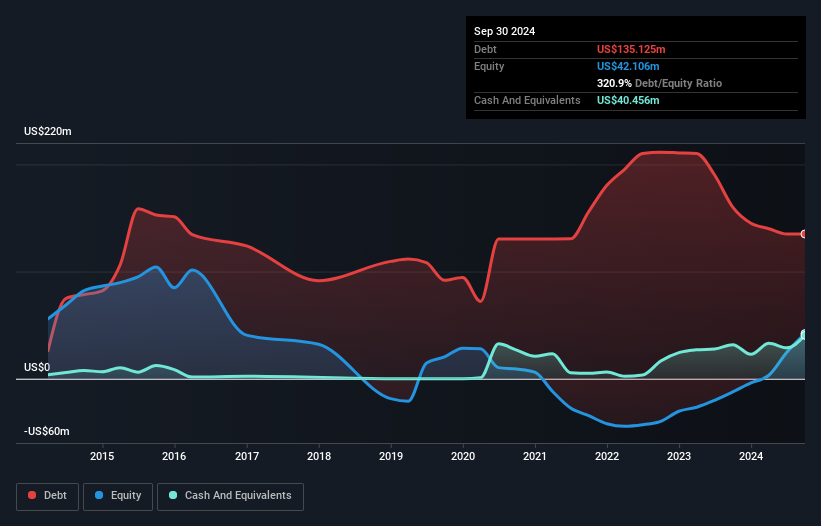

Power Solutions International (PSIX)

Simply Wall St Value Rating: ★★★★★★

Overview: Power Solutions International, Inc. is a company that designs, engineers, manufactures, markets, and sells engines and power systems across various regions including the United States and internationally, with a market cap of $895.97 million.

Operations: PSIX generates revenue primarily from its Engineered Integrated Electrical Power Generation Systems, amounting to $715.55 million.

Power Solutions International, with its earnings growing 25.8% over the past year, outpaced the electrical industry average of 23.1%. Despite a volatile share price recently, it trades at a significant discount of 78.8% below estimated fair value and boasts a satisfactory net debt to equity ratio of 31.9%. The company’s interest payments are well-covered by EBIT at 14.4 times coverage, indicating financial stability despite recent executive changes and legal challenges. While gross margins faced pressure due to production inefficiencies for data center products, the firm remains free cash flow positive with high-quality non-cash earnings contributing to its financial health.

TOYO (TOYO)

Simply Wall St Value Rating: ★★★★☆☆

Overview: TOYO Co., Ltd. operates across the solar power supply chain, including wafer and silicon production, solar cell manufacturing, and photovoltaic module development in Asia and the United States, with a market cap of approximately $542.97 million.

Operations: TOYO generates revenue primarily from the Machinery & Industrial Equipment segment, totaling $518.61 million. The company's operations span various stages of the solar power supply chain, contributing to its financial performance.

TOYO, a smaller player in the semiconductor industry, has demonstrated remarkable financial performance with earnings skyrocketing 203.6% over the past year, surpassing the industry's 18.7%. Trading at nearly 82% below estimated fair value suggests it offers significant upside potential. The company's interest payments are comfortably covered by EBIT at a ratio of 27.4 times, indicating strong financial health despite recent volatility in share price. Recent leadership changes and strategic focus on U.S. market expansion may bolster its growth trajectory further, although concerns remain about its ability to sustain operations long-term as highlighted by auditor doubts.

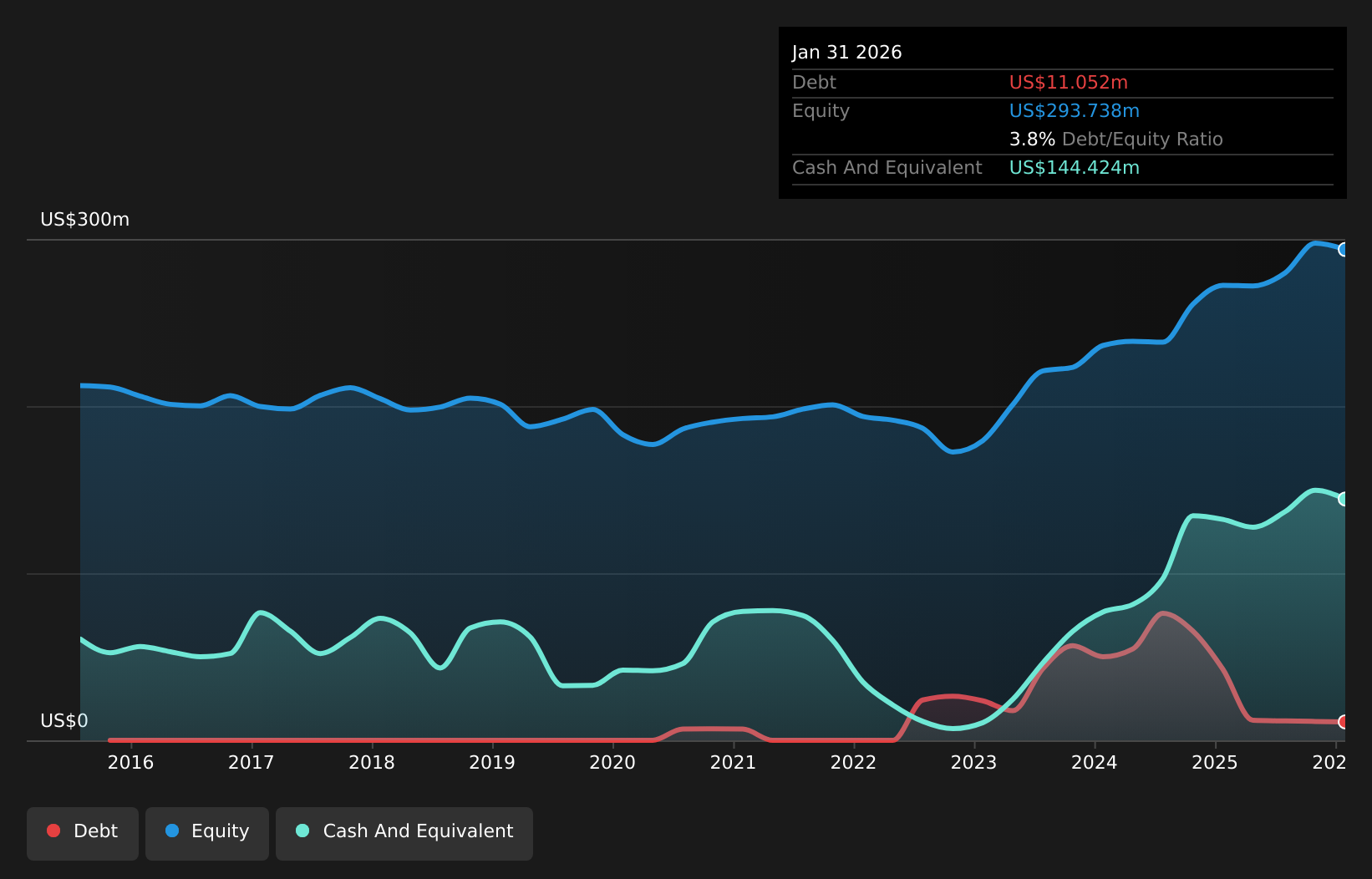

Daktronics (DAKT)

Simply Wall St Value Rating: ★★★★★★

Overview: Daktronics, Inc. is a company that specializes in designing, manufacturing, and selling electronic scoreboards and display systems for various applications including sports, commercial sectors, and transportation both domestically and internationally, with a market cap of approximately $979.97 million.

Operations: Daktronics generates revenue through five primary segments: Commercial ($181.01 million), Live Events ($295.79 million), International ($76.98 million), Transportation ($71.43 million), and High School Park and Recreation ($177.44 million).

Daktronics, a player in the electronic display industry, has seen its earnings soar by 2561.6% over the past year, outpacing the Electronic industry's growth of 13.4%. The company turned its negative shareholder equity from five years ago into a positive figure and now holds more cash than total debt, indicating improved financial health. Despite a one-off loss of US$13.7 million impacting recent results, Daktronics remains profitable with free cash flow standing at US$61.98 million as of January 2026. Recent projects include major installations at Yankee Stadium and Los Angeles International Airport, showcasing their expanding footprint in digital displays for sports and transportation sectors.

Turning Ideas Into Actions

- Unlock our comprehensive list of 338 US Undiscovered Gems With Strong Fundamentals by clicking here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.