Valero Energy (VLO) One Off US$1.1b Loss Tests Bullish Earnings Growth Narratives

Valero Energy Corporation VLO | 244.09 | +1.09% |

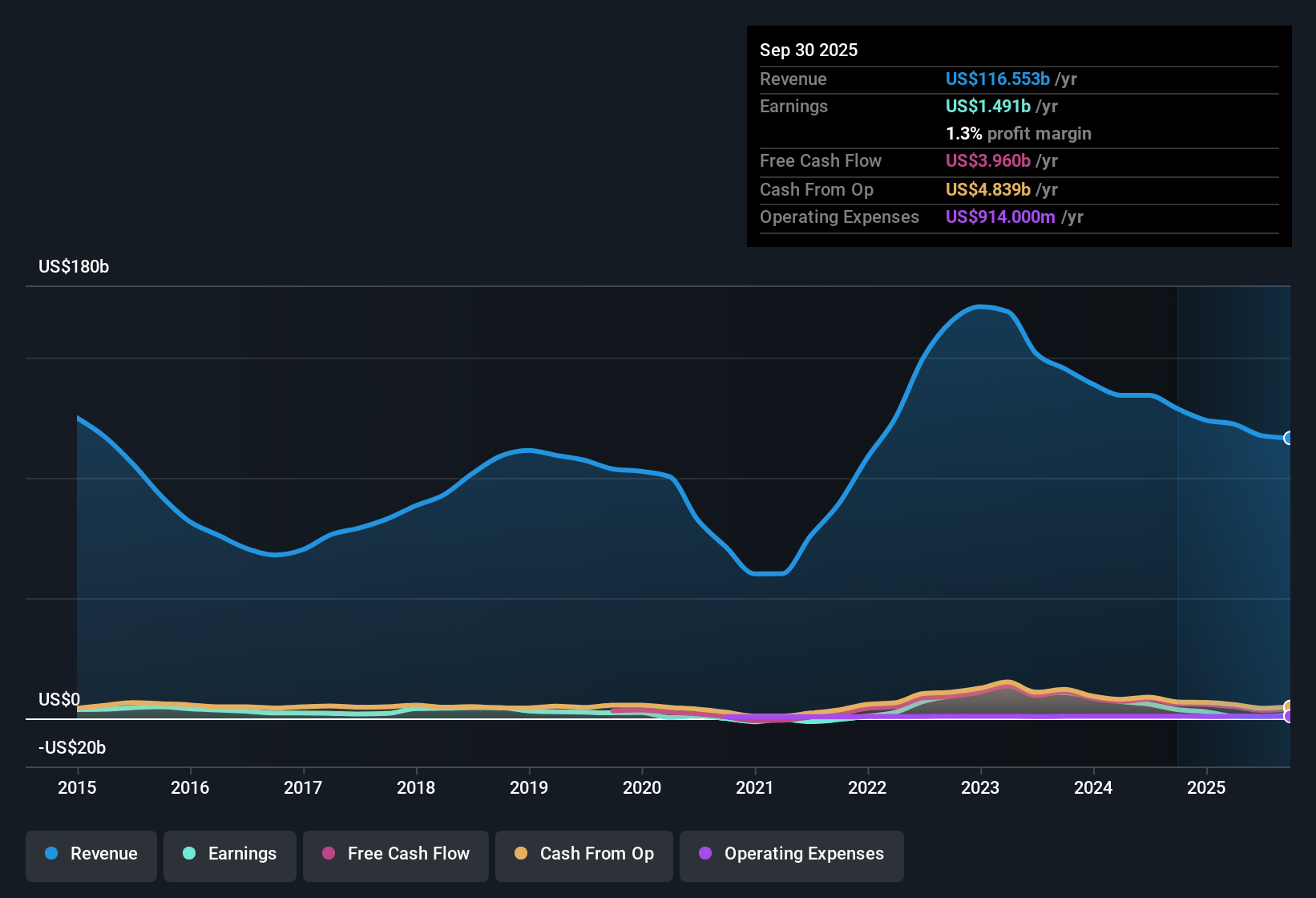

Valero Energy (VLO) closed out FY 2025 with fourth quarter revenue of US$30.4b and basic EPS of US$3.74, capping a year in which trailing twelve month revenue sat at US$122.7b and EPS at US$7.60. The company has seen quarterly revenue move from US$29.2b in Q4 2024 to between US$28.2b and US$31.3b across 2025, while basic EPS shifted from US$0.89 in Q4 2024 to a range spanning a loss of US$1.90 in Q1 2025 through to US$3.74 in Q4, leaving investors focused on how a 1.9% trailing net margin and a sizeable one off loss filter through to the quality of underlying profitability.

See our full analysis for Valero Energy.With the headline numbers on the table, the next step is to see how this mix of thin margins, one off impacts and changes in earnings expectations lines up against the most commonly held narratives around Valero and its outlook.

Margins Feel Tight At 1.9%

- Trailing net profit margin sits at 1.9%, compared with 2.2% a year earlier, on US$122.7b of revenue and US$2.3b of net income over the last twelve months.

- What stands out for a bearish take is that this thinner margin is showing up alongside mixed quarterly profitability, including a Q1 2025 net loss of US$596 million on US$28.8b of revenue, which critics may point to when they question how resilient profits are through the cycle.

- Bears may also highlight that EPS over the last twelve months is US$7.60, while the one off US$1.1b loss is still visible in those figures, so reported profitability is carrying the weight of that event.

- At the same time, quarterly net income excluding extra items moved from US$280 million in Q4 2024 to above US$1.1b in both Q3 and Q4 2025, so the margin picture is not one way for either side of the debate.

US$1.1b One Off Loss Still Matters

- The trailing figures include a non recurring loss of US$1.1b, which is large compared with the latest twelve month net income of US$2.3b and helps explain why EPS over that period is US$7.60 despite some strong recent quarters.

- What is interesting for a bullish view is that, even with this loss included, analyst models in the data point to earnings growth of around 16.1% per year and show 5 year earnings growth of 8.1% per year, so supporters may argue that the one off item does not define the longer term earnings trend.

- Bulls could argue that the quarterly pattern, with basic EPS of US$2.29, US$3.53 and US$3.74 in Q2, Q3 and Q4 2025 after the loss hit, signals that underlying operations are still producing solid profit per share.

- On the other hand, the 1.9% margin and the presence of the US$1.1b charge mean anyone leaning on the growth story needs to keep checking whether future reported earnings continue to absorb that kind of hit.

Valuation Split Between P/E 23.7x And DCF

- The data shows a P/E of 23.7x versus a US Oil & Gas industry average of 13.8x and a peer average of 27.2x, while a DCF fair value of US$310.88 sits well above the current share price of US$182.49, a gap of about 41.3% to that modelled value.

- What creates a real tension for bullish and bearish views alike is that this richer P/E sits next to analyst expectations for roughly 16.1% yearly earnings growth and forecast revenue declines of about 3.4% per year, so the valuation is being asked to reflect improving earnings metrics alongside softer top line trends.

- Some investors focused on the bullish case may lean on the DCF fair value and the earnings growth forecast to argue that the current price does not fully reflect the earnings outlook in the data.

- Others taking a more cautious stance may point to the higher than industry P/E, the 1.9% trailing margin and revenue decline forecasts when they question how much weight to give the DCF output at US$310.88.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Valero Energy's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Valero’s thin 1.9% net margin, one off US$1.1b loss and mixed quarterly profitability highlight how bumpy earnings can be across a full cycle.

If you would prefer companies where revenue and earnings show a steadier pattern through different conditions, check out stable growth stocks screener (2175 results) today to quickly focus on names with more consistent performance profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.