Varonis Systems (VRNS) Is Down 6.6% After Wave Of SaaS Transition Lawsuits Has The Bull Case Changed?

Varonis Systems, Inc. VRNS | 23.70 | +2.42% |

- Over the past year, multiple shareholder rights law firms have launched or expanded securities class actions against Varonis Systems, alleging that between February and October 2025 the company misrepresented its ability to sustain annual recurring revenue growth during its transition from on‑premises subscriptions to SaaS.

- These cases focus on claims that Varonis understated weaknesses in its legacy on‑premises and Federal businesses while highlighting its SaaS migration, with plaintiffs pointing to disappointing October 2025 results, reduced ARR guidance, product end‑of‑life decisions, and a workforce reduction as evidence of previously undisclosed operational strains.

- We’ll now examine how this wave of securities litigation and questions around the SaaS transition could affect Varonis Systems’ investment narrative.

The latest GPUs need a type of rare earth metal called Neodymium and there are only 30 companies in the world exploring or producing it. Find the list for free.

Varonis Systems Investment Narrative Recap

To own Varonis Systems, you need to believe that its data security platform can successfully complete the shift from on premises licenses to a higher quality, SaaS heavy recurring revenue base. The immediate catalyst is whether SaaS ARR growth and conversions can offset pressure in the legacy on prem and Federal segments, while the biggest risk now is that the new securities lawsuits and October 2025 reset point to deeper execution and disclosure issues around that transition.

Among recent developments, the October 28, 2025 earnings release and guidance cut sit at the center of the current litigation. Management reported a sharp term license revenue decline, reduced full year ARR expectations, announced end of life for its self hosted solution and a 5% workforce reduction, which together triggered the stock drop that plaintiff firms now cite as evidence. For investors, how Varonis manages this inflection will likely matter more than the lawsuits themselves.

Yet this renewed focus on legacy on prem and Federal renewal softness is exactly the kind of risk investors should be aware of before assuming the SaaS story is intact...

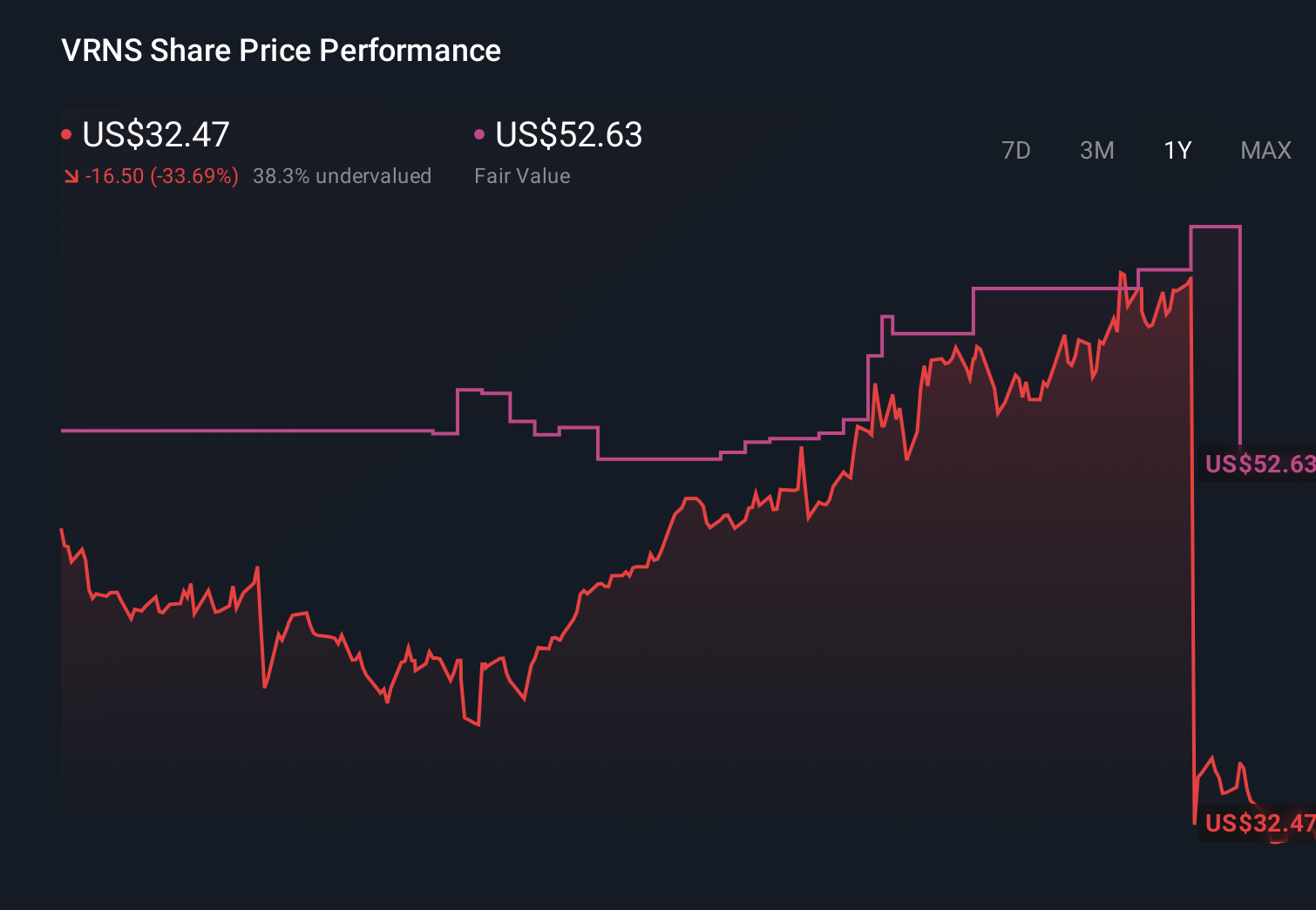

Varonis Systems’ narrative projects $911.4 million revenue and $119.3 million earnings by 2028. This requires 15.3% yearly revenue growth and about a $222 million earnings increase from -$102.9 million today.

Uncover how Varonis Systems' forecasts yield a $34.20 fair value, a 44% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already assuming about US$979 million of revenue and a small profit by 2029, but in light of the class action focus on slower SaaS conversions and weaker on prem renewals, you can see how their more cautious view of churn and margins could prove closer to reality than the upbeat consensus.

Explore 3 other fair value estimates on Varonis Systems - why the stock might be worth just $34.20!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Varonis Systems research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Varonis Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Varonis Systems' overall financial health at a glance.

Seeking Other Investments?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.