Varonis Systems (VRNS) Is Up 9.0% After AI-Fueled Beat, Buyback Completion And Raised 2026 Outlook

Varonis Systems, Inc. VRNS | 0.00 |

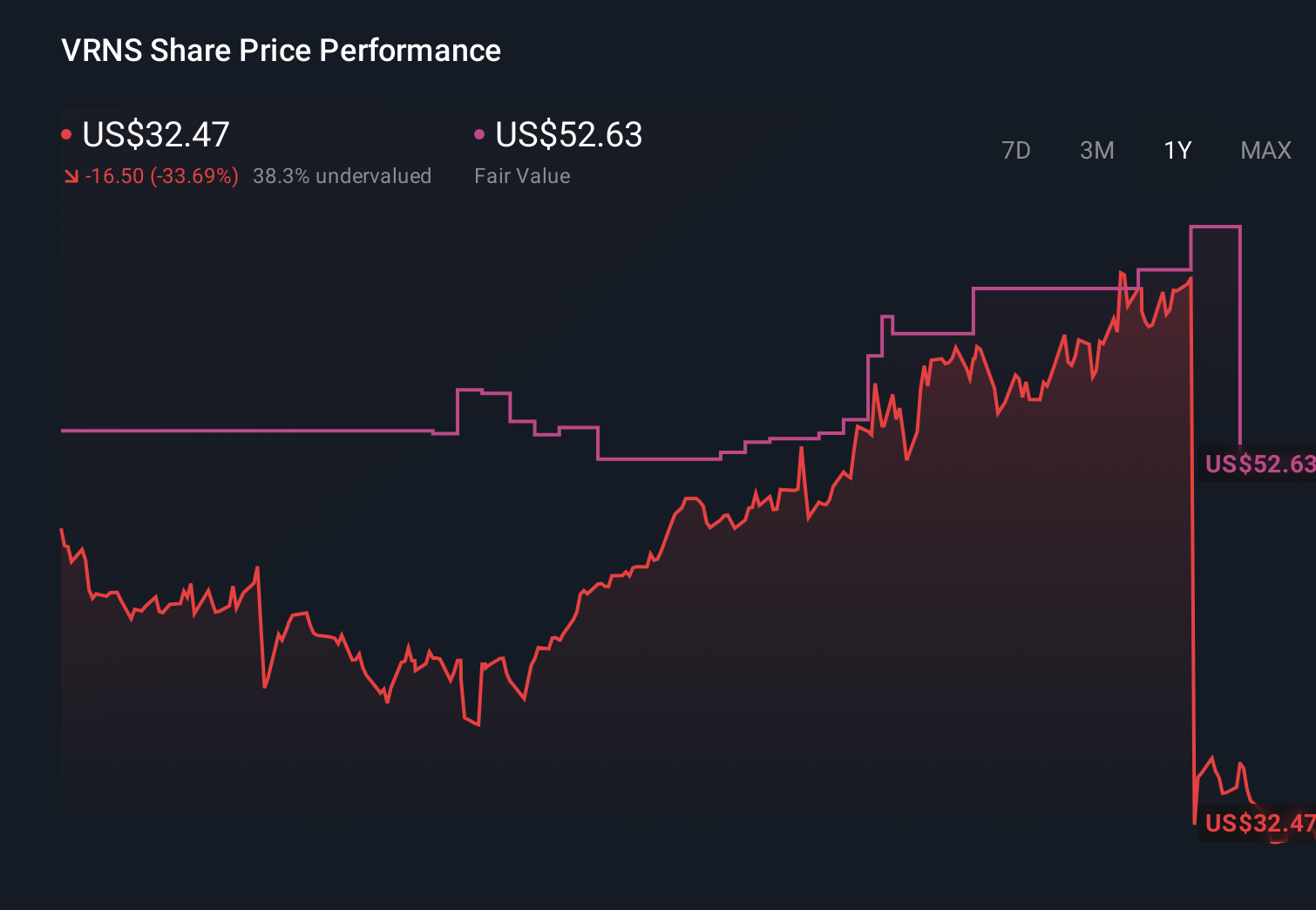

- In late April 2026, Varonis Systems reported first-quarter revenue of US$173.13 million, a similar loss per share as a year earlier, completed a US$149.99 million buyback program, and issued guidance calling for double-digit revenue growth for the second quarter and full year 2026.

- At the same time, Varonis highlighted surging demand for its AI and data security platform, including new ENS High certification in Spain and stronger SaaS adoption, reinforcing its role in securing the data that powers AI.

- We’ll now examine how this stronger-than-expected quarter and raised full-year outlook may influence Varonis’ existing AI-driven data security narrative.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Varonis Systems Investment Narrative Recap

To own Varonis today, you need to believe its AI focused data security platform can convert strong demand into a durable, higher margin SaaS business, despite ongoing losses. The latest quarter, with faster top line growth and raised 2026 revenue guidance, supports the near term catalyst of accelerating SaaS adoption, while the biggest risk remains the gap between that growth and consistent profitability. The completed buyback helps address dilution, but does not yet change the core earnings risk.

The ENS High certification in Spain looks especially relevant here, because it directly reinforces Varonis’ positioning in regulated, data sensitive environments where AI adoption is ramping. By meeting one of Europe’s stricter public sector security standards, Varonis is strengthening the case that its platform can win more mission critical workloads, which feeds into the same catalyst investors are watching most closely: can expanding AI and SaaS demand translate into more durable, higher quality revenue.

Yet while demand looks encouraging, investors should also recognize how ongoing losses and legal uncertainties could still weigh on the story...

Varonis Systems' narrative projects $992.3 million revenue and $113.1 million earnings by 2029. This requires 16.8% yearly revenue growth and a $242.4 million earnings increase from -$129.3 million today.

Uncover how Varonis Systems' forecasts yield a $33.43 fair value, a 17% upside to its current price.

Exploring Other Perspectives

The most optimistic analysts were already assuming about 18.5% annual revenue growth and US$1.0 billion sales by 2028, which contrasts sharply with concerns about on premises weakness and the announced end of life for self hosted products; with this new quarter in hand, it is worth asking how both the bullish and more cautious views might evolve from here.

Explore 3 other fair value estimates on Varonis Systems - why the stock might be worth just $33.43!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Varonis Systems research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Varonis Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Varonis Systems' overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.