Vericel (VCEL) Valuation In Focus After FDA Clears MACI Commercial Manufacturing Capacity

Vericel Corporation VCEL | 34.14 | +4.85% |

Vericel (VCEL) is back in focus after the FDA approved commercial manufacturing of its MACI cartilage repair therapy at the company’s Burlington, Massachusetts facility, a milestone tied directly to future production capacity.

Even with the FDA clearance for MACI manufacturing and recent earnings and guidance updates, Vericel’s share price has cooled, with a 1-year total shareholder return decline of 31.98%, although the 3-year total shareholder return of 14.66% still points to a better longer run.

If this FDA milestone has you thinking about where growth stories could emerge next in healthcare, it may be worth scanning 32 healthcare AI stocks as a fresh set of ideas.

With Vericel’s share price down over the past year despite recent FDA approval, revenue of US$276.26 million and net income of US$16.52 million, investors now have to ask: is there a mispricing here, or is the market already factoring in future growth?

Preferred P/E of 103.6x: Is it justified?

Vericel trades on a P/E of 103.6x, which is a rich price tag for the current earnings base at a last close of $33.71.

The P/E multiple compares the share price with earnings per share and is often used for profitable biopharma names where investors focus on earnings power alongside growth potential. A P/E above 100x usually signals that the market is paying heavily for future profitability rather than what the business is earning today.

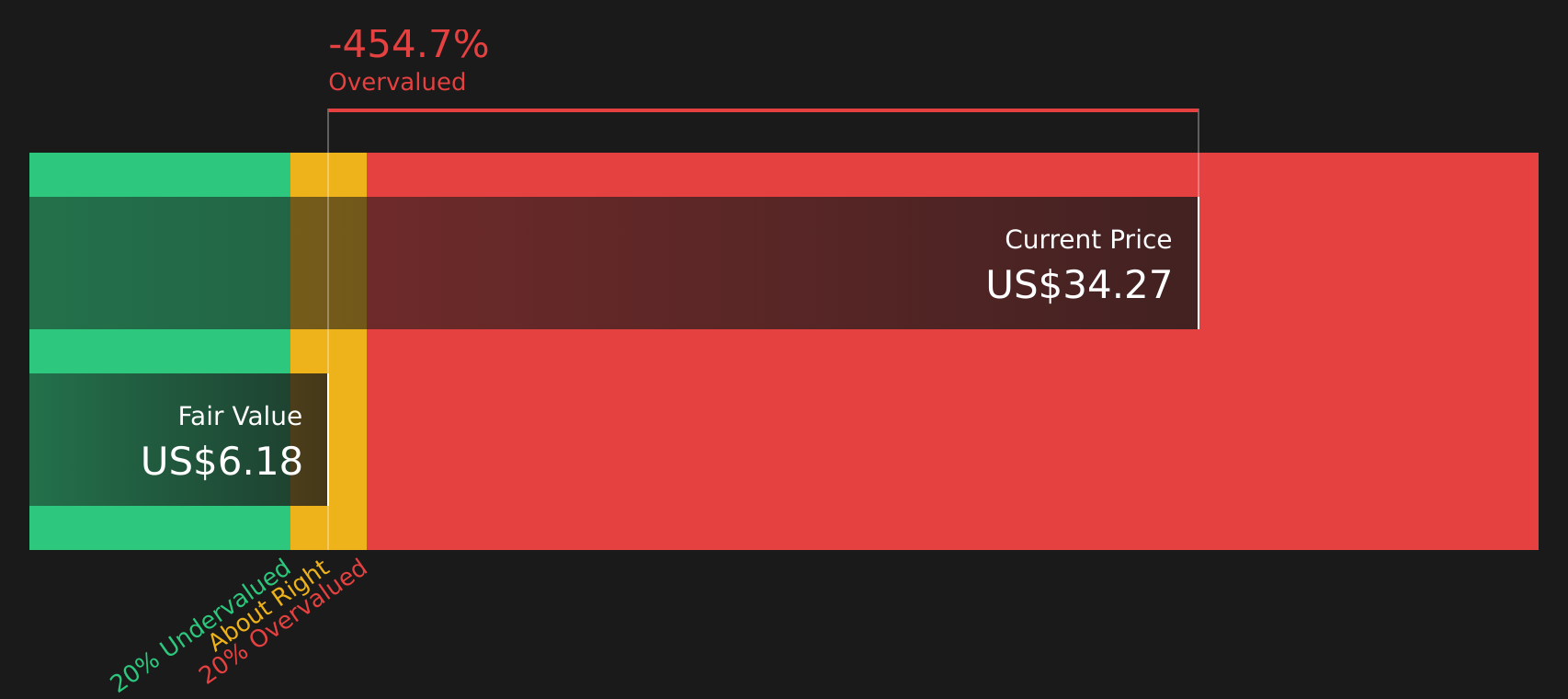

For Vericel, that high P/E sits against some strong fundamentals but also some constraints. Earnings grew 59.4% over the past year and have been compounding over the last five years. Analysts expect earnings growth of 32.7% per year to outpace the broader US market. At the same time, return on equity is 4.7%, which is considered low, and the SWS DCF model estimates future cash flow value of just $0.66 per share compared to the current $33.71 share price. This points to a large premium over that modelled cash flow value.

Relative to peers, the contrast is clear. Vericel’s 103.6x P/E is far above the US Biotechs industry average of 21x and the peer average of 17.3x. It is also well above the estimated fair P/E of 22.5x that the SWS fair ratio suggests the market could move toward if expectations cool.

Result: Price-to-Earnings of 103.6x (OVERVALUED)

However, you still have to weigh risks, such as any setback in commercializing MACI at scale or slower uptake of burn therapies affecting revenue and earnings momentum.

Another view: DCF paints a very different picture

While the 103.6x P/E suggests the market is paying up for Vericel, our DCF model comes out far more cautious, with future cash flows estimated at $0.66 per share versus the current $33.71 price. That implies Vericel screens as heavily overvalued on this approach. Which signal do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Vericel for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of high expectations and valuation gaps leaves you undecided, check the numbers yourself and move quickly to form your own stance; 3 key rewards can help highlight what some investors already view as potential upside.

Looking for more investment ideas?

If this story has you rethinking where your capital works hardest, do not stop here. Broaden your watchlist with fresh ideas that fit your style.

- Spot potential mispricings early by scanning our 49 high quality undervalued stocks, which pairs quality fundamentals with a price that may not fully reflect them.

- Strengthen your portfolio’s income stream using our 16 dividend fortresses, focused on higher yielding companies with an emphasis on resilience.

- Sleep easier by filtering for steadier names through the 63 resilient stocks with low risk scores, which screens for companies with lower overall risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.