Vertex Pharmaceuticals (VRTX) Valuation After 2025 Earnings Strength And 2026 Guidance For CF And Gene Editing Growth

Vertex Pharmaceuticals Incorporated VRTX | 438.95 | -1.20% |

Vertex Pharmaceuticals (VRTX) is back in focus after reporting full year 2025 results and issuing 2026 revenue guidance tied to its cystic fibrosis franchise and newer products CASGEVY, JOURNAVX, and ALYFTREK.

Vertex’s latest earnings and 2026 revenue guidance have landed against a backdrop of steady gains, with a 90 day share price return of 6.38% and a five year total shareholder return of 121.62% signaling momentum built over the longer term.

If Vertex’s progress in CF and gene editing has your attention, it could be a good moment to see what else is emerging through our 24 healthcare AI stocks as a broader healthcare opportunity set.

With shares up modestly over the past year, trading below the average analyst price target and with an intrinsic value estimate suggesting a wider discount, you have to ask: Is Vertex still underappreciated, or is the market already assuming years of future growth?

Most Popular Narrative: 7.7% Undervalued

At $465.02, the most followed narrative pegs Vertex’s fair value at about $504, suggesting a gap that rests on specific growth and margin assumptions.

Commercial success and broad payer coverage for recent launches, particularly JOURNAVX and CASGEVY, are setting the stage for larger market uptake and eventual margin improvement as early launch support programs unwind and operational leverage is realized, positively impacting net margins and earnings.

Curious what kind of revenue path and profit profile need to line up for that valuation gap to close? The narrative focuses on steady top line compounding, firmer margins and a richer future earnings multiple than the broader biotech group. If you want to see exactly how those moving pieces fit together, the full story lays out the numbers in detail.

Result: Fair Value of $504.04 (UNDERVALUED)

However, there is still the possibility that heavier spending on new programs or slower uptake outside cystic fibrosis could pressure margins and challenge the underappreciated story.

Another View: Earnings Multiple Flags a Different Risk

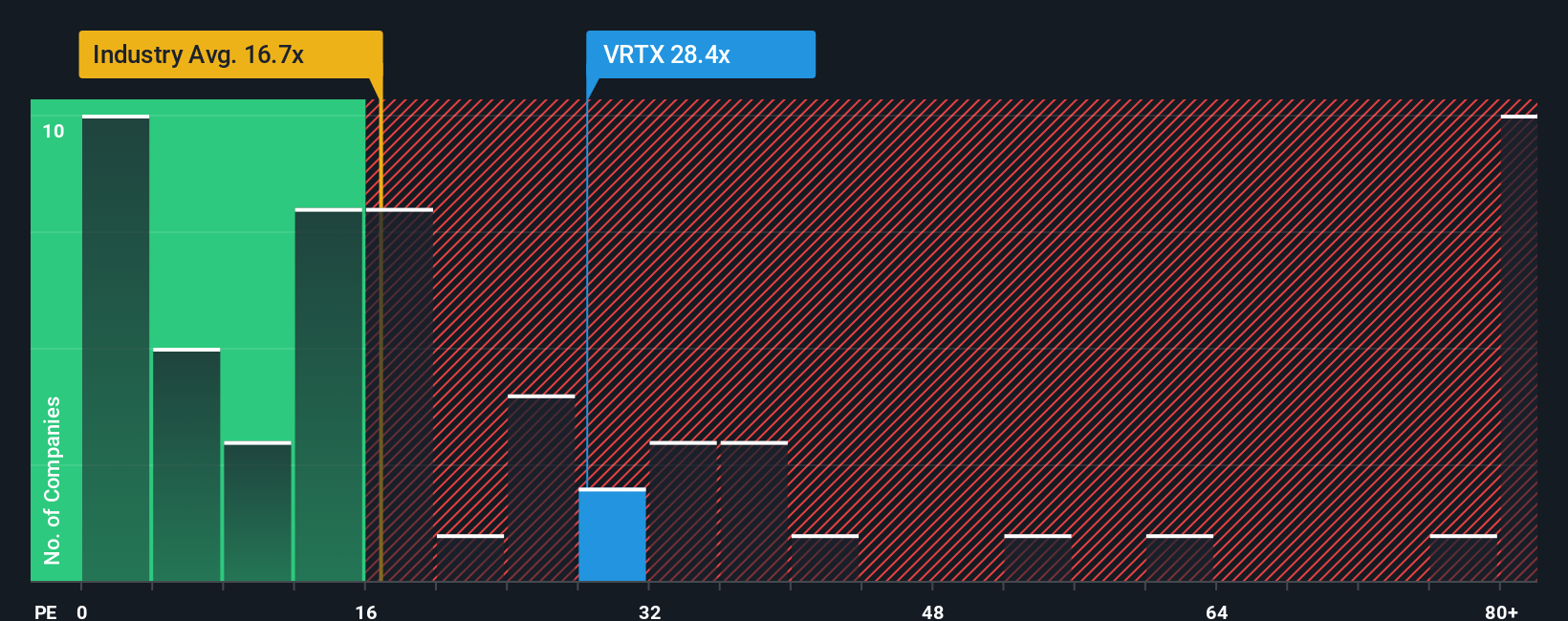

While the narrative and intrinsic value work point to upside, the current P/E of 32.1x paints a more cautious picture. It sits above the US Biotechs industry at 22.1x and above the 29.9x fair ratio, yet below the 40.2x peer average. Where does that leave you?

Those gaps suggest the market already prices in stronger earnings than the sector overall, but not as aggressively as closer peers, while still running ahead of the fair ratio the market could move toward over time. The question is whether you see that as valuation risk building, or a premium you are comfortable paying for Vertex’s profile. See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Vertex Pharmaceuticals Narrative

If you look at these numbers and reach a different conclusion, or just prefer to test your own assumptions directly, you can build a personalised Vertex view in minutes, starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Vertex Pharmaceuticals.

Looking for more investment ideas?

If Vertex has sharpened your focus, do not stop here. Take a few minutes to scan wider opportunities that could round out your watchlist and portfolio.

- Spot potential bargains early by checking companies our screener tags as screener containing 23 high quality undiscovered gems before they appear on everyone else's radar.

- Strengthen your core holdings by reviewing the solid balance sheet and fundamentals stocks screener (45 results) that pair financial resilience with fundamental support.

- Lock in more reliable income streams by scanning the 16 dividend fortresses that emphasise higher yields with a focus on durability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.