Victorias Secret (VSXY) Stock Valuation After Strong Q1 Beat And Upgraded Guidance

Victoria's Secret & Company VSXY | 0.00 |

Victoria's Secret (VSXY) is in focus after a busy start to June, with Q1 results beating consensus expectations, raised full year guidance, ongoing share repurchases, and proxy advisors backing the full board slate.

The stock’s recent run has been rapid, with a 69.2% 1 month share price return and 75.6% 3 month share price return, contributing to a very large 1 year total shareholder return of around 3x. Recent earnings beats, upgraded guidance, share repurchases and broad shareholder support have all helped shift sentiment and highlight how quickly perceptions of risk and growth potential can change around a single quarter.

If Victoria's Secret’s surge has you reassessing where momentum could build next, it may be worth scanning other retail and consumer stories via the 20 top founder-led companies

With VSXY up nearly 3x over 1 year and trading at about a 12% discount to the US$88.11 analyst target, plus an indicated 43% intrinsic discount, is there still a mispricing here, or is the market already banking on future growth?

Most Popular Narrative: 20.2% Overvalued

The most followed narrative pegs Victoria's Secret fair value at $65.56, below the last close of $78.78. This frames the recent share price surge in a very different light.

The ongoing transformation of Victoria's Secret toward inclusivity, body positivity, and enhanced storytelling continues to resonate with younger customers and drive new customer acquisition, especially among the 18-44 demographic, supporting sustained revenue and market share growth.

Read the complete narrative. Read the complete narrative.

Want to see what is baked into that $65.56 fair value? The narrative leans on richer margins, steadier revenue progress, and a different future earnings multiple. The full set of assumptions is where the real story sits.

Result: Fair Value of $65.56 (OVERVALUED)

However, higher tariffs and ongoing reliance on mall based stores could still pressure margins and sales, challenging the earnings story behind that $65.56 fair value.

Another View: DCF Sees Room Above the Current Price

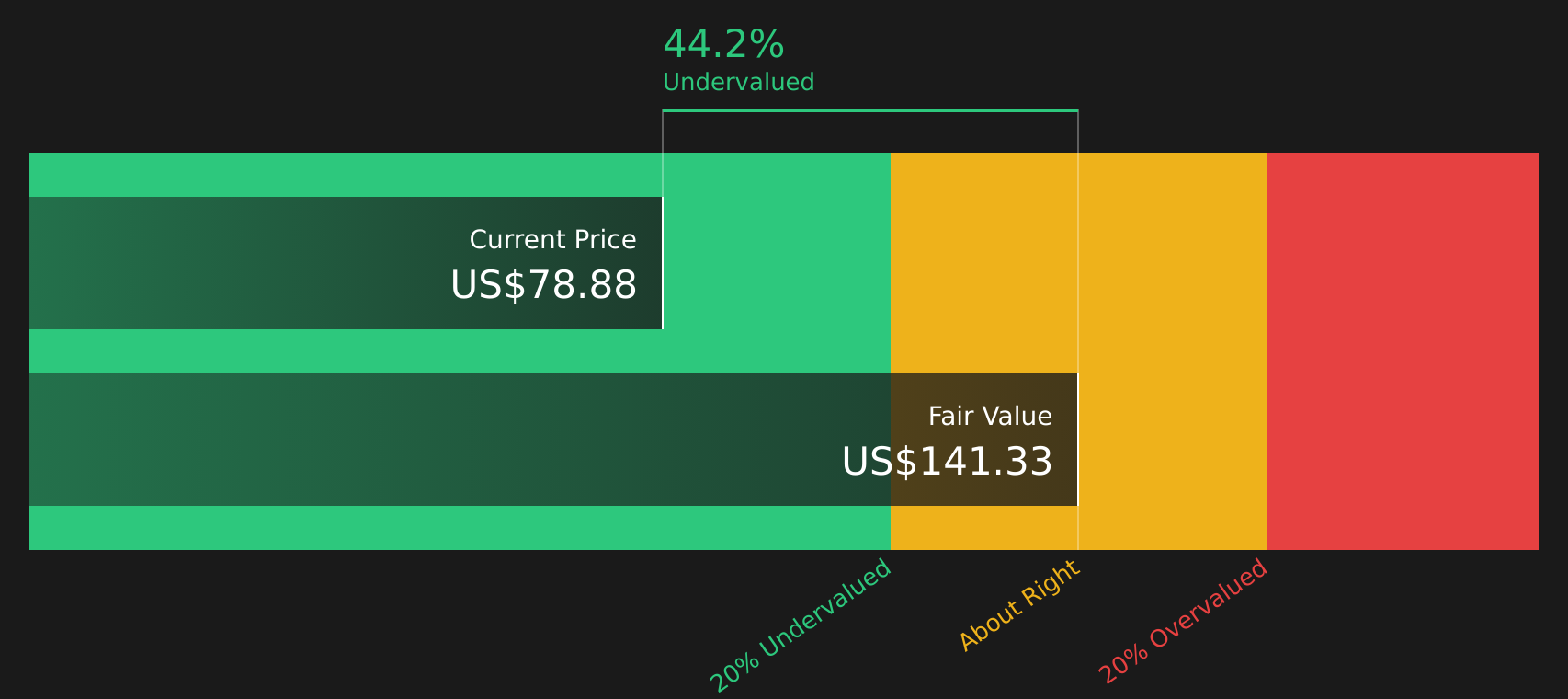

Analysts’ $65.56 fair value suggests Victoria's Secret is about 20.2% overvalued, but the SWS DCF model points the other way, with an estimated future cash flow value of $138.62 per share, around 43.2% above the current $78.78 price. Which story do you think better reflects the risk and reward you see?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Victoria's Secret for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment pulling in different directions, this is the moment to move quickly, test the assumptions yourself, and weigh both upside and downside using the 3 key rewards and 4 important warning signs

Looking for more investment ideas?

If Victoria's Secret has sharpened your focus on where capital could work harder next, do not stop here. Broaden your watchlist before the next moves get crowded.

- Target resilience first by scanning companies in the 67 resilient stocks with low risk scores that align with your comfort level on volatility and downside.

- Hunt for quality at a discount using the 46 high quality undervalued stocks to spot stocks where fundamentals and price appear out of sync.

- Build a watchlist of potential standouts by searching the screener containing 20 high quality undiscovered gems before the wider market catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.