Viridian Therapeutics (VRDN): What Recent Volatility Means for Shareholders and Valuation

Viridian Therapeutics, Inc. VRDN | 0.00 |

Viridian Therapeutics (VRDN) has caught investor attention after recent trading swings, with the stock making notable moves over the past month. Many are watching to see how the company’s pipeline could affect future performance.

After a steep drop in the last session, Viridian Therapeutics' share price is still up 12% for the past month and 25% over 90 days. This reflects renewed interest in its growth story. However, the 1-year total shareholder return stands at -6%, suggesting that while momentum has picked up recently, longer-term holders have faced headwinds.

If you’re watching biotech momentum build or want to widen your search, now is a great time to discover fast growing stocks with high insider ownership

With the stock trading well below analyst price targets and rapid recent gains, the key question is whether Viridian Therapeutics remains undervalued or if the market is already factoring in all of its future growth potential.

Price-to-Book Ratio of 5.5x: Is it justified?

Viridian Therapeutics currently trades at a price-to-book ratio of 5.5x, significantly higher than both the industry and its peers, despite recent price swings. This suggests the market is assigning a substantial premium to the stock relative to its accounting book value.

The price-to-book ratio compares a company’s stock price to its book value per share and reflects investor sentiment about growth prospects and asset quality. For biotechs, a high ratio can indicate high expectations for future breakthroughs and commercial success, even if current profitability is lacking.

However, when measured against the broader US Biotechs industry average of 2.6x and a peer group average of 3.8x, Viridian Therapeutics stands out as expensive by this metric. Such a premium indicates the market expects major upside, but it also adds pressure for the company to deliver on growth and execution.

Result: Price-to-Book Ratio of 5.5x (OVERVALUED)

However, rapid revenue growth and optimistic price targets may not shield Viridian Therapeutics if clinical setbacks or broader biotech market volatility affect sentiment.

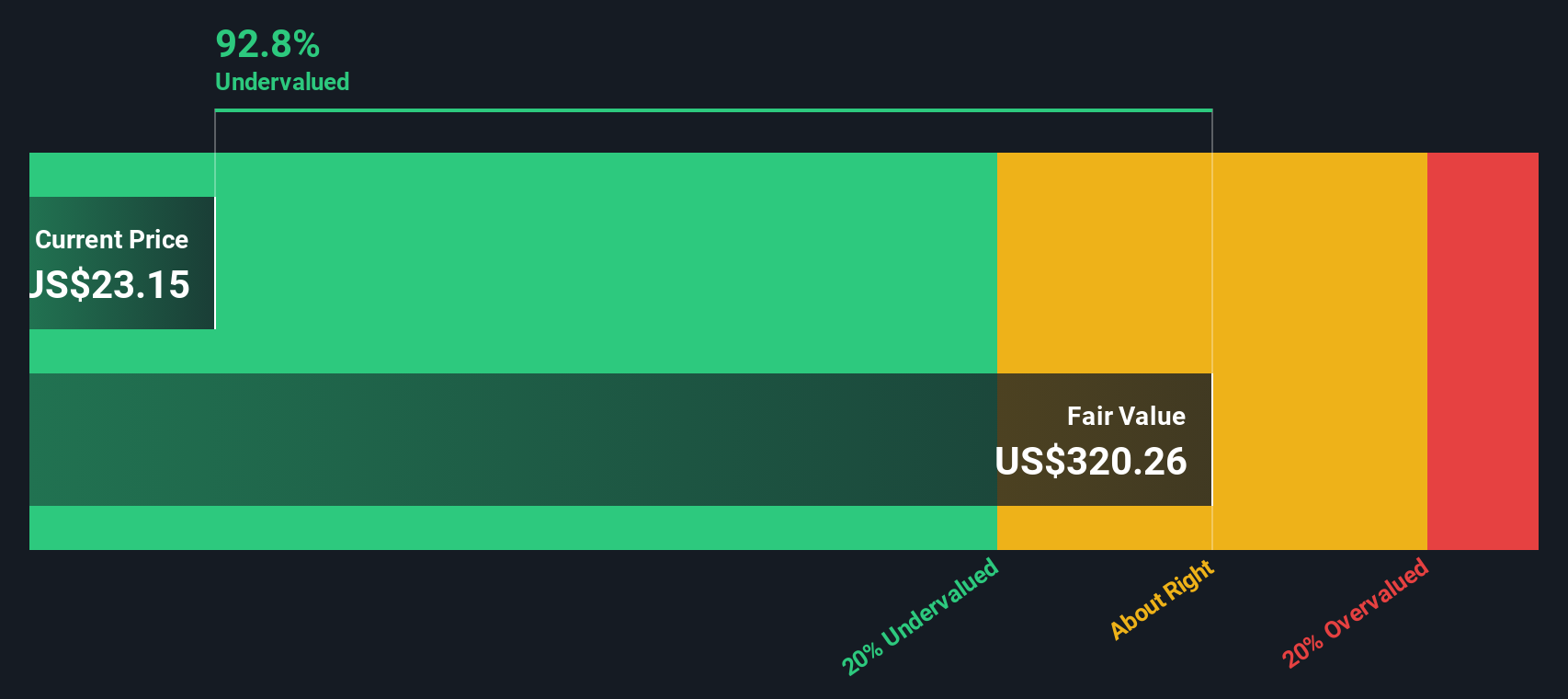

Another View: A Discounted Cash Flow Perspective

While Viridian Therapeutics appears expensive on a price-to-book basis, our DCF model provides a different perspective. The SWS DCF model estimates fair value at $328.77, which is much higher than the current share price of $21.9. This suggests the market may be undervaluing future growth potential. Could this disconnect indicate opportunity or simply reflect uncertainty?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Viridian Therapeutics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Viridian Therapeutics Narrative

If you have your own perspective or wish to dig deeper into the numbers, you can build a personalized view in just a few minutes, so go ahead and Do it your way.

A great starting point for your Viridian Therapeutics research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Take the next step toward smarter investing by tapping into fresh stock opportunities you won’t want to miss. Use the Simply Wall Street Screener to find tomorrow’s leaders today.

- Target attractive yields and steady cash flow when you check out these 17 dividend stocks with yields > 3% with impressive dividend histories and strong income potential.

- Ride the wave of AI-driven innovation by checking these 26 AI penny stocks that are pushing the boundaries of machine intelligence and transforming top sectors.

- Benefit from hidden value by reviewing these 875 undervalued stocks based on cash flows, where strong fundamentals could mean significant upside before the crowd catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.