Vishay Precision Group (VPG) Joins Russell Indexes But Is The Valuation Already Priced In

Vishay Precision Group, Inc. VPG | 0.00 |

Vishay Precision Group (VPG) has been added to several Russell growth indices, including the 2000, 2500, 3000, small cap, and microcap benchmarks, a development that can reshape how many investors access the stock.

Recent index additions come after a sharp share price move in Vishay Precision Group, with the stock at US$113.49 and a 90 day share price return of 127.43%. The 1 year total shareholder return is 293.24%, pointing to very strong longer term momentum despite a softer 30 day share price return of 7.48%.

If you are looking for other ideas in the measurement, sensing, and industrial technology space, it is worth checking out a curated list of 30 robotics and automation stocks.

Bulls point to Vishay Precision Group's index additions and recent momentum, while bears highlight the gap to analyst targets and valuation risk after a rapid move. Which side does the current valuation actually support?

Most Popular Narrative: 20% Overvalued

The most followed valuation narrative currently points to a fair value of $94.67 for Vishay Precision Group, compared with the last close at $113.49, setting up a clear tension between model and market.

The analysts have a consensus price target of $94.67 for Vishay Precision Group based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $109.0, and the most bearish reporting a price target of just $77.0.

Want to understand why a business growing earnings this quickly still screens as overvalued in this narrative? The key assumptions sit in a tight balance between projected revenue growth, a step change in profit margins, and a future earnings multiple that is higher than the sector benchmark. Curious which of those levers carries the most weight in getting to that $94.67 number?

Result: Fair Value of $94.67 (OVERVALUED)

However, Vishay Precision Group still faces clear risks, including dependence on humanoid robotics customer rollouts and pressure from tariffs and trade policy that could weigh on margins.

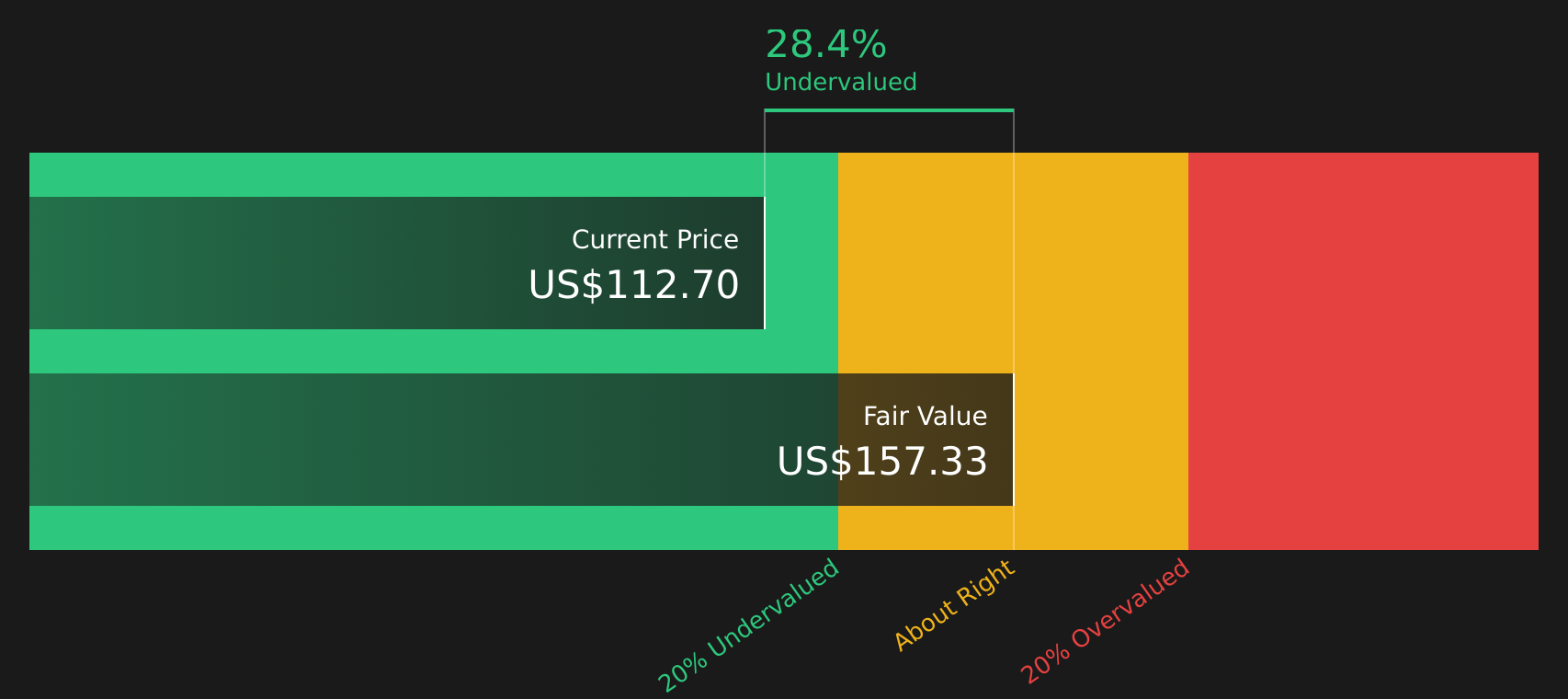

Another View: Vishay Precision Group Through a Cash Flow Lens

While the analyst narrative frames Vishay Precision Group as about 20% overvalued at a fair value of $94.67 versus a $113.49 share price, the SWS DCF model tells a different story. On that approach, VPG screens as trading below an estimated future cash flow value of $157.58, which points to upside instead of downside. Which set of assumptions do you find more convincing?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Vishay Precision Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split on Vishay Precision Group, it makes sense to review the numbers for yourself, weigh the concerns against the potential, and see how the balance of 3 key rewards and 2 important warning signs fits with your own view.

Looking for more investment ideas beyond Vishay Precision Group?

If Vishay Precision Group has sharpened your interest, do not stop here. Broaden your watchlist with other focused ideas that could suit your own investing style.

- Pinpoint potential mispricings by scanning a focused set of 44 high quality undervalued stocks that pair fundamental strength with discounted valuations.

- Strengthen your income stream by reviewing 9 dividend fortresses designed for investors who prioritize dependable cash payouts.

- Dial down portfolio risk by checking 73 resilient stocks with low risk scores that emphasize resilient balance sheets and steadier return profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.