Vishay Precision Group (VPG) Joins Russell Indexes On Beat Results As Fair Value Debate Grows

Vishay Precision Group, Inc. VPG | 0.00 |

Vishay Precision Group (VPG) has just been added to several Russell growth and small cap indices, a shift that increases visibility with institutional investors and coincides with quarterly results that surpassed earnings and revenue expectations.

Despite the latest 1-day share price return being down 15.57% at US$121.59, Vishay Precision Group has seen very strong momentum over a longer period, with a 90-day share price return of 171.59% and a 1-year total shareholder return of 311.05%. This indicates sentiment has shifted quickly following index inclusions and recent results.

If Vishay Precision Group’s surge has you rethinking where growth might appear next, this could be a good moment to scan for opportunities in 35 power grid technology and infrastructure stocks

With Vishay Precision Group now included in several Russell growth indices and trading at an intrinsic discount of about 21% alongside rapid recent share gains, is the stock mispriced value, or is the market already banking on stronger future growth?

Most Popular Narrative: 28.4% Overvalued

Vishay Precision Group’s most followed narrative pegs fair value at $94.67, well below the last close at $121.59. This sets up a tension between analyst assumptions and recent price strength.

The strong sequential growth in bookings and a positive book-to-bill ratio across key segments indicate building demand for VPG's precision sensors and measurement products, positioning the company to benefit as global Industry 4.0 adoption and automation trends accelerate, likely supporting top-line revenue growth. New order momentum in cutting-edge markets such as humanoid robotics and beta installations for high-performance testing systems (e.g., UHTC for aerospace and energy) show VPG's entry into high-growth, high-margin niches, which can meaningfully expand gross margin and improve earnings quality as these end-markets scale.

Curious how Vishay Precision Group gets to a higher fair value than the analyst target and still screens as overvalued? The narrative leans on faster earnings compounding, a sharp margin reset, and a rich future profit multiple that would usually be reserved for larger growth stocks. Want to see which assumptions need to hold for that to stack up over time?

Result: Fair Value of $94.67 (OVERVALUED)

However, investors in Vishay Precision Group still face execution risk if humanoid robotics demand or customer production ramp ups fall short, and if restructuring efforts encounter disruptions.

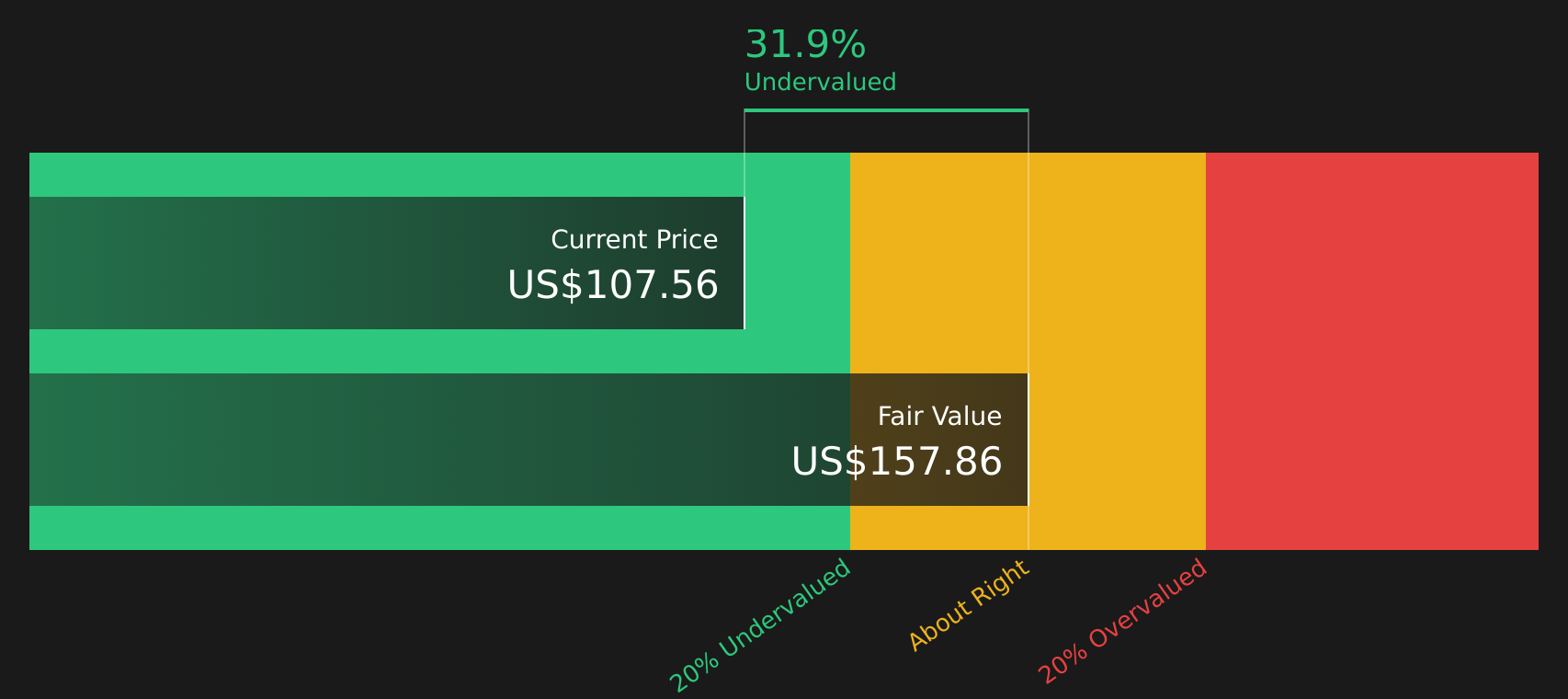

Another View: Vishay Precision Group Through A Cash Flow Lens

While the most popular Vishay Precision Group narrative points to a fair value of $94.67 and labels the stock as overvalued, the SWS DCF model comes to a different conclusion. At a fair value estimate of $154.76, VPG screens as undervalued versus the current $121.59 price. This raises the question of which set of assumptions you find more convincing.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Vishay Precision Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 42 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around Vishay Precision Group have you unsure which side to lean toward, this is the moment to review the data yourself, consider both the risks and the potential upside, and then weigh the 3 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Vishay Precision Group?

If Vishay Precision Group has sharpened your focus on where growth and value might appear next, do not stop here. Broaden your watchlist with fresh, data driven ideas.

- Target potential future upside by reviewing companies that currently screen as 42 high quality undervalued stocks based on solid fundamentals and pricing that has not yet fully reflected their potential.

- Strengthen portfolio resilience by focusing on businesses highlighted in the 75 resilient stocks with low risk scores, where balance sheets and risk profiles aim to limit unpleasant surprises.

- Look ahead of the crowd by checking the screener containing 18 high quality undiscovered gems that may not be widely followed but still show strong underlying quality signals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.