Vistance Networks (VISN) Valuation Check After RUCKUS Expands Pro AV Switches And AV Partnerships

Gyroscope Therapeutics Holdings plc VISN | 18.73 | +2.07% |

Vistance Networks (VISN) is back on investors' radar after its RUCKUS Networks unit expanded the Pro AV ICX switch lineup, updated AV-focused management platforms, and aligned with Crestron and the SDVoE Alliance.

The recent Pro AV ICX expansion and new alliances arrive after a mixed stretch for the shares, with a 6.43% 90 day share price return but a softer year to date move. At the same time, the 1 year total shareholder return of 245.42% points to strong longer term momentum that investors will weigh against current expectations.

If this kind of networking story has your attention, it could be a good time to see which other tech names are gaining interest through high growth tech and AI stocks.

With a 1 year total return of about 245% but a softer move year to date, and analysts seeing room above the recent US$17.72 close, is Vistance still mispriced or are markets already baking in future growth?

Most Popular Narrative: 26.9% Undervalued

At a last close of $17.72 versus a narrative fair value of $24.25, the widely followed view frames Vistance as trading at a sizeable discount.

The profit margin was reduced from 84.43% to 5.46%, representing a very large downward change in the long run profitability assumption that feeds into the valuation. The Future P/E increased from about 123x to a very large multiple above 2,000x, showing a much higher assumed valuation multiple applied to future earnings in the updated estimate.

Curious why a modest margin profile is paired with a very large future earnings multiple in this fair value math? The narrative leans on specific growth, profitability and discount rate assumptions that are anything but ordinary. If you want to see how those moving parts combine to support a $24.25 figure, the full story is where the details surface.

Result: Fair Value of $24.25 (UNDERVALUED)

However, those upbeat assumptions can easily be challenged if DOCSIS 4.0 rollouts slow or if customer concentration in ANS and RUCKUS leads to more volatile revenue and margin pressure.

Another View: Earnings Ratio Sends a Different Signal

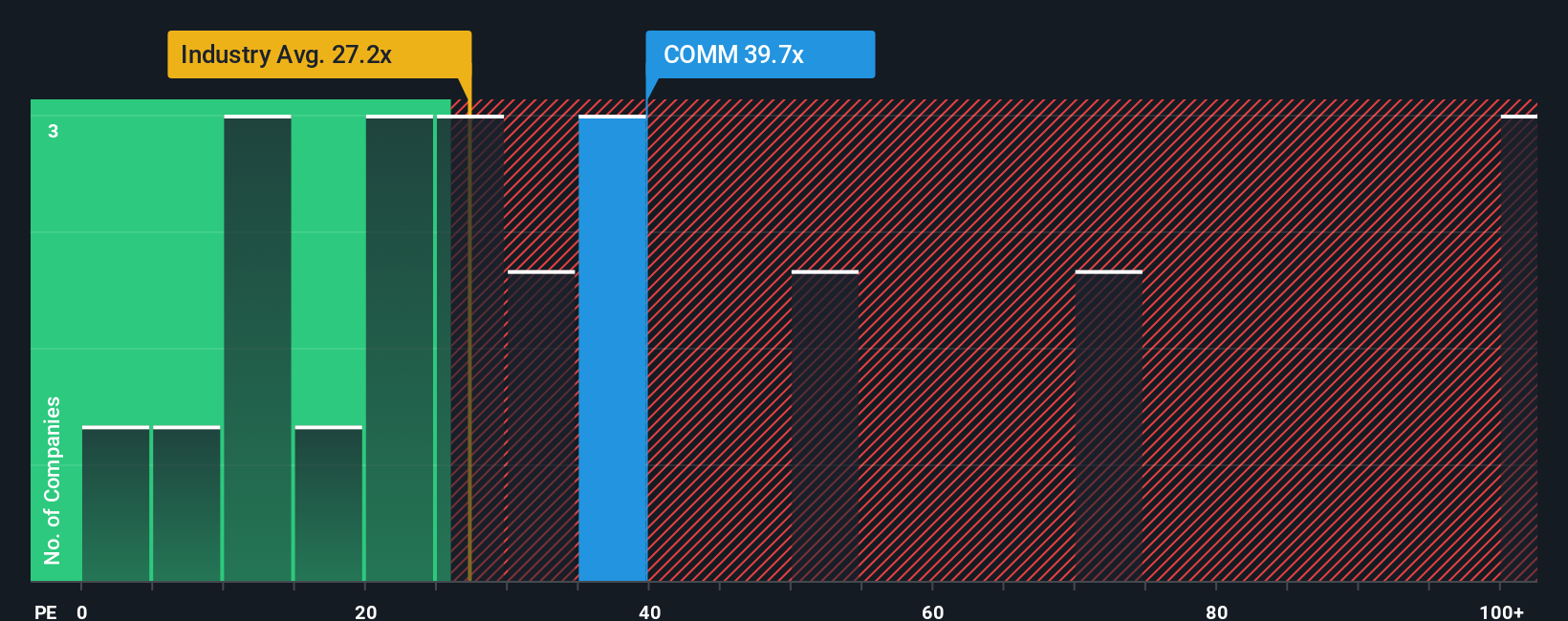

While the narrative fair value of $24.25 suggests Vistance Networks is 26.9% undervalued, the market’s current P/E of 13.7x tells a more cautious story. That multiple sits below the US Communications average of 31.8x and the peer average of 27.5x. However, it remains well above the fair ratio of 3.6x, which points to a higher valuation risk if expectations reset.

When one model indicates potential upside but the earnings ratio and fair ratio gap point to possible overpricing, which signal do you weigh more heavily for your own thesis?

Build Your Own Vistance Networks Narrative

If you see the numbers differently or prefer to test your own assumptions, you can build a tailored view in minutes with Do it your way.

A great starting point for your Vistance Networks research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Vistance has sparked your interest, do not stop here, the Simply Wall St Screener can quickly surface fresh ideas that match what you care about most.

- Target income potential with these 11 dividend stocks with yields > 3% that focus on established payouts above 3% and see which names merit a closer look.

- Spot emerging opportunities in artificial intelligence by scanning these 30 AI penny stocks and compare how different businesses are exposed to this theme.

- Hunt for mispriced opportunities using these 860 undervalued stocks based on cash flows where the current share price sits below estimated cash flow based value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.