W. P. Carey (WPC) Stock Could Be 6.6% Undervalued On Its Reinvestment Narrative

W. P. Carey Inc. WPC | 0.00 |

W. P. Carey (WPC) has attracted fresh attention after recent share price moves, with the stock trading around $72.23. For investors, the question is how its current valuation lines up with recent fundamentals.

Recent trading has been choppy, with the share price down 5.16% over the last day and 4.76% over the past week. However, W. P. Carey still shows an 11.36% year to date share price return and a 19.89% total shareholder return over one year, suggesting momentum has cooled in the short term but remains positive over a longer horizon.

If this kind of move has you thinking about what else is out there, it could be a good time to size up 34 power grid technology and infrastructure stocks

With W. P. Carey trading around $72.23 and showing a value score of 4 alongside a reported intrinsic discount of roughly 54%, the key question is whether the stock is still undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 6.6% Undervalued

On the latest numbers, the most followed narrative pegs W. P. Carey’s fair value at $77.36 versus a last close of $72.23, framing the current discount around its cash flow potential and balance sheet capacity.

Active balance sheet management, including high spreads (100-150 bps) between disposition and investment cap rates, allows accretive reinvestment from non-core asset sales (e.g., self-storage) into higher-yielding, long-term net lease assets, providing a catalyst for net margin expansion and AFFO growth. International diversification, with increasing deal flow and lower funding costs in Europe (borrowing approximately 125-150 bps below U.S. rates), mitigates localized economic risks and enhances portfolio cash flow stability, smoothing revenue and earnings volatility.

Want to see what sits behind that valuation gap for W. P. Carey? The narrative leans heavily on a specific revenue glide path, margin lift, and future earnings multiple that are anything but generic.

Result: Fair Value of $77.36 (UNDERVALUED)

However, the narrative around W. P. Carey could be challenged if tenant credit issues hit single tenant leases, or if asset sales slow and limit reinvestment capacity.

Another Take On W. P. Carey Valuation

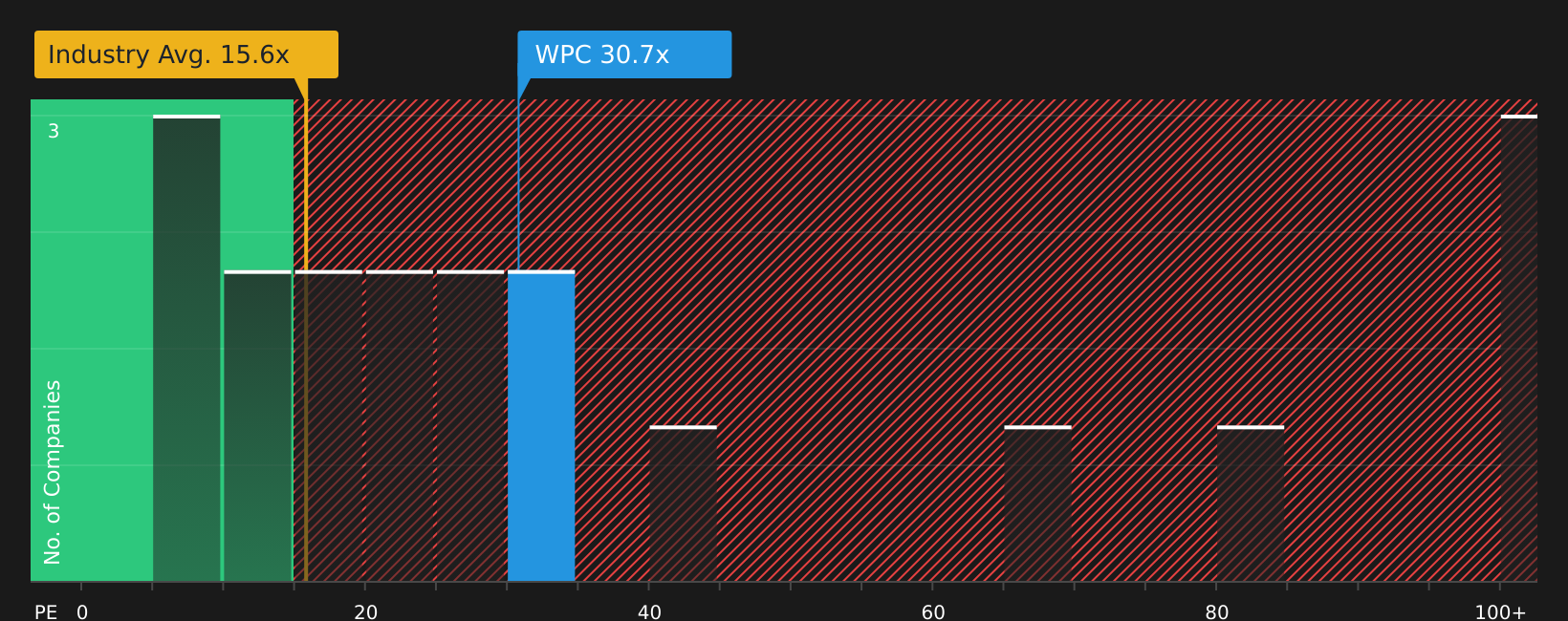

The earlier narrative leans on future cash flows and analyst targets to argue W. P. Carey stock is around 6.6% undervalued. On current numbers, though, the P/E of 31.1x looks expensive next to the Global REITs average of 15.6x, even if it sits below a fair ratio of 36.2x and a peer average of 77.8x. Is the higher multiple a sign of quality being rewarded, or a thinner margin of safety than the discount labels suggest?

To see how this price stacks up against earnings power in more detail, take a look at the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Mixed messages on W. P. Carey so far? Act while the data is fresh, consider both the caution and the optimism, and ground your own view with the 3 key rewards and 2 important warning signs

Looking For More Investment Ideas Beyond W. P. Carey?

If you are weighing what to do next after reviewing W. P. Carey, do not stop here. Broaden your watchlist with a few targeted ideas.

- Target dependable cash generators by checking out screener containing 20 high quality undiscovered gems before other investors pay attention to them.

- Strengthen your downside protection and focus on capital resilience with the 65 resilient stocks with low risk scores in just a few minutes.

- Zero in on companies that combine financial flexibility with disciplined balance sheets by scanning the solid balance sheet and fundamentals stocks screener (48 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.