W. R. Berkley (WRB) Stock Valuation Check After Mixed Recent Returns

W. R. Berkley Corporation WRB | 0.00 |

Why W. R. Berkley (WRB) is Drawing Fresh Investor Attention

W. R. Berkley (WRB) has been back on investors’ radar after recent trading left the stock with a mixed return profile, including a decline over the past year alongside solid multi year total returns.

Recent trading has been choppy, with a 1 day share price return of 1.08% and a 1 month share price return of 4.34%. The 1 year total shareholder return is down 4.36%, compared with much stronger 3 and 5 year total shareholder performance. This indicates that longer term momentum has been stronger than the recent pullback.

If you are reviewing insurers like W. R. Berkley and want to widen your search, it can be useful to scan for companies with resilient cash flows and balance sheets using the 20 top founder-led companies

With annual revenue growth running at 0.5%, net income growth at 0.9% and an internal intrinsic value estimate suggesting a 44% discount, is WRB offering a genuine entry point, or is the market already pricing in future growth?

Most Popular Narrative: 10% Undervalued

Compared with the last close at $68.27, the most followed narrative points to a fair value of about $68.33, putting W. R. Berkley slightly below that mark and framing recent weakness against expectations for resilient earnings and margins.

Prudent capital management, shown by a growing investment portfolio benefitting from higher new money yields and conservative reserving, is increasing investment income and book value per share, laying a foundation for higher long-term earnings and the potential for resumed share buybacks.

Curious what sits behind that earnings story? The narrative leans heavily on steady margins, measured revenue assumptions, and a future valuation multiple that is not typical for this sector.

Result: Fair Value of $68.33 (UNDERVALUED)

However, this hinges on pricing discipline and loss trends, with softer commercial and reinsurance rates, or claim costs rising faster than premiums, both capable of undermining that earnings story.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another Angle on Valuation

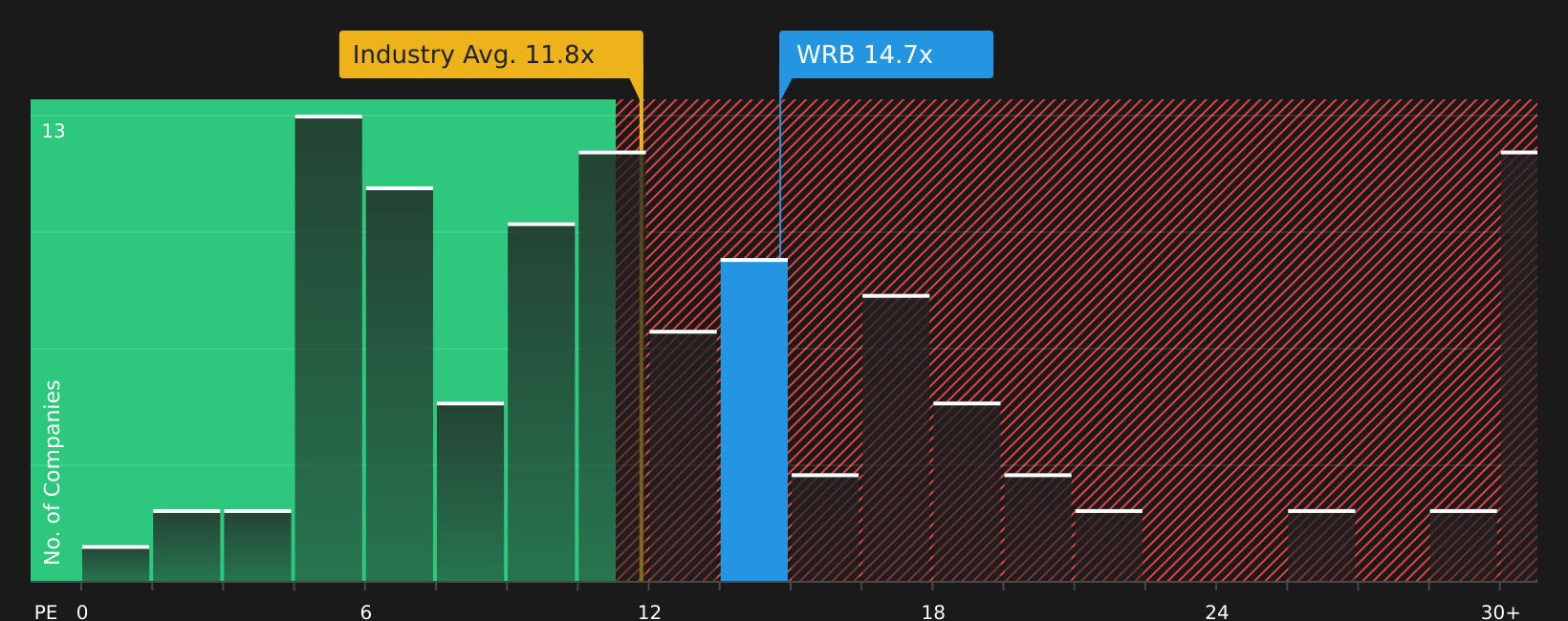

While the SWS DCF model flags WRB as undervalued, trading at $68.27 versus an estimated future cash flow value of $121.92, earnings based comparisons tell a different story. The current P/E of 14.2x is higher than the US Insurance industry and peer average of 11.3x, and above a fair ratio of 10.5x. This points to less room for error if growth or margins disappoint. Which signal do you weigh more heavily?

Next Steps

It is uncertain whether this mixed picture leaves WRB cheap or fairly priced. Act while the data is fresh and review the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop here, you risk missing other stocks that fit your style, so take a few minutes to turn WRB’s insights into a broader watchlist.

- Spot potential value opportunities early by scanning 44 high quality undervalued stocks that combine reasonable pricing with solid fundamentals.

- Prioritize income and stability by checking out 8 dividend fortresses that focus on higher yields with an emphasis on resilience.

- Aim for staying power in tougher markets by reviewing 70 resilient stocks with low risk scores built around stronger balance sheets and lower risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.