Warrior Met Coal’s (HCC) Insider Sales Amid Rich Valuation: What Do They Signal About Risk‑Reward?

Warrior Met Coal, Inc. HCC | 0.00 |

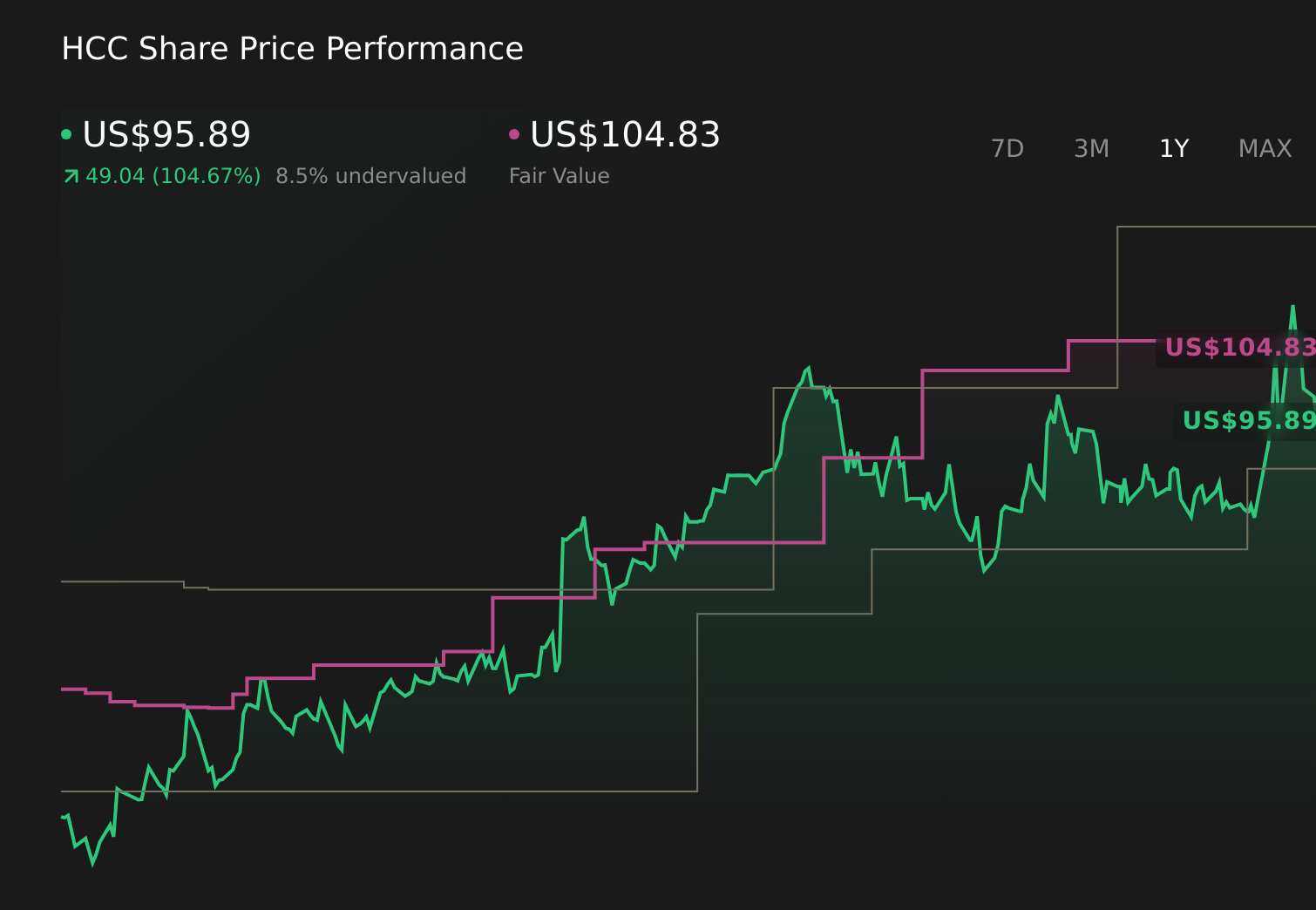

- Recently, Warrior Met Coal was flagged as trading well above one intrinsic value estimate while insiders sold about US$2.2 million of stock over three months without any offsetting insider purchases.

- This tension between strong recent financial results and rising institutional ownership on one hand, and valuation plus insider selling concerns on the other, raises fresh questions about how investors assess the company’s risk‑reward profile today.

- We’ll now examine how insider selling amid perceived overvaluation could reshape Warrior Met Coal’s investment narrative and risk‑reward trade‑offs.

AI is about to change healthcare. These 38 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Warrior Met Coal Investment Narrative Recap

To own Warrior Met Coal today, you need to believe that strong recent earnings and the Blue Creek ramp-up can offset cyclical steel and coal price pressures. The latest news of the stock trading well above one intrinsic value estimate and US$2.2 million of insider selling does not directly alter Blue Creek’s near term execution, but it does sharpen near term focus on valuation risk as the key counterweight to the growth story.

The reaffirmed 2026 production and sales guidance after Q1 2026, targeting 12.0 to 13.0 million short tons of production and 12.5 to 13.5 million short tons of sales, is especially relevant here. It underpins the volume growth thesis that many institutions appear to be backing, even as some valuation models flag potential downside and insiders reduce exposure at recent prices.

Yet, against this strong operational backdrop, investors should still be watching the risk that sustained met coal price weakness and growing dependence on Asian demand could...

Warrior Met Coal's narrative projects $2.5 billion revenue and $543.8 million earnings by 2029.

Uncover how Warrior Met Coal's forecasts yield a $104.83 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts look at the same insider selling and perceived overvaluation and still build in earnings of about US$267 million by 2029, which is far below the more optimistic views, so if you own or are considering Warrior Met Coal it is worth seeing how different investors weigh that kind of slower growth path against the Blue Creek opportunity and possible revisions to expectations after this latest news.

Explore 4 other fair value estimates on Warrior Met Coal - why the stock might be worth as much as 89% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Warrior Met Coal research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Warrior Met Coal research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Warrior Met Coal's overall financial health at a glance.

Contemplating Other Strategies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.