Waste Management (WM) Could Be 7% Undervalued Following Its July 28 Earnings Buildup

Waste Management, Inc. WM | 0.00 |

Waste Management (WM) drew attention after its stock closed at $236.71, a 1.45% gain that came on a day when major indices were weaker, ahead of the company’s July 28 earnings report.

For context, Waste Management’s recent 1.45% one day share price gain and 7.87% 30 day share price return sit within a broader pattern where year to date share price return is 8.38% and 5 year total shareholder return is 78.21%. This suggests solid long term participation in the stock’s story even as attention tightens around the upcoming earnings release.

If this earnings buildup has you thinking more broadly about opportunities in essential infrastructure, it could be a good time to scan power and grid related plays using our 34 power grid technology and infrastructure stocks.

The recent jump in Waste Management stock puts the focus squarely on what is already priced in versus what might still be up for grabs. How much upside are you really paying for at today’s valuation?

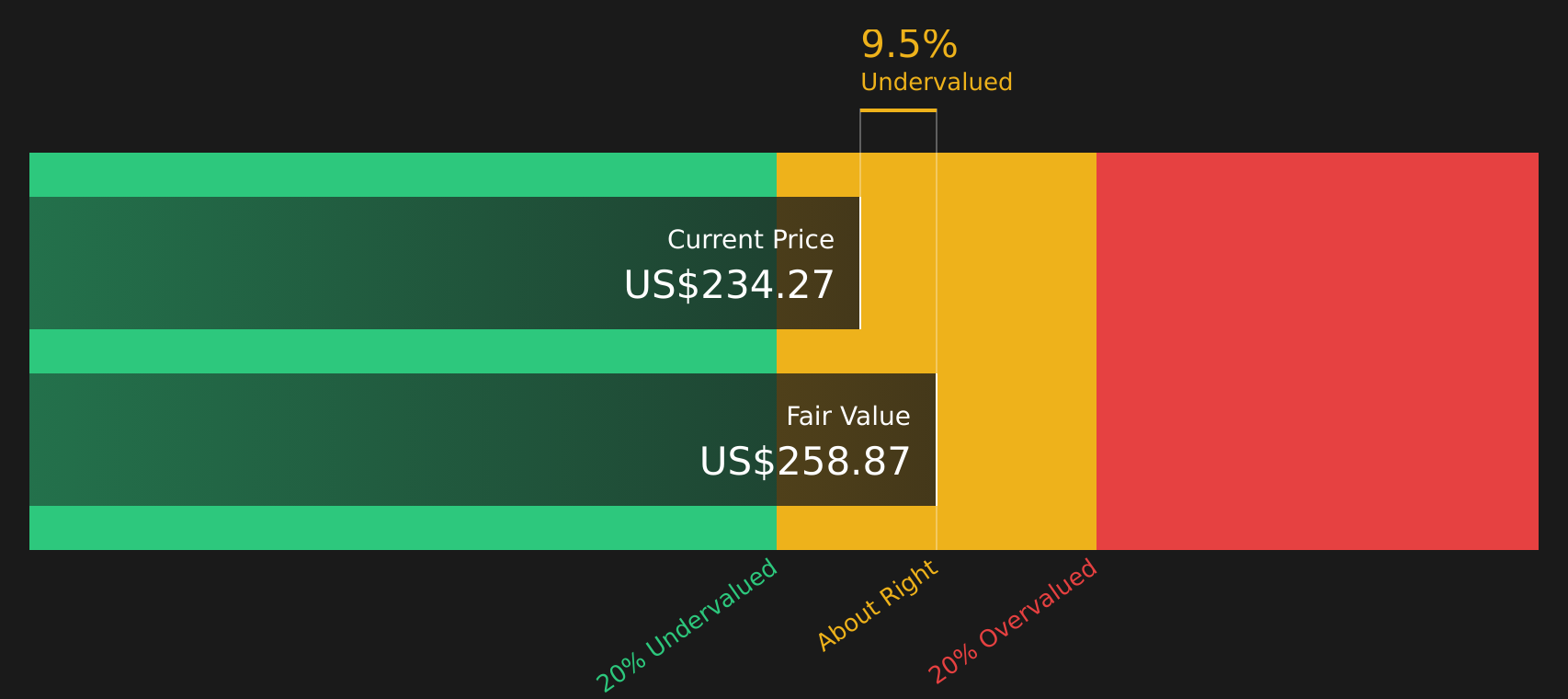

Most Popular Narrative: 6.5% Undervalued

At a last close of $236.71 versus a narrative fair value of $253.12, Waste Management is framed as modestly undervalued using a 7.25% discount rate.

The company's strategic investments in sustainability, particularly in the areas of recycling and renewable energy, are showing strong, high-return growth, which could drive future revenue increases. The integration and optimization of WM Healthcare Solutions are on track to deliver significant synergies, anticipated to reach $250 million annually by 2027, positively impacting earnings.

Here is the core of the Waste Management story. A bigger revenue base. Fatter margins. A future profit profile that assumes meaningful compounding without stretching into fantasy.

Result: Fair Value of $253.12 (UNDERVALUED)

However, that story for Waste Management can be knocked off course if higher leverage from deals like Stericycle integration bites, or if regulatory shifts hit recycling and renewable energy economics.

Another View on Waste Management’s Valuation

The SWS DCF model sees Waste Management at $236.71 trading below an estimated future cash flow value of $258.55, which is framed as 8.4% undervalued. That sits alongside a current P/E of 34x versus a fair ratio of 26.3x, raising a simple question: which signal do you trust more?

Next Steps

Mixed signals on Waste Management's valuation and outlook so far, right, so move quickly to test the data yourself and weigh the 4 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Waste Management?

If you like the story around Waste Management but do not want to rely on a single stock, use the Simply Wall Street Screener to broaden your watchlist intelligently.

- Target potential long term compounders by zeroing in on quality companies trading below their estimated worth through the 46 high quality undervalued stocks.

- Build a steadier income stream by focusing on companies with higher yields and resilient payouts using the 8 dividend fortresses.

- Prioritise resilience by concentrating on companies with stronger finances and cleaner balance sheets through the solid balance sheet and fundamentals stocks screener (47 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.