Waste Management (WM) In Focus On Russell Index Adds As Valuation Debate Builds

Waste Management, Inc. WM | 0.00 |

Index additions and earnings expectations put Waste Management in focus

Waste Management (WM) has been added to several Russell value indices, drawing fresh attention from institutional investors as the company heads into its second quarter earnings report later this month.

Waste Management’s share price has held relatively firm around $228.98, with a 7 day share price return of 2.51% and a year to date share price return of 4.84%, while the 5 year total shareholder return of 73.01% points to a solid longer term record. However, the 90 day share price return has slipped 1.86% as investors weigh its new Russell value index inclusions and the upcoming earnings report.

If this focus on index additions and steady compounding appeals to you, it could be a good moment to broaden your search using the 20 top founder-led companies

Bulls point to Waste Management’s index additions, consistent revenue and profit growth, and an implied upside to analyst targets. Bears, however, question how much is already in the price, raising the question of what the valuation actually suggests.

Most Popular Narrative: 9.5% Undervalued

Waste Management’s most followed valuation narrative puts fair value at $253.12 per share, compared with the last close of $228.98. This frames the current debate around whether investors are fully pricing in its growth and capital allocation plans.

The company's strategic investments in sustainability, particularly in the areas of recycling and renewable energy, are showing strong, high-return growth, which could drive future revenue increases. The adoption of automation and technology, such as automated recycling facilities, is leading to improved EBITDA margins, which might provide stronger future earnings.

Want to see what kind of revenue runway and margin profile needs to line up for that fair value? The narrative leans on steady top line expansion, thicker profitability, and a premium earnings multiple that has to hold up over time. Curious which assumptions really move the valuation and which barely matter? The full breakdown joins those pieces together so you can judge how comfortable you are with the path implied.

The current narrative relies on a discount rate of 7.25%, steady mid single digit revenue growth and slightly higher profit margins, combined with an earnings multiple that sits above the broader Commercial Services sector. All of that is being weighed against the existing $25.4b revenue base, $2.8b of net income and the company’s ongoing capital returns through dividends and buybacks. For investors following Waste Management closely, the key question is whether those inputs feel conservative, aggressive, or about right given the company’s scale and balance sheet.

Result: Fair Value of $253.12 (UNDERVALUED)

However, that story can quickly change if economic pressure on industrial customers bites harder or if issues related to the Stericycle integration keep leverage elevated and squeeze Waste Management’s flexibility.

Another view on Waste Management’s valuation

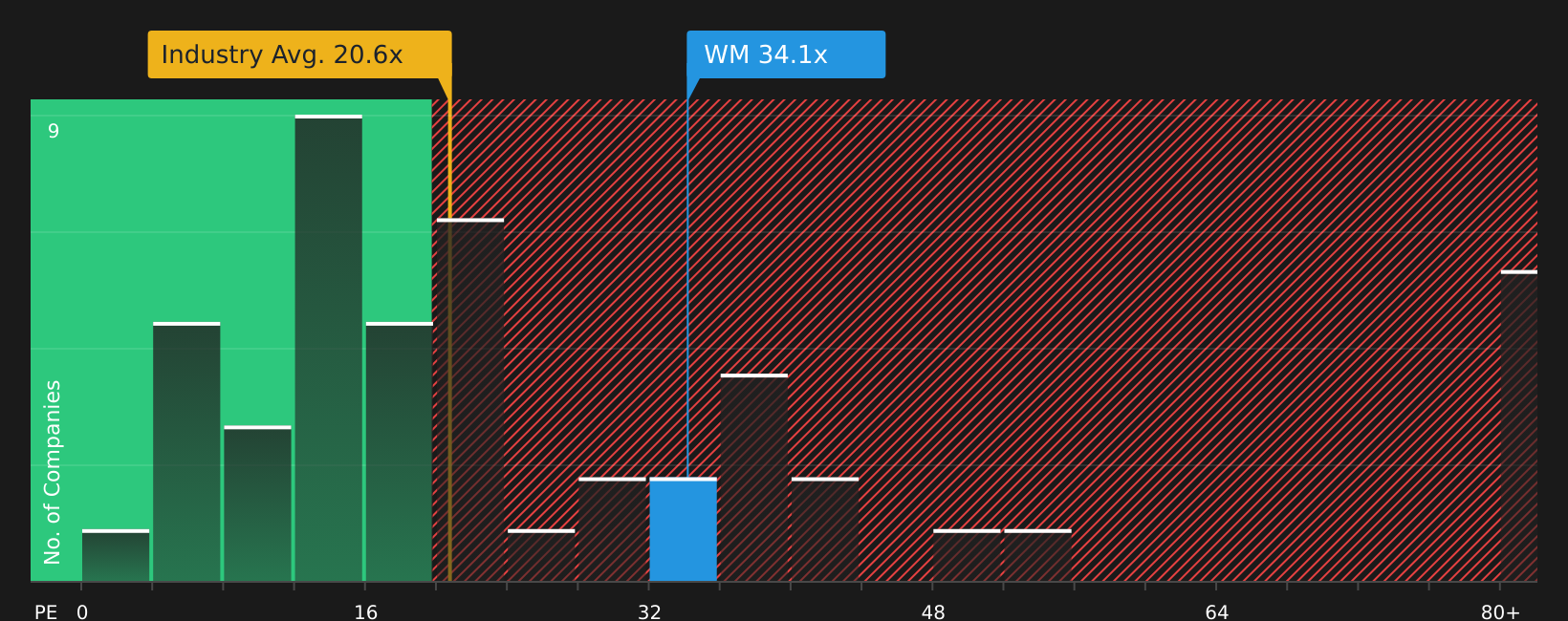

While the narrative and fair value estimate of $253.12 per share lean on discounted future cash flows, the current P/E of 32.9x tells a tougher story. It sits above the estimated fair ratio of 26.4x and well above the US Commercial Services average of 20.8x, which can leave less room for error if sentiment turns.

For investors weighing these signals side by side, the key consideration is whether Waste Management’s quality and cash generation justify paying so far above both the fair ratio and the wider industry, or whether expectations have simply been set too high at today’s price.

Next Steps

With mixed signals around valuation and sentiment on Waste Management, it makes sense to move quickly and test the story against the underlying data yourself. To weigh both the optimism and the concerns side by side, start by reviewing the 4 key rewards and 1 important warning sign.

Looking for more ideas beyond Waste Management?

If the Waste Management story has sharpened your thinking, do not stop here. Broaden your opportunity set now with a few focused stock idea screens.

- Target potential value opportunities by checking companies highlighted in the 41 high quality undervalued stocks that combine quality fundamentals with pricing that may be worth a closer look.

- Strengthen your income stream by reviewing stocks in the 8 dividend fortresses that pair higher yields with an emphasis on stability.

- Prioritize resilience by examining companies in the 74 resilient stocks with low risk scores that score well on financial strength and lower risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.