Waste Management (WM) Valuation Check After Earnings Beat Rekindles Investor Interest

Waste Management, Inc. WM | 0.00 |

Waste Management (WM) is back in focus after reporting quarterly revenue and adjusted EPS that topped analyst expectations, with investors watching how this renewed interest lines up with the company’s upcoming William Blair conference appearance.

The share price has started to stabilize, with a 1-day share price return of 2.86% and a 7-day share price return of 1.12%. It remains down 11.41% over 90 days and the 1-year total shareholder return is down 7.36%. However, the 5-year total shareholder return of 68.15% highlights how longer term holders have experienced a very different journey.

If recent earnings have you reassessing your watchlist, it could be a good moment to widen the search and scan 20 top founder-led companies

With shares still below recent highs yet trading after an earnings beat and renewed analyst interest, is Waste Management quietly offering value, or is the current price already factoring in most of the company’s future growth potential?

Most Popular Narrative: 13.9% Undervalued

At the latest close, Waste Management shares at $218.00 sit below a narrative fair value estimate of $253.12, which frames the current debate around upside potential.

The company's strategic investments in sustainability, particularly in the areas of recycling and renewable energy, are showing strong, high-return growth, which could drive future revenue increases. The integration and optimization of WM Healthcare Solutions are on track to deliver significant synergies, anticipated to reach $250 million annually by 2027, positively impacting earnings.

Want to see what sits behind that valuation gap? The narrative leans on steady top line expansion, rising margins, and a richer earnings multiple that needs careful unpacking.

Result: Fair Value of $253.12 (UNDERVALUED)

However, that potential upside sits alongside real pressure points, including revenue volatility from business exits and higher leverage following the Stericycle acquisition, which could limit flexibility.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another Angle on Valuation

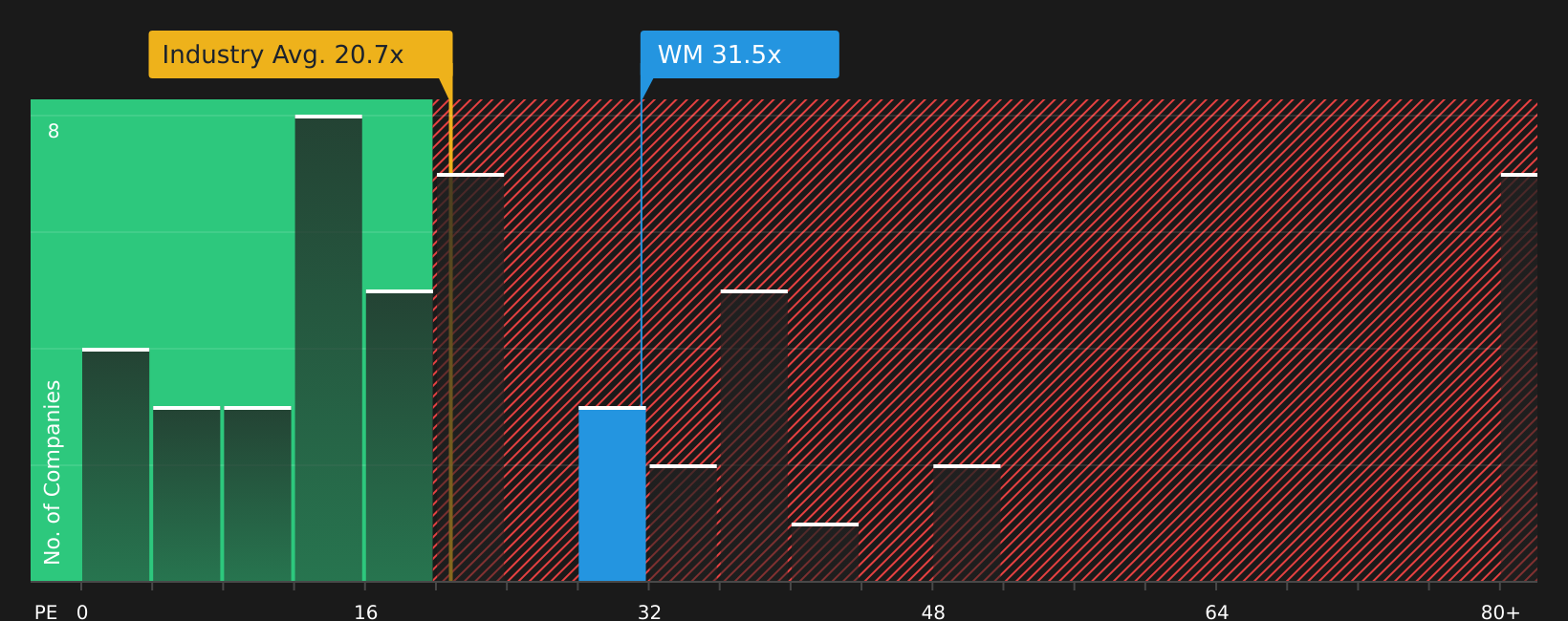

The community narrative points to a fair value of $253.12 and labels Waste Management as undervalued. However, the current P/E of 31.3x sits above both the US Commercial Services industry at 21.7x and a fair ratio of 25.7x. This raises the question of how much margin of safety is really there.

Next Steps

With mixed signals on value, risk and reward, now is the time to look through the numbers yourself and decide where you stand. Start with the 4 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Waste Management is on your radar, do not stop there; cast a wider net with focused stock lists that can surface opportunities you might otherwise miss.

- Target strong income potential by reviewing companies in the 10 dividend fortresses and see which payouts catch your attention.

- Prioritise balance sheet strength by scanning the solid balance sheet and fundamentals stocks screener (47 results) so you can focus on businesses with financial resilience.

- Hunt for lesser known opportunities using the screener containing 22 high quality undiscovered gems and spot ideas before they become crowded trades.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.