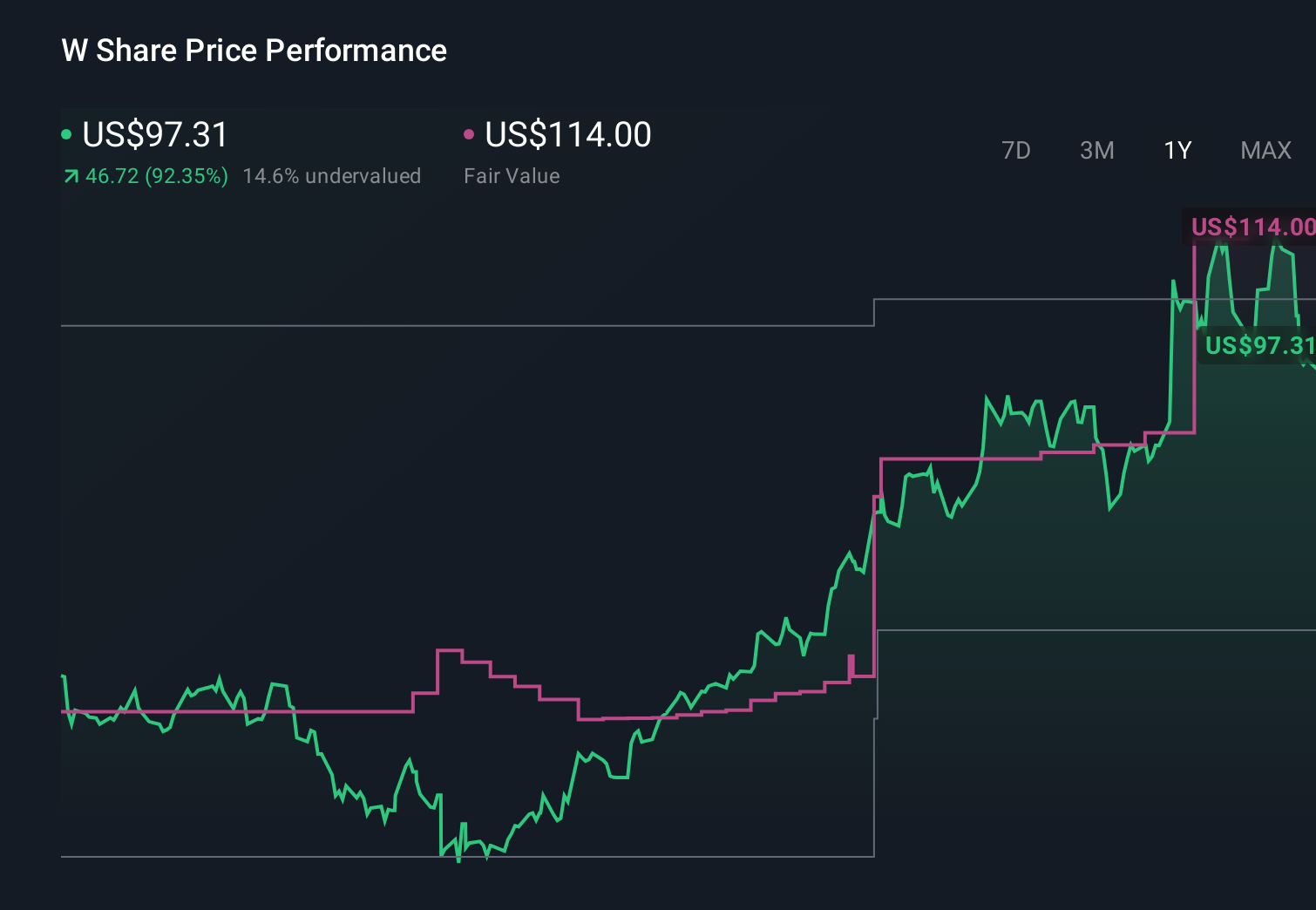

Wayfair (W) Is Down 5.4% After Insider Selling And Macro Jitters Challenge Its Upgrade Story

Wayfair W | 0.00 |

- In recent days, Wayfair faced renewed scrutiny as investors weighed rising interest rates, insider share sales worth US$37.5 million over three months, and concerns about profitability and valuation against ongoing operational upgrades and promotional efforts such as its post-holiday Warehouse Sale.

- At the same time, Wayfair has been rolling out logistics and delivery enhancements, including automation and more precise delivery options, which aim to improve customer experience and reduce last‑mile costs even as macroeconomic and advertising headwinds intensify.

- We’ll now examine how insider selling alongside macro pressure on growth valuations may alter Wayfair’s previously outlined investment narrative.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

Wayfair Investment Narrative Recap

To own Wayfair today, you have to believe its logistics, merchandising, and omnichannel investments can eventually turn a currently unprofitable, promotion-heavy model into something more durable. In the near term, the key catalyst is evidence of sustained margin progress, while the biggest risk is that higher rates and soft housing demand keep pressuring big-ticket purchases. The latest pullback on valuation worries and insider selling highlights those concerns but does not fundamentally change that core debate.

Among recent announcements, the logistics upgrades showcased at Home Delivery World 2026 look most relevant. More accurate product dimensions, consolidated delivery options, and automated pre delivery communication all tie directly into the CastleGate thesis that better fulfillment can lower last mile costs and support healthier margins. If these initiatives scale effectively, they could matter more for the story than short term promotional events like the Warehouse Sale.

But while these logistics gains are encouraging, investors should also be aware that...

Wayfair's narrative projects $14.9 billion revenue and $378.0 million earnings by 2029. This requires 5.7% yearly revenue growth and a $683.0 million earnings increase from -$305.0 million today.

Uncover how Wayfair's forecasts yield a $93.43 fair value, a 37% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting revenues near US$15.9 billion and earnings above US$600 million by 2029, yet the recent rate driven pullback shows how quickly views on risks like structurally thin margins and interest rate sensitivity can shift, so it is worth weighing these bullish assumptions against more cautious scenarios.

Explore 4 other fair value estimates on Wayfair - why the stock might be worth 35% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Wayfair research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Wayfair research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Wayfair's overall financial health at a glance.

Searching For A Fresh Perspective?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.