Wayfair (W): Valuation in Focus After Q3 Beat, Board Addition, and Retail Expansion Push

Wayfair, Inc. Class A W | 75.25 75.25 | +0.05% 0.00% Post |

Wayfair (W) delivered upbeat third-quarter results, highlighting momentum in sales growth and profitability. Investor confidence received another lift as the company welcomed Hal Lawton, CEO of Tractor Supply, to its board of directors.

Wayfair’s share price has skyrocketed 132% year-to-date, with momentum accelerating. For example, November saw an 8% jump after robust Q3 results, expansion plans, and a seasoned retail executive joining the board. Despite a challenging long-term stretch, the last twelve months brought a total shareholder return of 175% as investors reward the company's strategic shifts and growth signals.

If you’re curious what other fast-growing businesses with notable insider skin in the game look like, consider broadening your search and discover fast growing stocks with high insider ownership

With shares soaring and new initiatives underway, the key question is whether Wayfair’s impressive turnaround leaves room for further upside or if the current stock price fully reflects these positive shifts and future growth potential.

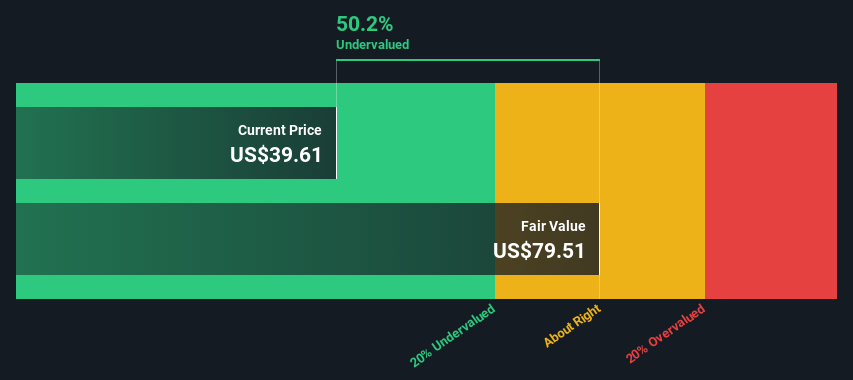

Most Popular Narrative: 4.8% Undervalued

Wayfair's most closely tracked narrative points to a fair value of $112.31, just above the recent closing price of $106.88. The minimal gap highlights a debate on whether current optimism is fully priced in or still has more room to run. Let’s look at the thinking driving this estimate.

Wayfair's proprietary logistics network, CastleGate, is expected to provide a meaningful growth unlock by improving efficiency and customer experience, which can positively impact revenue growth through higher conversion rates and potentially improved net margins.

What is fueling this calculated optimism? The narrative leans heavily on shifting profit margins and revenue gains that hinge on operational and customer experience breakthroughs. Curious about the concrete assumptions and where the bulls and bears clash? Only the full narrative reveals the key projections and hidden fault lines.

Result: Fair Value of $112.31 (UNDERVALUED)

However, persistent challenges in the housing market or weaker than expected returns from new initiatives could quickly cool investor optimism around Wayfair’s turnaround story.

Another View: The DCF Deep Dive

While the price-to-sales ratio suggests that Wayfair shares may be trading at a premium compared to industry and fair ratio benchmarks, our SWS DCF model tells a different story entirely. According to this discounted cash flow approach, Wayfair looks significantly undervalued based on projected future cash flows. Could the market be overlooking long-term value, or is the DCF painting too rosy a picture?

Build Your Own Wayfair Narrative

If you think there’s another angle to consider or want to dig into the numbers on your own, you can easily build your own perspective in just a few minutes, your way. Do it your way.

A great starting point for your Wayfair research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Angles?

Unlock even more potential opportunities faster. The right stock could change your outlook, so do not let these standout picks slip past your radar. Check them out now.

- Uncover higher passive income streams when you scan these 16 dividend stocks with yields > 3% with yields topping 3% and a history of rewarding shareholders.

- Jump into the AI trend and back up-and-coming businesses making headlines among these 25 AI penny stocks, before the rest of the market catches on.

- Spot undervalued gems hiding in plain sight through these 875 undervalued stocks based on cash flows, where strong cash flows and low prices meet genuine opportunity.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.