Wayfair (W) Valuation in Focus Following Analyst Upgrades, New Board Appointment, and Q3 Earnings Beat

Wayfair, Inc. Class A W | 75.25 75.25 | +0.05% 0.00% Post |

Wayfair (W) is catching attention after a series of analyst rating upgrades and board changes, following third-quarter results that outperformed expectations. Renewed investor confidence is being shaped by a mix of strategic moves and management shifts.

Wayfair’s momentum has picked up following a flurry of board changes, debt management moves, and new retail store strategies. This has sent its share price to $101.94 and resulted in a 121% year-to-date price return. While the stock slid 4.3% in the latest session during a tech selloff, its one-year total shareholder return of 153% and a three-year return over 200% indicate a strong recovery phase, especially as institutional investors reposition and management undertakes significant strategic initiatives.

If this dramatic rebound has you rethinking what’s possible in today’s market, now’s a great time to explore fast growing stocks with high insider ownership.

With shares rallying and analyst price targets on the rise, the big question is whether Wayfair’s rapid rebound signals an undervalued opportunity for investors or if the market has already priced in future growth.

Most Popular Narrative: 9.2% Undervalued

Wayfair’s most widely tracked narrative suggests a fair value of $112.31, almost $10 above its last closing price of $101.94. This points to further upside potential if the narrative projections materialize. The narrative sets expectations for meaningful improvement in financial performance and valuation compared to the current market.

"Wayfair's proprietary logistics network, CastleGate, is expected to provide a meaningful growth unlock by improving efficiency and customer experience. This can positively impact revenue growth through higher conversion rates and potentially improved net margins. The launch of Wayfair Verified and new merchandising initiatives like personalized promotions are aimed at enhancing customer trust and user experience, potentially driving higher sales and revenue per unit through increased customer engagement and conversion rates."

Curious what’s behind this bullish valuation? The narrative includes a bold set of forward-looking earnings assumptions, margin expansion, and revenue growth rates built into the core outlook. Want to see how these ambitious forecasts turn into today’s price estimate? The numbers might surprise you.

Result: Fair Value of $112.31 (UNDERVALUED)

However, persistent weakness in the housing market or delayed returns on heavy tech and logistics investments could challenge these optimistic projections.

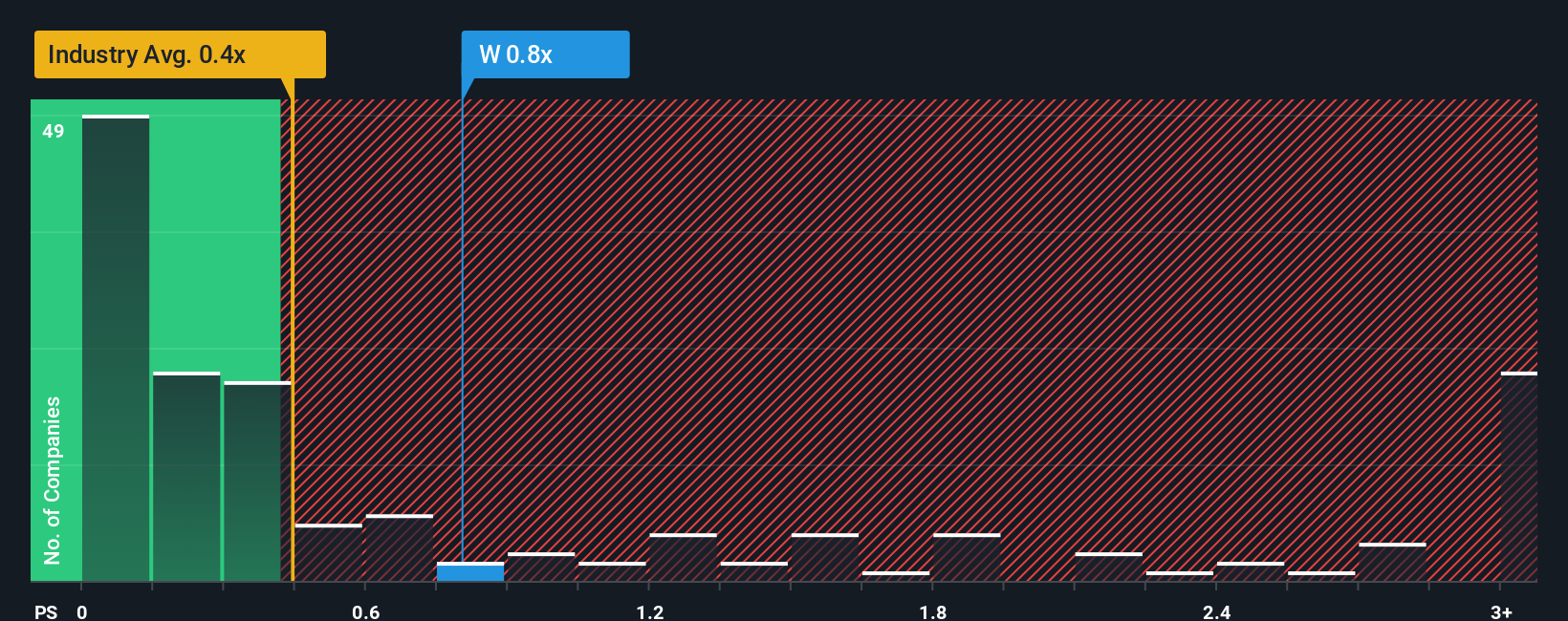

Another View: Multiples-Based Valuation Challenges the Narrative

While some forecasts paint Wayfair as undervalued, a quick look at its price-to-sales ratio tells another story. Wayfair trades at 1.1x sales, which is much higher than the US Specialty Retail industry average of 0.4x and above its fair ratio of 0.7x. This raises questions about whether the rebound is fully justified, especially if the market eventually demands alignment with broader industry norms.

Build Your Own Wayfair Narrative

If you see things differently or want to dive into the numbers yourself, you can put together your own narrative. It only takes a few minutes. Do it your way

A great starting point for your Wayfair research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t limit your portfolio’s potential. Act now to identify hidden gems and seize new opportunities with these proven strategies tailored for different investor goals.

- Cash in on tomorrow’s trends by targeting these 26 AI penny stocks that are capitalizing on breakthroughs in artificial intelligence and automation.

- Start building passive income by tapping into these 16 dividend stocks with yields > 3% that deliver yields greater than 3% from reliable businesses.

- Position yourself early in a transformational sector by targeting these 26 quantum computing stocks at the forefront of computing innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.