Weaker Earnings And Oil‑to‑Gas Shift Might Change The Case For Investing In Devon Energy (DVN)

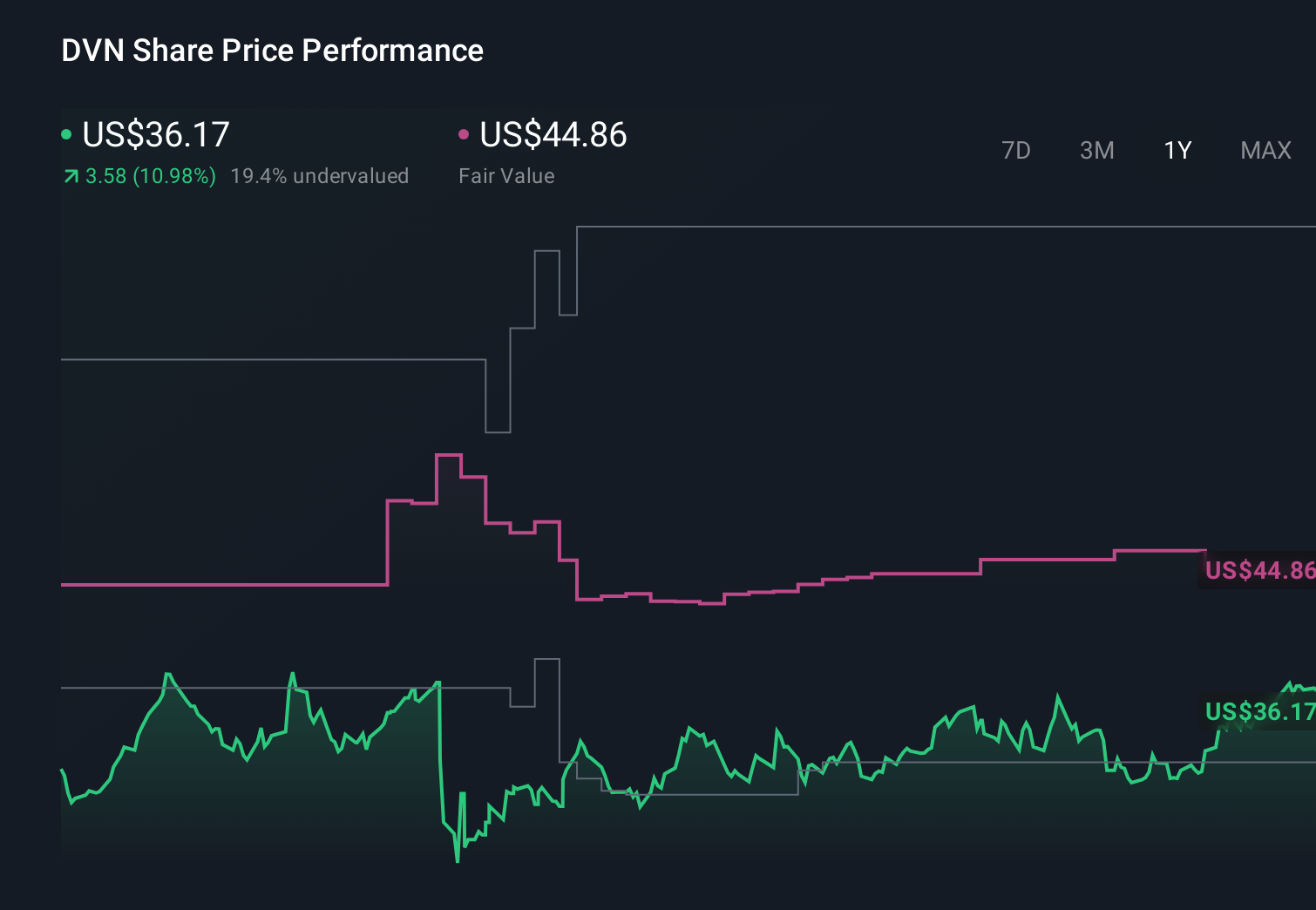

Devon Energy Corporation DVN | 0.00 |

- Devon Energy recently reported that its February 17, 2026 earnings release showed earnings per share down more than 30% year over year, alongside an 8.52% revenue decline and a shift toward higher gas revenues but lower oil revenues.

- This combination of weaker earnings and a changing oil-gas revenue mix has prompted analysts to reassess their expectations and trim earnings forecasts.

- Next, we’ll consider how these weaker near-term earnings expectations and downward estimate revisions affect Devon Energy’s broader investment narrative.

Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

Devon Energy Investment Narrative Recap

To own Devon Energy, you need to believe in the resilience of its U.S. shale portfolio and its ability to convert volatile commodity-linked cash flows into shareholder returns through cycles. The expected 30 percent-plus EPS decline and 8.52 percent revenue drop, alongside a heavier tilt toward gas, sharpen the near term focus on earnings sensitivity to prices, but do not yet clearly alter the key near term catalyst of potential portfolio moves or the biggest risk around sustained margin pressure.

The most relevant recent development here is the round of analyst estimate cuts heading into the 17 February 2026 earnings release, with consensus EPS for the quarter reduced by 11.6 percent in just 30 days. That reassessment sits uncomfortably beside ongoing discussions about Devon’s future scale and mix, including rumored merger talks, because weaker expected earnings can influence how investors view any deal’s risks, potential synergies, and the company’s capacity to keep funding buybacks and dividends.

Yet behind the appeal of Devon’s assets and capital returns, there is a growing concern investors should be aware of around how quickly core shale wells decline and whether...

Devon Energy's narrative projects $19.3 billion revenue and $3.0 billion earnings by 2028.

Uncover how Devon Energy's forecasts yield a $44.34 fair value, in line with its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already assuming revenue of about US$17.4 billion and earnings near US$2.0 billion by 2028, so if you worry about prolonged margin compression and more volatile gas weighted cash flows, their more cautious view may feel closer to home, especially now that the latest earnings expectations are being reset and both the consensus and the pessimists might need to revisit their numbers.

Explore 9 other fair value estimates on Devon Energy - why the stock might be worth 31% less than the current price!

Build Your Own Devon Energy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Devon Energy research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Devon Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Devon Energy's overall financial health at a glance.

Looking For Alternative Opportunities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Find 54 companies with promising cash flow potential yet trading below their fair value.

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.