Webull (BULL) Premium Push Keeps Fair Value Debate Alive

Bull Run Corp BULL | 0.00 |

Webull (BULL) has caught investor attention after recent trading, with the stock closing at $6.75 and short term returns mixed, up about 5% over the past month but down year to date.

While Webull’s share price return over the past 90 days is up 40.62%, the year to date share price return is down 17.58% and the 1 year total shareholder return is down 43.56%. This suggests that recent momentum contrasts with weaker longer term performance.

If you are weighing Webull against other ideas in the current market, this could be a good moment to scan for 20 top founder-led companies

With Webull trading at $6.75 and screens flagging a large gap to some estimated value metrics, the core question is simple: is the stock still undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 43.8% Undervalued

At a last close of $6.75 against a narrative fair value of $12.00, Webull is framed as materially undervalued, with that gap resting on ambitious long term assumptions.

The successful launch and acceleration of subscription-based offerings such as Webull Premium and paid analytics products are already exceeding targets, combining higher daily trading activity and increased average revenue per user (ARPU) to boost net margins and recurring revenue stability.

Want to see what turns this story into a $12.00 fair value? The narrative leans on steep revenue expansion, margin rebuilding, and a richer earnings multiple. Curious which projections really move the needle?

Result: Fair Value of $12.00 (UNDERVALUED)

However, this Webull narrative still leans on continued retail trading activity and supportive regulations, either of which could shift and challenge those fair value assumptions.

Another View: Webull Looks Expensive On Sales

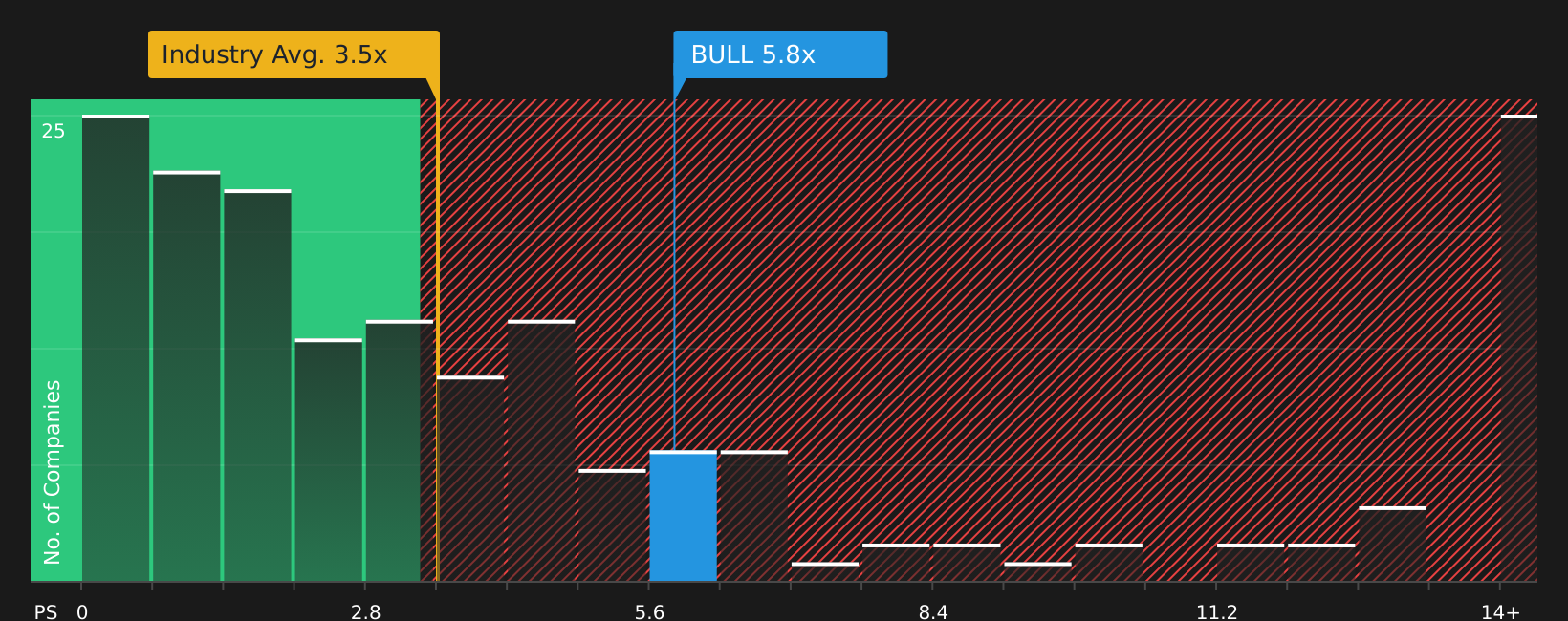

While the narrative fair value suggests Webull is undervalued, the picture changes when you look at its P/S ratio. At around 6x sales, the stock trades well above the estimated fair ratio of 3x, the US Capital Markets industry average of 3.4x, and the peer average of 1.4x.

In practical terms, you are paying a higher price for each dollar of Webull revenue than both the wider industry and closer peers. This raises the bar for how well future growth would need to develop to justify today’s valuation. Is that premium something you are comfortable underwriting?

Next Steps

With sentiment on Webull clearly split between risks and rewards, this is a moment to move quickly and weigh the 3 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Webull?

If Webull has you thinking more broadly about your portfolio, this can be a useful time to scan other opportunities that might better match your risk and return goals.

- Target steadier compounding by reviewing companies with 72 resilient stocks with low risk scores that aim to limit drawdowns while still offering room for growth.

- Hunt for mispriced quality by scanning screener containing 19 high quality undiscovered gems that may not be widely followed but still show strong fundamentals.

- Strengthen your defensive core by filtering for companies in the solid balance sheet and fundamentals stocks screener (48 results) that prioritize resilient finances and financial discipline.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.