Webull (BULL) Stock Could Be 42.8% Undervalued as Crypto Growth Narrative Builds

Bull Run Corp BULL | 0.00 |

Webull (BULL) is drawing attention after recent trading data highlighted its mixed return profile, with the stock down about 34% over the past year and up roughly 34% in the past 3 months.

For Webull, the 30 day share price return of 11% and 90 day share price return of 33.7% contrast with a 1 year total shareholder return that is down 34.2%. This points to improving short term momentum from a weaker longer term base.

If you are rethinking your watchlist after Webull's recent moves, it could be a good moment to broaden your search with the 20 top founder-led companies

With Webull trading at a steep discount to its analyst price target and screens suggesting an intrinsic discount as well, the key question is whether the stock is genuinely undervalued or whether the market is already pricing in future growth.

Most Popular Narrative: 42.8% Undervalued

With Webull shares last closing at $6.86 against a narrative fair value of $12.00, the current setup centers on whether earnings and user growth can eventually support that gap.

Rapid adoption and reintroduction of crypto trading, alongside the platform's ability to quickly add new digital asset classes and prediction markets, positions Webull to capture growing demand for broad, mobile-accessible investment options, fueling revenue growth and market share.

Want to see what is driving that valuation gap for Webull? The core of this narrative leans on faster revenue growth, sharply higher margins, and a richer earnings multiple. Curious how those moving parts fit together into a $12 fair value, and what assumptions sit under each of them?

Result: Fair Value of $12 (UNDERVALUED)

However, Webull’s reliance on retail trading activity and exposure to shifting regulations, particularly around crypto and international expansion, could quickly challenge this upside narrative.

Another View: What Webull’s Valuation Ratios Are Saying

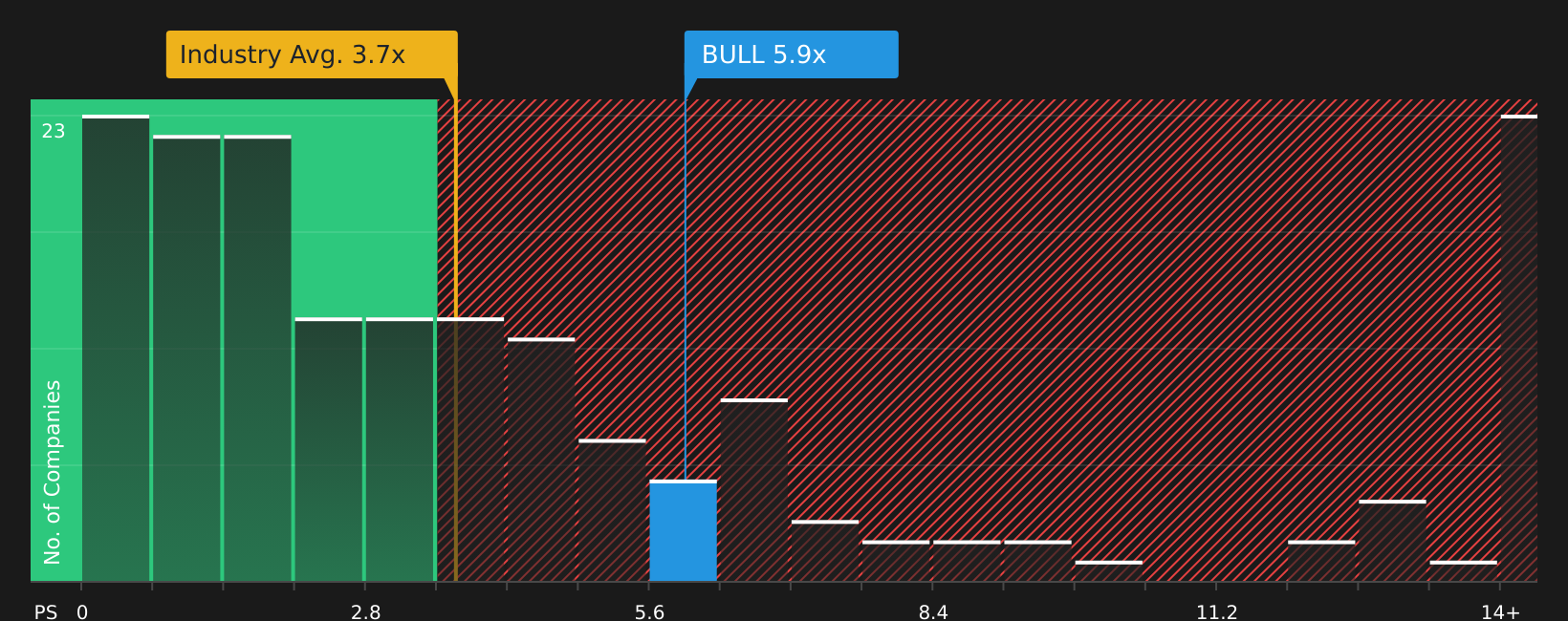

While the SWS DCF model points to Webull as undervalued based on future cash flows, the current P/S ratio of 6.1x looks expensive versus the US Capital Markets industry at 3.7x and an estimated fair ratio of 3.1x. Is the market overpaying for growth, or underestimating long term cash generation?

For a closer look at how this gap between market pricing and the fair ratio could matter for your risk and return expectations, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With both upbeat and cautious signals around Webull in play, this is the moment to review the details yourself and form a clear stance using the 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond Webull?

If you are serious about building a stronger portfolio, now is the time to widen your search with other high quality ideas before the crowd catches on.

- Target reliable income streams by hunting for companies with robust payouts and staying power using the 7 dividend fortresses.

- Spot potential mispricings ahead of the market by scanning companies that score well on quality yet trade at attractive valuations via the 44 high quality undervalued stocks.

- Focus on resilience by reviewing companies that pair durable fundamentals with lower risk profiles inside the 66 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.