Weighing The Split Valuation Signals For Wells Fargo (WFC) After Its Recent Share Gains

Wells Fargo & Company WFC | 80.29 80.30 | -1.73% +0.01% Pre |

Context for Wells Fargo Stock Right Now

Without a single headline catalyst today, Wells Fargo (WFC) still gives investors plenty to work with, from its recent share performance to its current earnings profile and valuation signals.

At a share price of US$88.70, Wells Fargo’s recent gains, including a 4.77% 90 day share price return, sit alongside a much stronger picture over time. The 1 year total shareholder return is 16.94% and the 5 year total shareholder return is 175.64%, which hints at sentiment that has shifted meaningfully over the longer term.

If this has you thinking about where else capital could work hard in financials and beyond, it could be worth scanning 22 top founder-led companies as a way to surface fresh stock ideas.

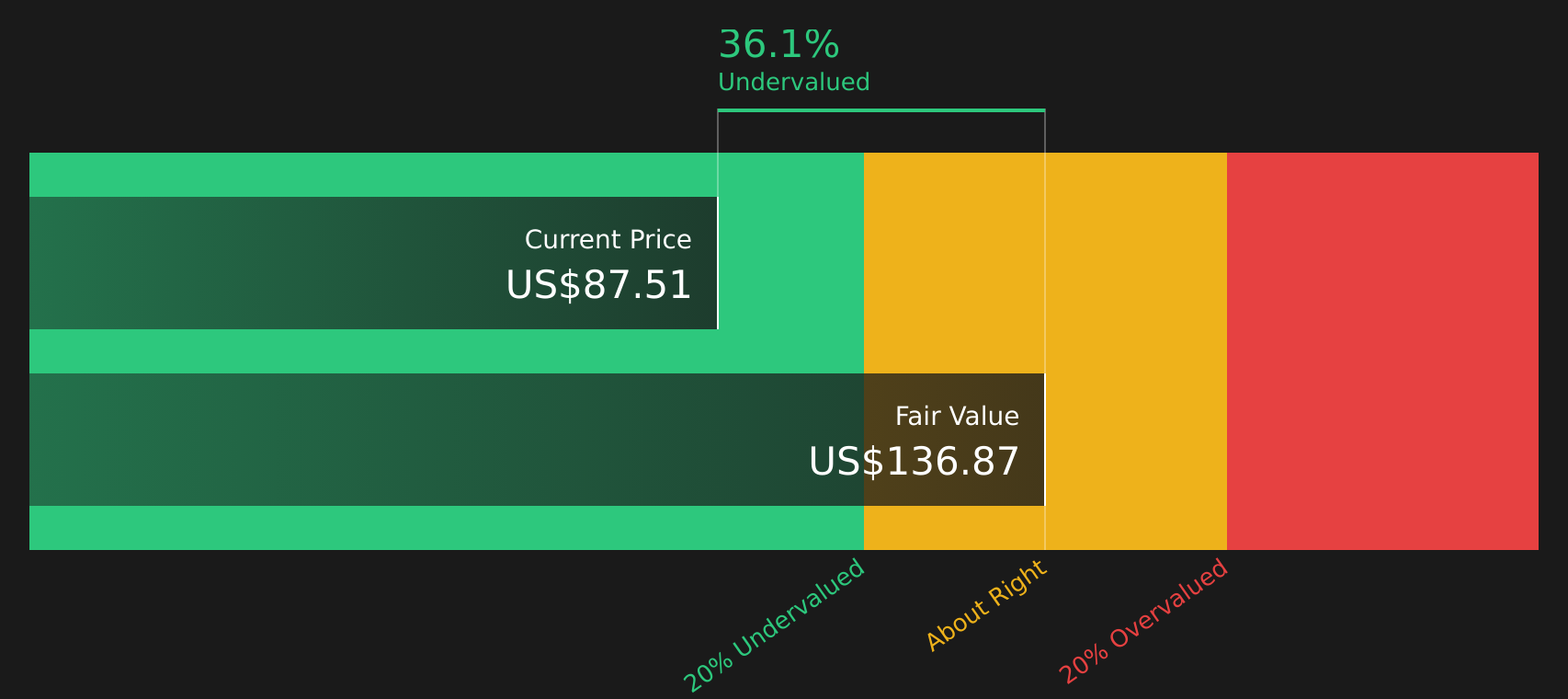

With Wells Fargo trading at US$88.70 alongside a value score of 4 and an indicated intrinsic discount of roughly 31%, the key question is whether this reflects a genuine mispricing or a market that is already factoring in future growth.

Most Popular Narrative: 18.7% Overvalued

Compared to the last close of $88.70, the most followed narrative from mschoen25 points to a fair value of $74.70 built on detailed growth and profitability assumptions.

One of the reasons for its undervaluation is related to the broader economic environment, particularly the sluggishness in the housing and manufacturing sectors. However, Wells Fargo has significant advantages, such as a wide economic moat from its large customer base and low funding costs. Additionally, potential regulatory changes, like the lifting of the asset cap that limits the bank's growth, could drive future profitability. In short, while Wells Fargo is trading below its intrinsic value, its strong fundamentals, expansive customer base, and strategic investments make it a compelling option for investors seeking undervalued opportunities in the banking sector.

Curious how a bank with this kind of moat, margin profile, and future earnings multiple ends up with a lower fair value than today’s price? The full narrative walks through the revenue path, profit assumptions, and valuation anchor that pull the estimate down while still leaning on constructive growth inputs.

Result: Fair Value of $74.70 (OVERVALUED)

However, this narrative could be challenged if housing and manufacturing stay weak for longer than expected, or if regulatory changes, such as the asset cap, shift less favorably.

Another Angle on Value

That community fair value of $74.70 says Wells Fargo looks 18.7% overvalued, but our DCF model comes back with a very different message. On that view, the stock at $88.70 screens as undervalued against an estimated future cash flow value of $127.77. Which story do you think fits better with your risk tolerance?

Next Steps

If the split view on Wells Fargo has you on the fence, this is the moment to look through the numbers yourself and decide where you stand. Then weigh up 3 key rewards and 2 important warning signs to round out your own judgment.

Looking for more investment ideas?

If Wells Fargo has sharpened your thinking, do not stop here. The right next idea could be sitting just one screen away.

- Target resilient income by scanning companies we flag as 15 dividend fortresses that might suit investors who care about cash flow from payouts.

- Hunt for value first and story second with our list of 54 high quality undervalued stocks that filter for quality fundamentals and pricing that may not reflect them.

- Prioritise peace of mind by checking 87 resilient stocks with low risk scores designed to highlight businesses with measured risk profiles and sturdier financial footing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.