Wells Fargo Stock And Other Bank Shares Worth A Closer Look Now

Wells Fargo & Company WFC | 0.00 |

With AI semiconductor stocks under pressure and markets rotating toward steadier areas, many investors are taking a fresh look at value stocks in non tech, defensive sectors. The recent mix of softer jobs data, record highs in the Dow, and firming financials has put more attention on companies with established business models, lower volatility, and grounded valuations. This article introduces three stocks from a Value Stocks screener that appear especially exposed to the latest macro news. It is designed to help you think through where the risks and potential resilience might sit before you decide how they fit, or do not fit, in your own portfolio.

Wells Fargo (WFC)

Overview: Wells Fargo is a large US financial services company that offers everyday banking, lending, mortgage, investment, and wealth management services to consumers, small businesses, corporations, and institutions in the US and internationally.

Operations: Wells Fargo generates most of its revenue from Consumer Banking and Lending at about US$34.5b, followed by Corporate and Investment Banking at about US$19.2b, Wealth and Investment Management at about US$16.8b, and Commercial Banking at about US$11.9b, with all reported revenue of roughly US$81.1b coming from the United States.

Market Cap: US$261.7b

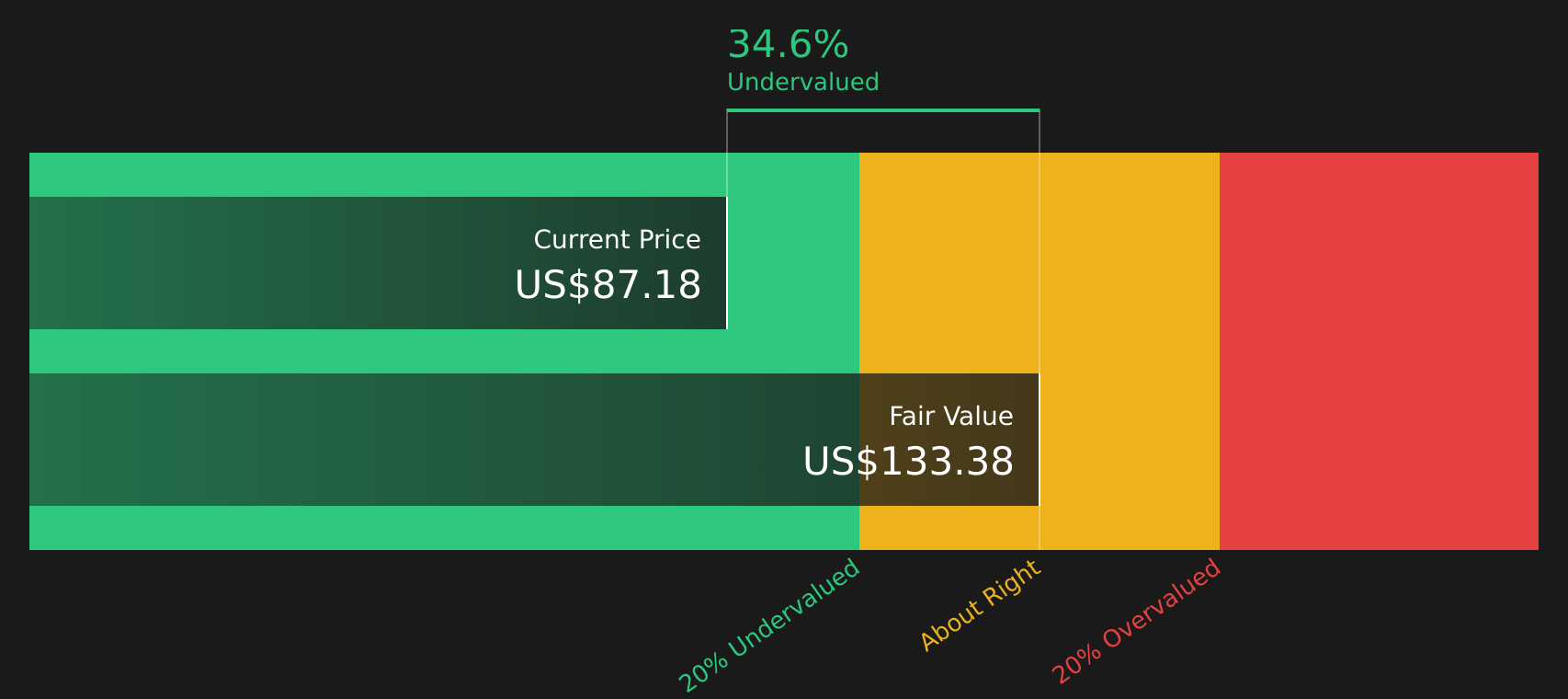

In a market that is rotating toward established financials, Wells Fargo offers large scale US exposure, solid earnings quality, and a valuation that screens as attractive against estimated fair value. It also sits at the center of the post asset cap reopening story. The removal of regulatory limits, recent Fed stress test clearance, and plans to raise dividends and continue buybacks highlight how more of its earnings power can now reach shareholders, even as forecast earnings growth of about 4% to 5% per year remains relatively modest. On the risk side, only moderate return metrics, an uneven dividend history, and governance concerns around high CEO pay and a lack of fresh board appointments mean investors still need to weigh how much trust to place in this turnaround.

Wells Fargo’s asset cap story is reopening and its valuation still screens as appealing, but the real question is how much of that earnings power truly reaches you, and what the 3 key rewards and 1 important warning sign might be hinting at

PNC Financial Services Group (PNC)

Overview: PNC Financial Services Group is a diversified US bank that offers everyday checking and savings accounts, loans, credit cards, and digital banking for consumers and small businesses. It also provides lending, cash management, capital markets, and wealth management services to larger corporations, institutions, and high net worth families.

Operations: PNC generates most of its revenue from Retail Banking including residential mortgage at about US$14.8b and Corporate & Institutional Banking at about US$11.3b. There is a smaller contribution from Asset Management Group at about US$1.8b and a declining Other segment that reduced revenue by about US$4.8b.

Market Cap: US$100.2b

PNC Financial Services Group is positioned as a value oriented bank at a time when some investors are favoring financials over more expensive technology stocks. It has high earnings quality, a 2.69% dividend, and analysts are focused on its capital return and revenue ambitions. The stock appears inexpensive compared with some intrinsic value estimates and peers, while having a conservative risk profile, a long operating history, and tangible developments such as FirstBank integration, expense discipline, and interest rate risk management that relate to current labor market data and sector rotation toward more defensive areas. At the same time, insider selling, modest return on equity, and governance questions around pay and board refresh indicate there may be more factors to evaluate before determining whether this is a long term compounder or a value opportunity that may warrant closer ongoing scrutiny.

PNC’s mix of conservative balance sheet, 2.69% dividend, and a stock that screens as inexpensive hints at a story many investors may be underestimating. The real question is what the 4 key rewards and 1 important warning sign could reveal about how that trade off actually plays out.

U.S. Bancorp (USB)

Overview: U.S. Bancorp is a large U.S. financial services holding company that provides everyday banking, loans, credit cards, payments, wealth management, and trust services to consumers, businesses, institutions, and government clients across the country.

Operations: U.S. Bancorp generates about US$11.9b in revenue from Wealth, Corporate, Commercial and Institutional Banking, US$8.7b from Consumer and Business Banking, US$5.9b from Payment Services, and a smaller contribution from Treasury and Corporate Support, with all reported revenue of roughly US$26.6b coming from the United States.

Market Cap: US$96.2b

U.S. Bancorp is attracting attention as investors rotate out of expensive AI and tech stocks into established financials, because it offers a mix of high quality earnings, a 3.31% dividend, and exposure to payments and capital markets through initiatives like the BTIG acquisition and new Amazon business card partnership. Earnings and revenue are both forecast to grow at high single digit rates, margins are currently reported at 27.9%, and recent stress test results and dividend increases are cited as indicators of a solid capital position. The stock is also described as trading below some intrinsic value estimates and peer P/E multiples. The key tension is significant insider selling and a history of weaker longer term earnings trends, which raises the question of whether the recent momentum and platform upgrades are being fully appreciated by the market or are being priced as temporary.

U.S. Bancorp’s mix of payments exposure, its 3.31% dividend, and high single digit earnings and revenue forecasts suggests the story may be richer than a simple value play. The analyst forecasts for U.S. Bancorp could show whether recent insider selling is hinting at something deeper or masking an underappreciated shift in the business.

The three stocks in this article are just a starting point. The full Value Stocks, Non Tech, Defensive Sectors, screener surfaces 36 more companies with equally compelling narratives through the Value Stocks (Non-Tech, Defensive Sectors) screener. Use Simply Wall St to identify and analyze the specific catalysts, risk profiles, and valuation signals that matter to you so you can focus on the highest conviction ideas in this defensive value theme.

Take Control of Your Investment Journey

If PNC Financial Services Group or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Curious About Seeking Smarter Alternatives?

Fresh ideas move fast. While attention is fixed on today’s headlines, other stocks can be building quiet breakout momentum under the radar for now, so consider acting promptly.

- Spot companies quietly building momentum before the crowd notices by scanning the 18 high quality undiscovered gems curated for resilience and quality while prices still look reasonable.

- Lock onto cash generative businesses with sturdy balance sheets using the curated list of solid balance sheet and fundamentals (47 results) so you are not caught chasing strength after prices start moving.

- Stay informed on developments in precious metals by tracking producers in the 33 elite gold producer stocks while sentiment is still cooling and entry points may be more forgiving.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.