Wells Fargo (WFC) Stock Looks To Trade At A Discount To Fair Value

Wells Fargo & Company WFC | 0.00 |

Wells Fargo has more than doubled investors' money over the past five years, yet its current checks suggest the stock still trades at a discount, with both the intrinsic value estimate and earnings multiples pointing to potential undervaluation rather than excess optimism.

- A 114.5% return over five years suggests Wells Fargo has already rewarded patient shareholders, so any perceived discount now matters more for future risk and reward.

- Recent earnings strength and higher capital returns can support the market's confidence in Wells Fargo, while regulatory and credit cycle risks may limit how far investors are willing to re rate the stock.

- On Simply Wall St's broader checks, Wells Fargo screens as undervalued in 4 out of 6 tests, which presents a mixed picture rather than a clear, across the board bargain.

The issue now is whether that apparent discount reflects a genuine margin of safety in Wells Fargo's valuation or a fair pricing of the risks that still sit around the story.

Is Wells Fargo a Bargain on Excess Returns?

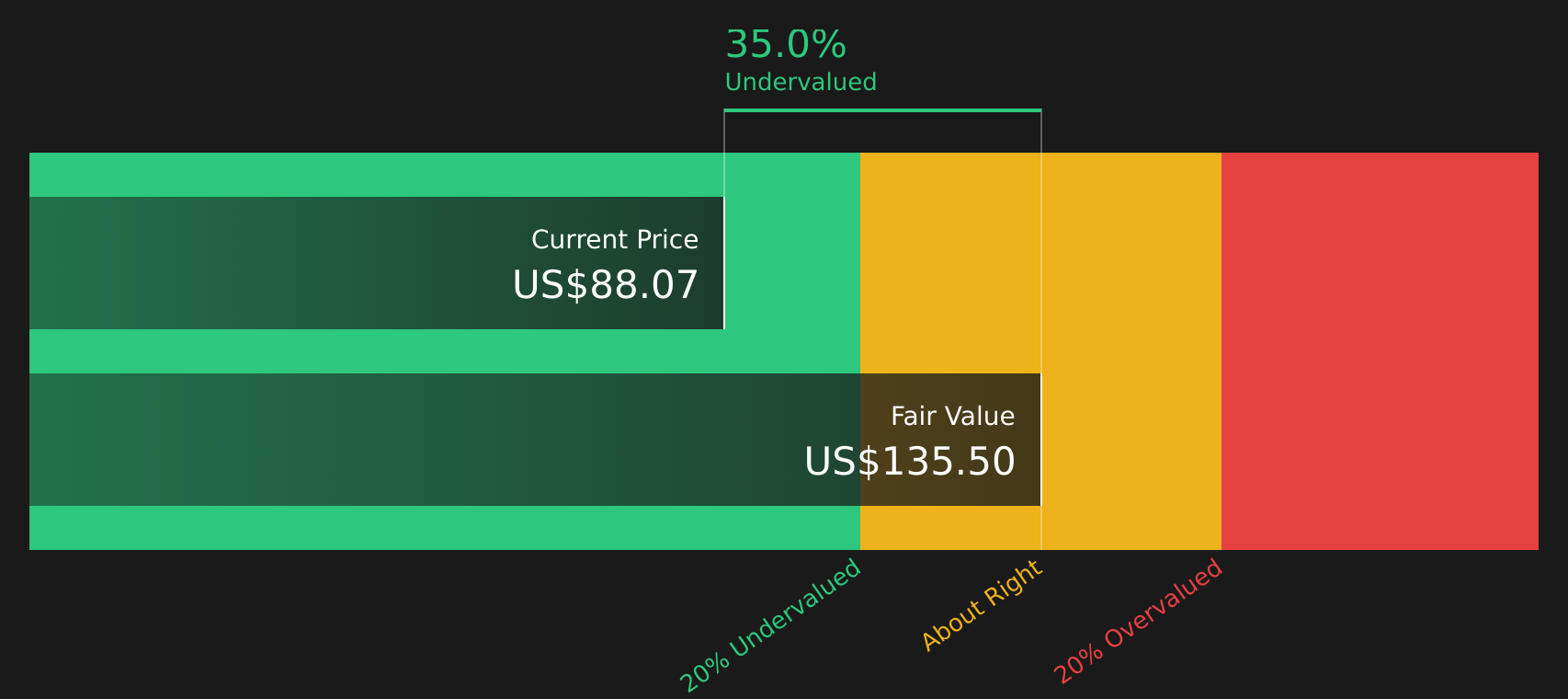

The Excess Returns model looks at how much profit Wells Fargo can earn above its cost of equity over time. For Wells Fargo, the inputs point to a bank earning more than its required return on capital, with stable EPS projected at $8.03 per share, a cost of equity of $4.79 per share, and an excess return of $3.24 per share. That rests on an average return on equity of 13.32% and a stable book value moving from $53.21 per share today toward $60.31 per share.

On these assumptions, the Excess Returns model arrives at an intrinsic value of about $133.73 per share, which implies the stock is 36.2% undervalued relative to the current price. Because the latest Q2 2026 results showed Wells Fargo reporting a 17.7% return on tangible common equity and returning cash through buybacks and planned dividend increases, the market may be slower to reflect those excess returns in the share price.

Overall, the Excess Returns analysis suggests Wells Fargo currently screens as undervalued against its estimated intrinsic value.

Our Excess Returns analysis suggests Wells Fargo is undervalued by 36.2%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Does Wells Fargo Look Undervalued on Earnings?

The P/E ratio is a useful quick check for Wells Fargo because earnings are a central driver of how investors typically value large, mature banks. Right now, Wells Fargo trades on a P/E of about 12.6x, which is slightly above the Banks industry average of 12.2x but below the peer group average of 14.4x. That puts the stock in a middle ground, not the lowest in its sector, yet not priced as highly as some large bank peers.

On Simply Wall St’s fair P/E estimate of 14.8x, which reflects Wells Fargo’s size, profitability and risk profile, the current 12.6x implies the stock trades at a discount to what this framework suggests investors might normally be willing to pay. The gap indicates investors are not paying a premium multiple for Wells Fargo despite its earnings base and sector position.

On this P/E yardstick, Wells Fargo stock appears undervalued relative to the level implied by the fair multiple model.

The Wells Fargo Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Wells Fargo pick up where the valuation checks leave off by spelling out which paths for Wells Fargo's growth, margins and earnings would need to hold for the stock to be worth materially more or less than today's price on the Community page. Each narrative links a specific set of catalysts and risks to an implied fair value, so you can see over time which version of Wells Fargo's story appears to be unfolding.

Share your own Wells Fargo Narrative to build a number-driven case on the stock, including your view on whether the recent earnings strength and higher shareholder returns justify today’s pricing, and track how your thesis holds up as new results and news arrive.

Do you think there's more to the story for Wells Fargo? Head over to our Community to see what others are saying!

The Bottom Line

Wells Fargo screens as undervalued on both the Excess Returns intrinsic value estimate and its current earnings multiple, but the broader checks still point to a mixed picture rather than an outright bargain. The key question is whether the market is underestimating the durability of those excess returns or correctly weighing ongoing regulatory and credit related risks. For you, the crux is simple: does that discount represent a margin of safety that compensates for those risks, or is it a warning that the market expects a ceiling on how far the stock can re rate from here?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.