West (WST) Stock Looks Fair On Cash Flow Yet Pricey On Earnings

West Pharmaceutical Services, Inc. WST | 0.00 |

West Pharmaceutical Services has delivered a 64.1% return over the past year, and after that kind of run the stock no longer looks obviously cheap, especially with most of the valuation checks leaning toward a premium price tag. The Discounted Cash Flow (DCF) intrinsic value estimate points to a roughly fair valuation, while market based multiples suggest the shares are priced on the rich side.

- West Pharmaceutical Services' 64.1% 1 year return puts recent momentum front and center, which can limit the margin of safety for new investors if fundamentals do not keep pace.

- Recent moves to deepen its partnership with Daikyo Seiko and refocus the SmartDose platform on larger volume systems may support long term growth expectations, while execution risk around portfolio reshaping and product development can still affect how much investors are prepared to pay today.

- On Simply Wall St's broader checks, West Pharmaceutical Services is flagged as cheap in 0 of 6 valuation tests, which means the stock currently leans expensive rather than a clear bargain based on this valuation summary.

The issue now is whether West Pharmaceutical Services' current price fairly reflects its intrinsic value, or if the strong share price performance has pushed it beyond what the fundamentals justify.

Is West Pharmaceutical Services Fairly Priced on Cash Flow?

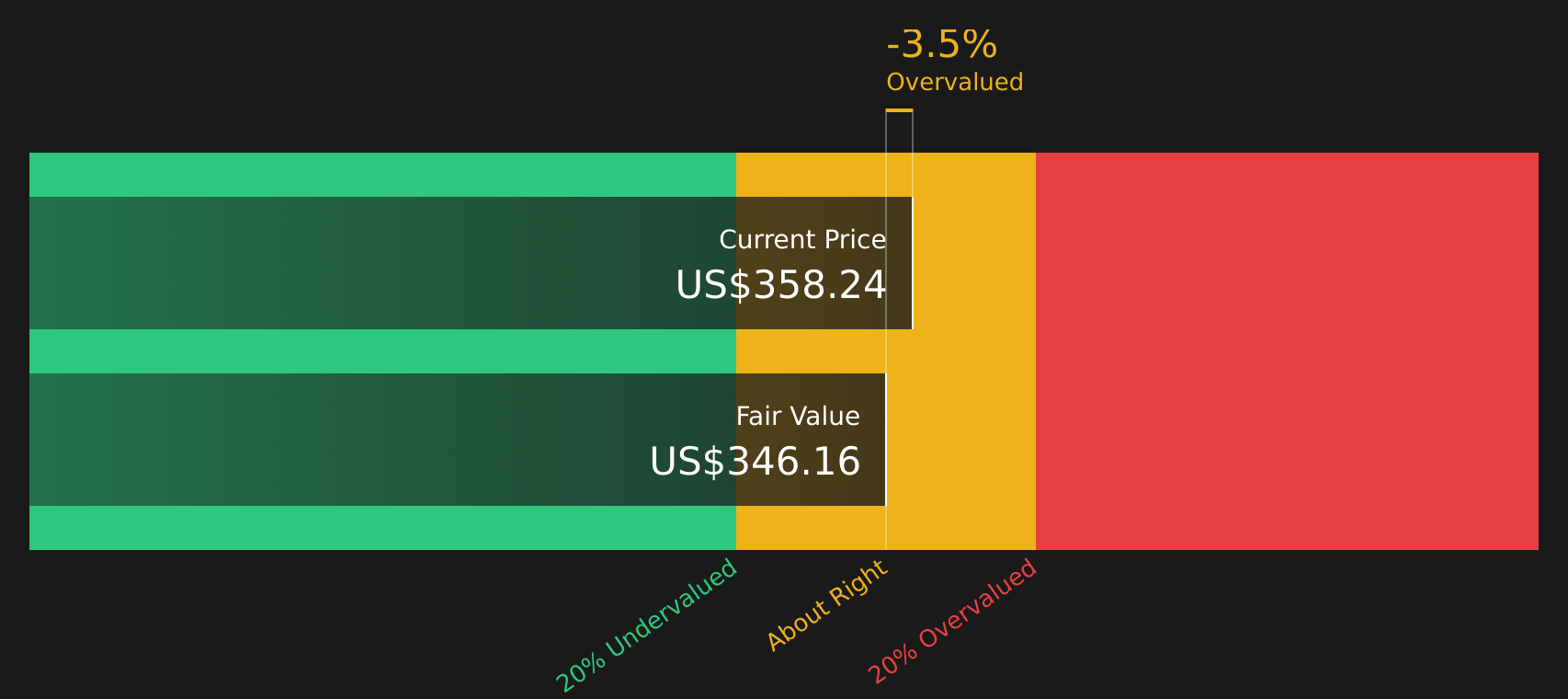

The Discounted Cash Flow (DCF) model estimates what West Pharmaceutical Services could be worth based on its projected cash generation. On the latest twelve month figures, the company produced around $364.4 million of free cash flow, and the model applies a growing cash flow profile over time to reflect expectations that West Pharmaceutical Services can build on its current earnings base.

On this basis, the DCF points to an intrinsic value of about $345 per share, which sits slightly below the current share price and implies the stock is roughly 5% overvalued. The recent sale of the SmartDose 3.5mL system to AbbVie, together with the focus on larger volume delivery solutions, helps explain why investors may be willing to pay a premium to these cash flow estimates.

Overall, the DCF workup suggests West Pharmaceutical Services appears to be roughly fairly valued, with the current price sitting close to its intrinsic value estimate.

West Pharmaceutical Services is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Is West Pharmaceutical Services Getting Expensive on Earnings?

The P/E ratio is a useful yardstick for West Pharmaceutical Services because earnings remain a key driver for how the market values this kind of established healthcare supplier.

Right now, West Pharmaceutical Services trades on a P/E of about 47.2x, compared with a Life Sciences industry average of roughly 41.0x and a peer average near 43.1x. On Simply Wall St's fair ratio framework, which looks at what multiple might make sense given the company’s growth profile, margins, size and risk, a P/E closer to 23.0x would be more in line with those fundamentals.

That leaves the current P/E sitting well above both the tailored fair ratio and the broader sector benchmarks. This suggests investors are paying a clear premium for West Pharmaceutical Services stock at today’s price.

On the P/E measure, West Pharmaceutical Services currently looks overvalued compared with what the fair ratio and industry context would imply.

The West Pharmaceutical Services Narrative: What Would Justify Today's Price?

Simply Wall St Narratives take the valuation puzzle around West Pharmaceutical Services a step further by spelling out which assumptions about future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today, and they sit on Simply Wall St's Community page. Each one treats fair value as a thesis about how West Pharmaceutical Services' business might develop over time, so you can see how that view holds up as new information arrives.

You can add your voice to the Simply Wall St community by sharing a Narrative on West Pharmaceutical Services that lays out a numbers based view on how the expanded Daikyo Seiko agreements and the SmartDose 3.5mL sale to AbbVie might shape the company from here. Set out your case today and see how it stacks up as West Pharmaceutical Services' results and news flow develop over time.

Do you think there's more to the story for West Pharmaceutical Services? Head over to our Community to see what others are saying!

The Bottom Line

For West Pharmaceutical Services, the Discounted Cash Flow (DCF) work suggests the stock is trading close to intrinsic value, while the P/E multiple indicates it is overvalued compared with both peers and a tailored fair ratio. That split comes down to cash flows broadly supporting today’s level, but a market price that assumes generous growth and margin resilience. With broader valuation checks still weak, the key question is whether West Pharmaceutical Services can deliver the earnings progress and execution on its portfolio reshaping that would keep investors comfortable paying a premium multiple from here.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.