Weyerhaeuser (WY) Could Be 3% Undervalued As Valuation Questions Follow 2025 Results

Weyerhaeuser Company WY | 0.00 |

Weyerhaeuser (WY) is drawing investor attention after reporting 2025 net sales of US$6.9b and net income of US$397m, prompting closer scrutiny of how the timber and wood products business is currently valued.

Recent trading has been positive, with Weyerhaeuser's share price delivering a 1 day return of 3.52%, a 30 day share price return of 6.93% and a 90 day share price return of 7.20%. Over the same period, the 3 year total shareholder return declined 16.52%, suggesting that near term momentum contrasts with weaker longer term results.

If the recent move in Weyerhaeuser has you thinking about other opportunities, this is a good moment to scan 29 best rare earth metal stocks for potential ideas in the broader materials space.

With Weyerhaeuser generating US$6.9b in net sales and US$397m in net income, plus mixed short and longer term returns, the key question is whether the current share price offers an attractive entry point or if markets are already fully reflecting the company’s prospects.

Most Popular Narrative: 2.7% Undervalued

Based on the most followed narrative, Weyerhaeuser's fair value of $26.00 sits slightly above the last close at $25.30, putting a modest valuation gap in focus.

Construction of the US$500 million Monticello engineered wood facility through 2027 and the company’s focus on aligning output with single family starts position Wood Products to benefit when housing and repair and remodel volumes recover, which could help lift revenue and improve operating leverage.

Curious what justifies that fair value for Weyerhaeuser? The narrative refers to specific revenue paths, margin shifts and a future earnings multiple that is described as anything but conservative.

Result: Fair Value of $26.00 (UNDERVALUED)

However, there are still clear swing factors, including stronger than expected housing and repair activity or faster growth in Natural Climate Solutions, that could challenge this Weyerhaeuser narrative.

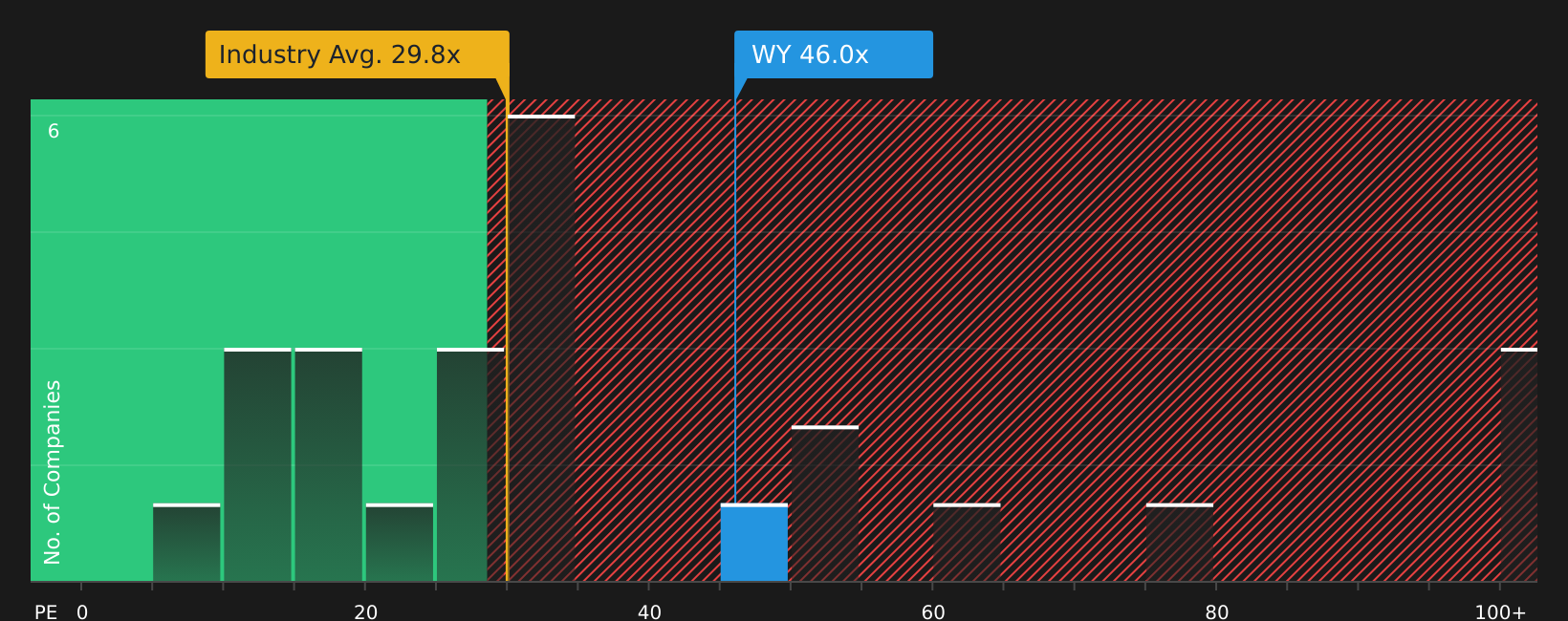

Another View: What Weyerhaeuser's P/E Is Telling You

The narrative fair value of $26.00 suggests Weyerhaeuser is slightly undervalued, but the P/E ratio of 46x tells a tougher story. That multiple sits above the US Specialized REITs industry at 29.5x, the peer average at 42x and even the 43.8x fair ratio. This points to valuation risk if expectations cool.

For investors comparing these signals, the key question is whether the earnings outlook justifies Weyerhaeuser holding a premium multiple over its sector, peers and the fair ratio, or whether the market could eventually drift closer to those lower reference points.

Next Steps

With Weyerhaeuser showing both appealing elements and clear valuation questions, this is a moment to act promptly and evaluate the story against your own judgement using 3 key rewards and 3 important warning signs.

Looking for more Weyerhaeuser style investment ideas?

If Weyerhaeuser has sharpened your focus on valuation and quality, you can use this momentum to broaden your watchlist with a few carefully selected stock ideas.

- Target potential bargains early by scanning companies that look mispriced on fundamentals through the 44 high quality undervalued stocks.

- Strengthen your income stream by reviewing dependable payers with the 7 dividend fortresses before the next round of payouts passes you by.

- Stay defensively positioned by checking the 69 resilient stocks with low risk scores and focus on businesses with more resilient profiles when markets shift.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.