Weyerhaeuser (WY) Faces Earnings Pressure, Is The 24% Undervalued View Enough?

Weyerhaeuser Company WY | 0.00 |

Weyerhaeuser (WY) is back in focus as the company prepares to release its second quarter earnings, with analysts looking for diluted FFO of $0.10 per share, implying a 16.7% decline year over year.

At a share price of $23.79, Weyerhaeuser has seen recent momentum soften, with a 7 day share price return that declined 7.65% and a 30 day share price return that declined 2.46%, while the 1 year total shareholder return declined 6.8%. This points to fading performance rather than a strong rebound so far.

If earnings season has you reassessing your watchlist, this can be a useful moment to look beyond timber and check out 35 power grid technology and infrastructure stocks

With Weyerhaeuser trading at $23.79 and sitting at a discount to the average analyst price target, the key question is whether the current weakness signals undervaluation or whether the market already reflects the company’s future growth potential.

Most Popular Narrative: 23.7% Undervalued

With Weyerhaeuser last closing at $23.79 against a narrative fair value of $31.18, the widely followed view is building in a clear valuation gap based on long term cash flow assumptions and margin expectations.

The carbon capture and sequestration (CCS) agreement with Occidental Petroleum represents a growth opportunity in Weyerhaeuser's Natural Climate Solutions business, likely boosting future earnings. Ongoing construction of the EWP facility in Arkansas and return to normal operations at the Montana facility will drive increased production, positively impacting revenue and net margins.

Curious how that CCS deal and new mills translate into a higher fair value for Weyerhaeuser? The narrative leans on rising efficiency, richer margins and a future earnings profile that assumes far stronger profitability than today. Want to see which growth, margin and valuation hurdles have to be cleared to support that $31.18 figure?

Result: Fair Value of $31.18 (UNDERVALUED)

However, that upside narrative for Weyerhaeuser still runs into real tests, including weaker lumber demand tied to cautious housing activity and the ongoing ban on U.S. log imports by China.

Another View On Weyerhaeuser’s Valuation

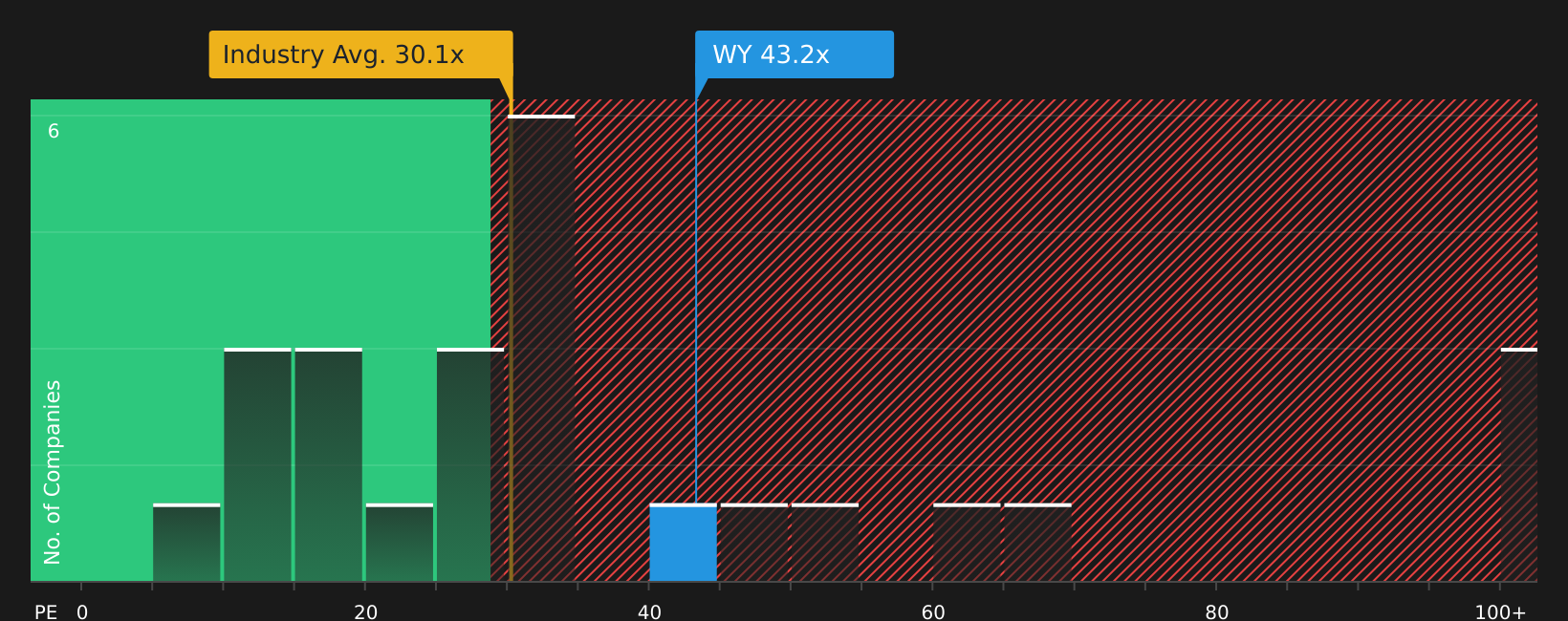

The narrative fair value for Weyerhaeuser points to upside, but the P/E ratio tells a more cautious story. At 43.2x earnings, the stock trades above the US Specialized REITs average of 30.1x and even its own 41.8x peer average, while the fair ratio sits higher at 45.1x. This gap could indicate either additional potential or increased valuation risk if sentiment cools.

For a closer look at how these P/E comparisons stack up and what the fair ratio might imply if the market shifts toward it, take a moment to review the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Mixed signals around Weyerhaeuser’s valuation and outlook are clear, so this is a useful moment to weigh the trade off between risk and reward for yourself. If you want a quick way to see how others are balancing those views, start with 3 key rewards and 3 important warning signs

Looking for more investment ideas beyond Weyerhaeuser?

If Weyerhaeuser has you rethinking your portfolio mix, use this moment to scan fresh ideas that match your style before the next wave of earnings shifts sentiment again.

- Target reliable income by reviewing companies in the 7 dividend fortresses and see which yields stand out for consistency and scale.

- Spot potential mispricings early by scanning the 43 high quality undervalued stocks and compare valuations before attention catches up.

- Prioritize resilience by working through the 75 resilient stocks with low risk scores and focus on businesses with more measured risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.