What Bank of America (BAC)'s Higher Net Interest Income Outlook and AI Push Means For Shareholders

Bank of America Corp BAC | 0.00 |

- Over recent days, Bank of America has been active across funding and governance, completing multiple fixed‑rate senior note offerings, supporting new financing initiatives in advanced manufacturing and defense, and reporting shareholder votes that rejected proposals for an independent chair and expanded animal-welfare risk oversight.

- At the same time, the bank’s role in AI‑enabled bond trading platforms and its raised net interest income guidance after the latest Federal Reserve decision underline how technology investment and interest rate positioning are reshaping its business mix.

- Next, we’ll examine how Bank of America’s stronger net interest income outlook influences its existing investment narrative built around digital transformation.

The latest GPUs need a type of rare earth metal called Dysprosium and there are only 33 companies in the world exploring or producing it. Find the list for free.

Bank of America Investment Narrative Recap

To own Bank of America, you need to believe in a large, tech-focused bank that is leaning into digital engagement and disciplined balance sheet management, with net interest income as a key earnings driver. The latest guidance upgrade for net interest income, following the Federal Reserve’s decision, supports that near term catalyst, while credit quality and deposit competition remain the biggest risks. Recent funding, governance votes, and AI trading initiatives do not materially alter that risk reward balance.

The most relevant recent update is Bank of America’s raised full year net interest income guidance after the Fed held rates steady, especially when set against a backdrop of no expected 2026 rate cuts in its own economics team outlook. For shareholders, that guidance ties directly into the existing narrative that interest rate management and asset repricing, alongside heavy digital and AI investment, are central to how the bank is trying to grow earnings efficiently.

Yet against this stronger income outlook, investors should also be aware of rising competition for deposits and what that could mean for...

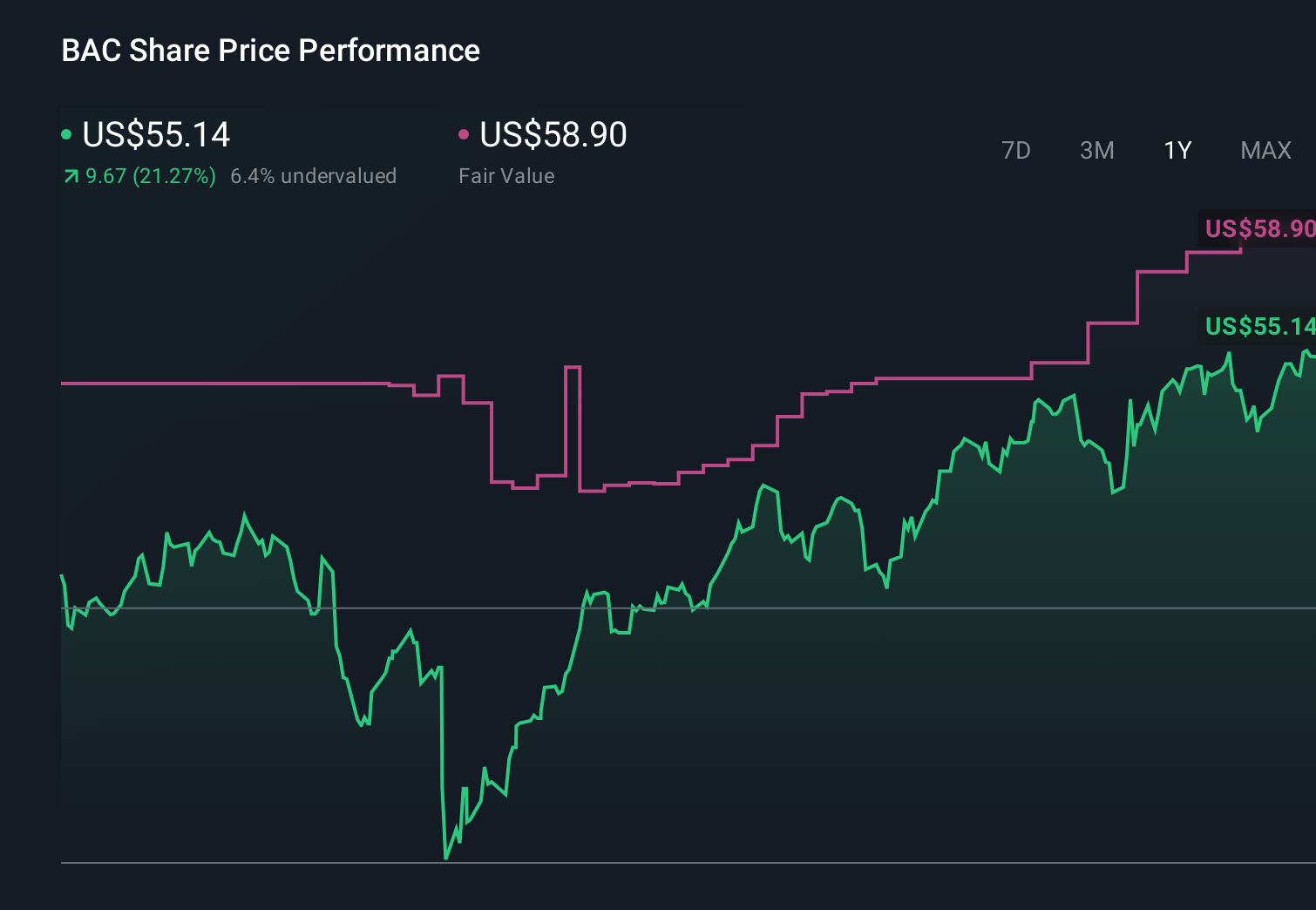

Bank of America's narrative projects $133.8 billion revenue and $36.7 billion earnings by 2029. This requires 6.9% yearly revenue growth and about a $6.4 billion earnings increase from $30.3 billion today.

Uncover how Bank of America's forecasts yield a $62.98 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Eight members of the Simply Wall St Community currently see Bank of America’s fair value between US$58 and about US$66.6, showing a fairly tight cluster of views. You can weigh those opinions against the recent net interest income upgrade and consider how shifts in deposit pricing or credit costs could affect the bank’s ability to sustain its current earnings profile.

Explore 8 other fair value estimates on Bank of America - why the stock might be worth just $58.00!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Bank of America research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bank of America research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank of America's overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.