What Bank of America (BAC)'s Preferred Redemption and Card Revamp Means for Shareholders

Bank of America Corp BAC | 54.31 | +1.81% |

- In early February 2026, Bank of America detailed plans to redeem its Series DD preferred stock next year while aggressively reworking its credit card offerings, aiming to grow its consumer customer base and enhance profits using data and artificial intelligence.

- This combination of balance-sheet reshaping and a heavier push into higher-margin consumer credit highlights how the bank is recalibrating its mix of funding and growth engines.

- We’ll now examine how Bank of America’s renewed credit card push and broader consumer expansion efforts influence its longer-term investment narrative.

Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

What Is Bank of America's Investment Narrative?

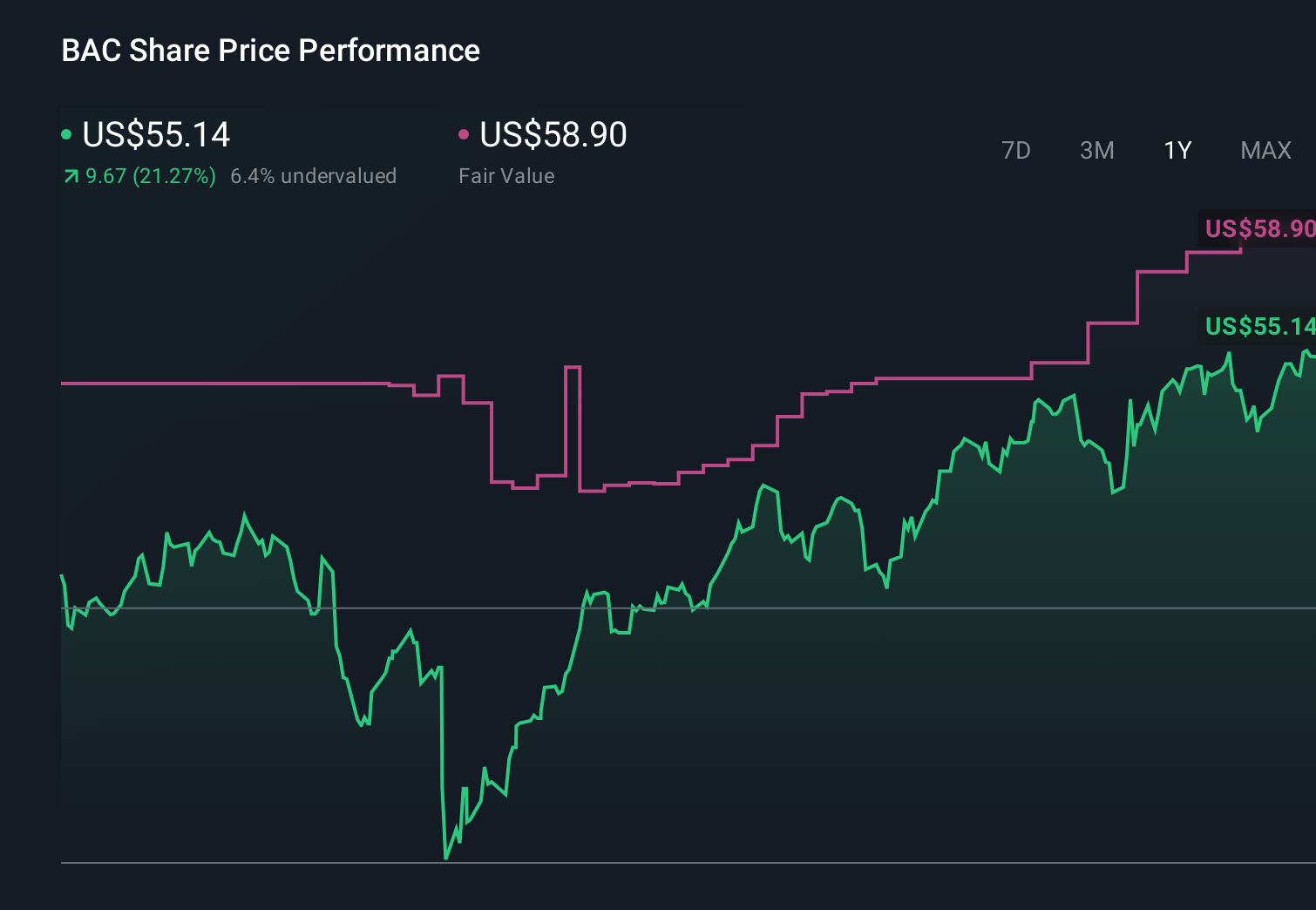

To own Bank of America, you really need to believe in a large, diversified franchise that compounds value through steady earnings, disciplined balance sheet management and a consistent dividend, rather than dramatic growth. The latest moves fit that story: redeeming the Series DD preferred stock and issuing new senior notes look like routine capital and funding housekeeping, while the credit card overhaul is more central to the investment case. Management is leaning harder into higher-margin consumer credit, data and AI to support mid‑single‑digit earnings growth on a roughly US$107.42 billion revenue base, even as buybacks pause and the dividend yield screens less generous after a strong multi‑year total return. Near term, key catalysts still sit around rate expectations, credit quality and execution in consumer, with the preferred redemption itself unlikely to be a material swing factor for the stock.

However, the bigger risk is that a sharper tilt to consumer credit could bring more earnings volatility if conditions change. Bank of America's shares have been on the rise but are still potentially undervalued by 17%. Find out what it's worth.Exploring Other Perspectives

Seventeen fair value estimates from the Simply Wall St Community span roughly US$43 to US$66 per share, showing how far private investors can differ on Bank of America’s worth. Set against that spread, the bank’s shift toward more credit card driven consumer profits and a pause in buybacks put more weight on how comfortably you think it can manage funding costs, credit risk and regulation over the next few years.

Explore 17 other fair value estimates on Bank of America - why the stock might be worth as much as 20% more than the current price!

Build Your Own Bank of America Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Bank of America research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Bank of America research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank of America's overall financial health at a glance.

Ready For A Different Approach?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Find 55 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.