What Bio-Techne (TECH)'s New Refeyn Partnership Means For Shareholders

Bio-Techne TECH | 0.00 |

- Earlier this week, Refeyn and Bio-Techne announced a first-of-its-kind integrated workflow that links Bio-Techne’s MauriceFlex™ icIEF fractionation system with Refeyn’s TwoMP mass photometry platform, enabling four-hour, single-molecule characterization of charge and size variants in bispecific antibodies and biosimilars using nanogram-level samples.

- This pairing allows researchers to directly connect charge heterogeneity with molecular weight and aggregation in a single streamlined workflow, reducing dependence on multiple assays and potentially improving the efficiency of complex biotherapeutic development and process characterization.

- We’ll now examine how this MauriceFlex–TwoMP workflow, which tightens Bio-Techne’s role in complex biologics characterization, influences its investment narrative.

Find 47 companies with promising cash flow potential yet trading below their fair value.

Bio-Techne Investment Narrative Recap

To own Bio-Techne, you have to believe its specialized tools can stay embedded in complex biologics, cell therapy, and diagnostics workflows despite slow organic growth and compressed returns on capital. The MauriceFlex–TwoMP launch reinforces the high-value instrumentation and workflow story, but it does not meaningfully shift the near term catalyst, which is a return to consistent organic revenue growth, or the key risk, that prolonged funding and pricing pressure could keep margins and ROIC under strain.

Among recent announcements, the April 2026 brand simplification into three portfolio pillars (R&D Systems, Bio-Techne Spatial, Bio-Techne Diagnostics) is most relevant here, because it is all about clarifying where growth and margins should come from. Cleaner branding around platforms like Maurice and COMET can make these types of integrated workflows easier to position with pharma and diagnostic customers, which matters if investors are counting on higher mix toward instruments and recurring consumables to support earnings recovery.

But while this innovation story is attractive, investors should also be aware that prolonged weakness in core consumables demand and shrinking returns on capital could still...

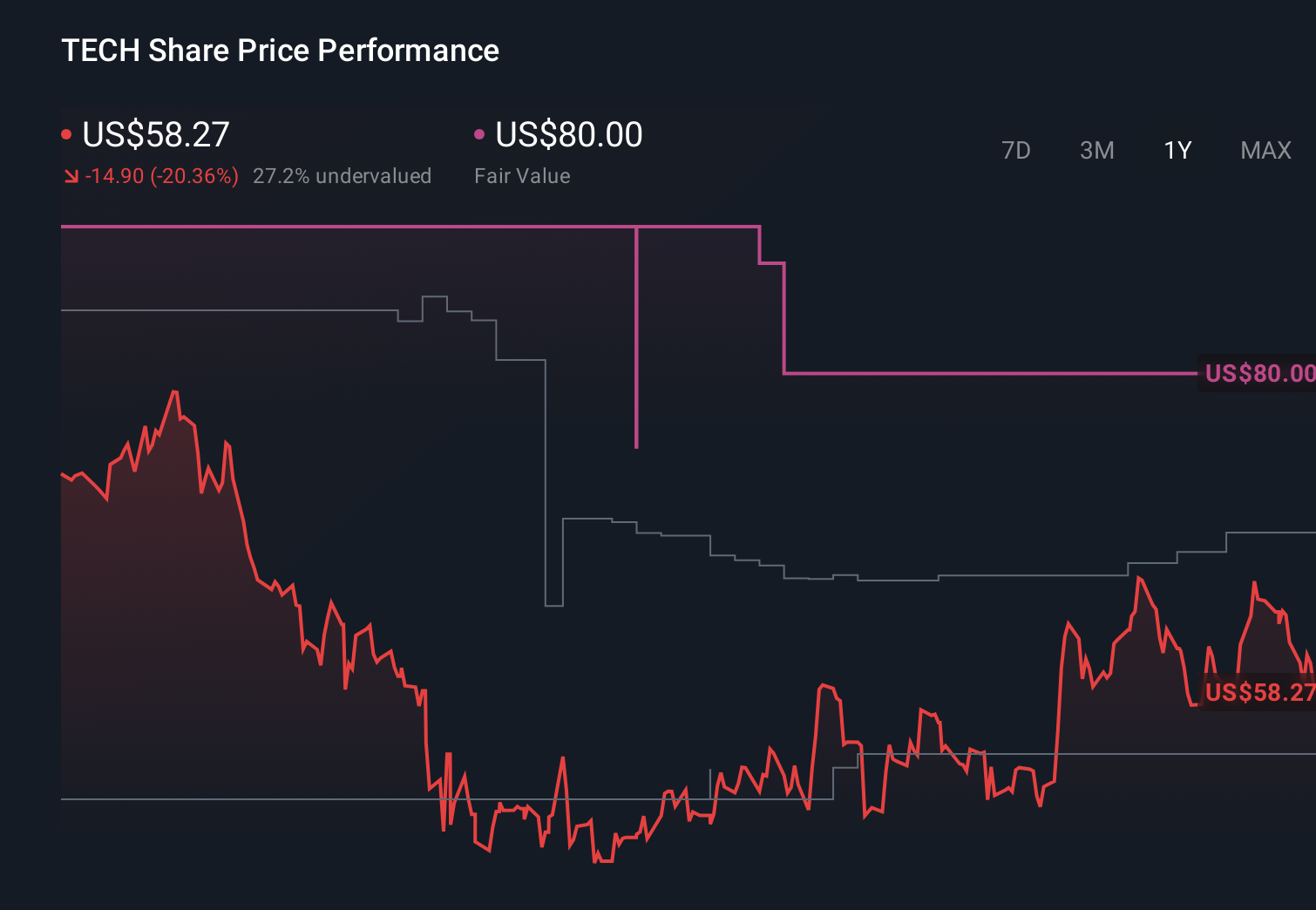

Bio-Techne's narrative projects $1.4 billion revenue and $281.1 million earnings by 2029.

Uncover how Bio-Techne's forecasts yield a $61.42 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$1.5 billion and earnings US$307.9 million by 2029, so if you are weighing this new MauriceFlex–TwoMP collaboration against that bullish path, it helps to remember that others worry heavy reliance on legacy consumables could cap the upside, which shows just how far apart reasonable views on Bio-Techne’s trajectory can be.

Explore 4 other fair value estimates on Bio-Techne - why the stock might be worth just $52.22!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Bio-Techne research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

- Our free Bio-Techne research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bio-Techne's overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.