What Bruker (BRKR)'s Mixed Q1 2026 Results and Reaffirmed Guidance Means For Shareholders

Bruker Corporation BRKR | 0.00 |

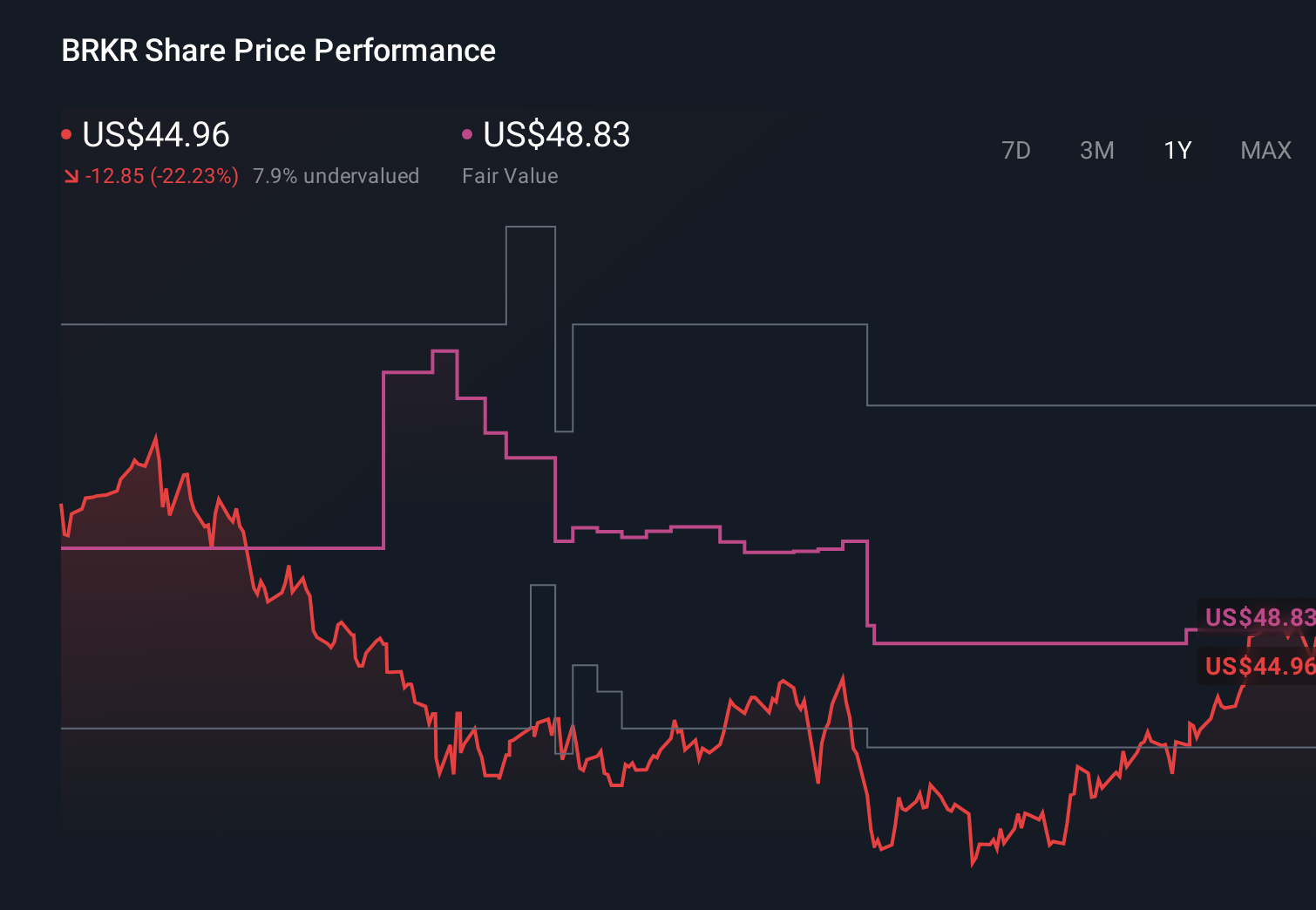

- Bruker Corporation recently reported first-quarter 2026 results, with sales rising to US$823.4 million from US$801.4 million a year earlier, while net income eased to US$14.4 million, and it reconfirmed full-year 2026 revenue guidance of US$3.57 billion to US$3.60 billion.

- The combination of higher quarterly sales but lower earnings, alongside unchanged full-year revenue expectations, highlights how Bruker is balancing growth investments and cost pressures as it enters the rest of 2026.

- We will now examine how Bruker’s reaffirmed 2026 revenue guidance shapes its existing investment narrative and future earnings expectations.

The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Bruker Investment Narrative Recap

To own Bruker, you need to believe its portfolio in advanced analytical and diagnostic tools can translate into steadier profits despite uneven funding and cost pressures. The latest quarter, with higher sales but softer earnings and reaffirmed 2026 revenue guidance, does not materially alter that near term. It does, however, keep execution on margin recovery as the key short term catalyst, while persistent pressure on research budgets in the US and China remains the central risk.

The reaffirmed full year 2026 revenue outlook of US$3.57 billion to US$3.60 billion is the announcement that most closely ties to these results, because it signals management’s confidence in modest growth despite a weak start to earnings. That guidance sits alongside a deep product pipeline in areas like spatial biology and diagnostics, which many investors see as potential longer term supports for both revenue mix and recurring sales, if demand conditions stabilize.

Yet, against this steady revenue guidance, investors should be aware that...

Bruker's narrative projects $4.0 billion revenue and $332.4 million earnings by 2029.

Uncover how Bruker's forecasts yield a $49.15 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts paint a tougher picture, assuming only about 4 percent annual revenue growth to roughly US$3.9 billion and placing more weight on risks like weaker order intake and prolonged funding softness, so you may want to compare their expectations with your own view of Bruker’s latest quarter and guidance.

Explore 4 other fair value estimates on Bruker - why the stock might be worth as much as 14% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Bruker research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bruker research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bruker's overall financial health at a glance.

Curious About Other Options?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are the new gold rush. Find out which 33 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.