What Carvana (CVNA)'s Expansion of Tracy Reconditioning Facilities Means For Shareholders

Carvana CVNA | 0.00 |

- Carvana recently announced it is adding Inspection and Reconditioning Center capabilities to its ADESA Golden Gate auction site in Tracy, California, expanding reconditioning capacity and bringing approximately 100 new jobs to the area.

- This integration enhances both retail and wholesale operations, supporting faster delivery times for local customers and offering expanded capabilities for wholesale buyers in the region.

- We'll explore how Carvana's expanded reconditioning footprint could impact its long-term growth narrative and operational efficiency outlook.

Find companies with promising cash flow potential yet trading below their fair value.

Carvana Investment Narrative Recap

Owning Carvana shares requires a belief in its ability to scale its online used-car marketplace by overcoming operational challenges, particularly in reconditioning and logistics. The recent expansion of Inspection and Reconditioning Center capabilities at the ADESA Golden Gate site bolsters operational capacity, but its effect on near-term catalysts, primarily unit growth from faster delivery and broader inventory, remains relatively modest. Risks around margin pressure and ramp-up efficiency are still front and center for investors considering the stock.

Carvana’s launch of same-day vehicle delivery in the Seattle area this September offers a strong parallel to its expanded Bay Area footprint, illustrating ongoing investments to enhance speed and convenience for customers. These service advancements highlight the company’s focus on addressing a core catalyst: accelerating consumer adoption of its online buying platform, which remains key to sustaining ambitious growth targets.

In contrast, investors should keep a close watch on potential cost overruns and utilization delays from these expansions, as these factors...

Carvana's outlook projects $33.2 billion in revenue and $2.2 billion in earnings by 2028. This is based on a 26.8% annual revenue growth rate and a $1.6 billion increase in earnings from the current $563.0 million.

Uncover how Carvana's forecasts yield a $414.20 fair value, a 14% upside to its current price.

Exploring Other Perspectives

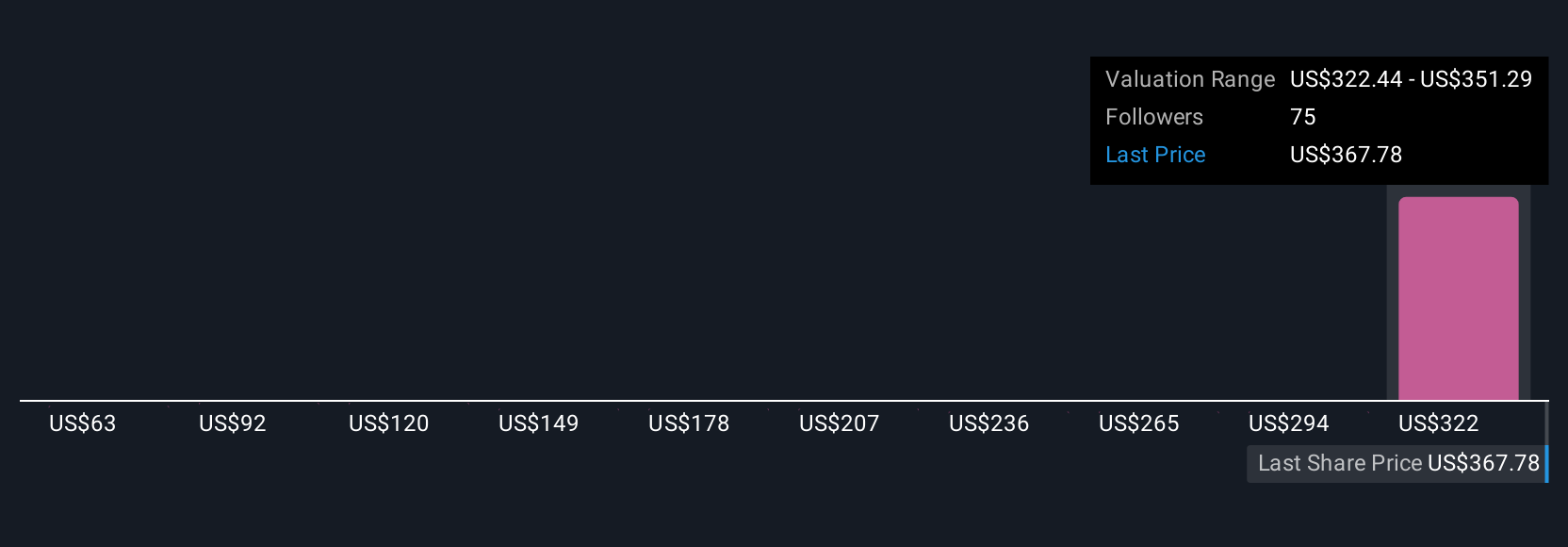

Fifteen fair value estimates from the Simply Wall St Community range from US$62.76 to US$500 per share. While investors’ views differ widely, many are weighing Carvana’s need to ramp up operational efficiency against the risk of cost overruns impacting future performance.

Explore 15 other fair value estimates on Carvana - why the stock might be worth as much as 38% more than the current price!

Build Your Own Carvana Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Carvana research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Carvana research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carvana's overall financial health at a glance.

Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.