What Centene (CNC)'s Margin Improvement Outlook Means For Shareholders

Centene Corporation CNC | 0.00 |

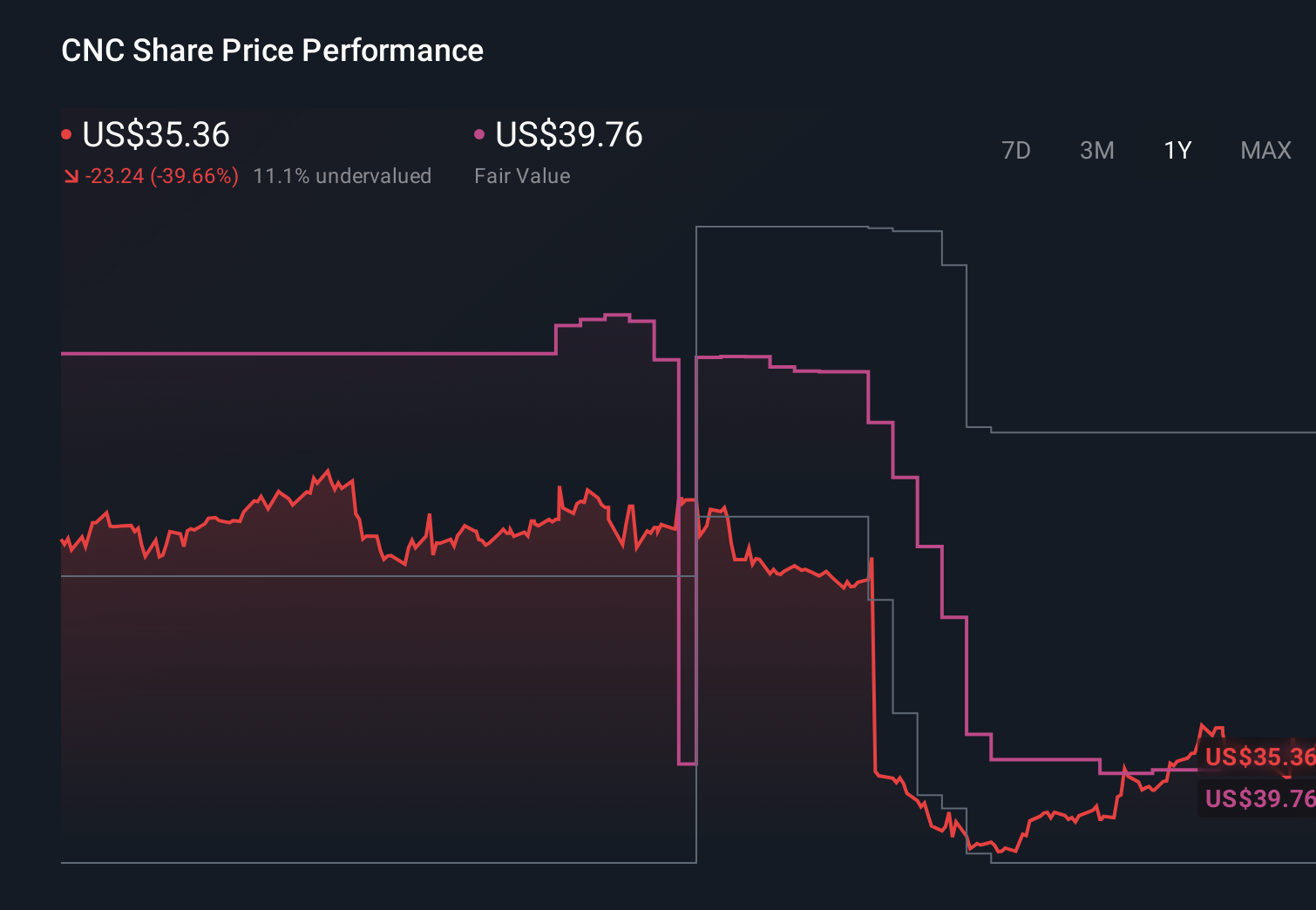

- In recent days, Centene reported that management sees improved profitability across its Medicaid, Marketplace and Medicare businesses, following meetings with Truist that highlighted margin improvement opportunities and operational progress.

- This upbeat management commentary contrasts with earlier concerns about subdued customer growth and falling earnings per share despite higher revenue, underscoring how margin quality rather than simple top-line expansion has become a central focus for the company.

- Next, we’ll explore how this improved margin outlook, particularly in Medicaid, may influence Centene’s existing investment narrative and risk profile.

Outshine the giants: these 22 early-stage AI stocks could fund your retirement.

Centene Investment Narrative Recap

To own Centene, you need to believe that its large Medicaid, Marketplace and Medicare footprint can eventually translate scale into consistent, higher quality margins, not just more revenue. The Truist meetings, where management pointed to improving profitability across these segments, support that margin-first story and may soften the biggest near term worry around Medicaid earnings pressure. At the same time, they do little to remove key risks tied to policy changes and unexpected medical cost spikes.

The most relevant recent announcement is Centene’s 2026 guidance, which points to US$186.5 billion to US$190.5 billion in revenue and positive GAAP diluted EPS above US$1.98. Put alongside management’s comments about better Medicaid, Marketplace and Medicare profitability, that guidance frames the main short term catalyst as execution on margin recovery after a year of sizeable losses, rather than sheer top line expansion or contract wins alone.

Yet beneath this improving margin story, investors should still be aware of how dependent those margins are on future Medicaid rate adequacy and...

Centene's narrative projects $195.6 billion revenue and $2.1 billion earnings by 2028.

Uncover how Centene's forecasts yield a $44.18 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already penciling in about US$215.7 billion of revenue and US$2.7 billion of earnings by 2028, so if you lean toward that view, the latest margin commentary might look like early confirmation rather than a surprise. Others will see it as only a first data point, reminding you that reasonable people can disagree sharply on Centene’s potential and encouraging you to weigh several viewpoints before deciding what this new information means for you.

Explore 16 other fair value estimates on Centene - why the stock might be worth over 4x more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Centene research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Centene research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Centene's overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 45 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 28 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.