What EMCOR Group (EME)'s Rising Analyst Optimism Means For Shareholders

EMCOR Group, Inc. EME | 0.00 |

- In recent weeks, EMCOR Group has attracted upbeat analyst coverage, with firms such as Oppenheimer, Baird, William Blair and Zacks highlighting its record Remaining Performance Obligations backlog, strong first-quarter operational performance, and exposure to high-tech manufacturing and data center projects.

- This wave of positive research attention, combined with modest upward revisions to earnings estimates and a predominantly Buy-oriented recommendation base, underscores how EMCOR’s scale in complex construction and services markets is increasingly being recognized by Wall Street as a competitive strength.

- With this backdrop of more optimistic earnings revisions, we’ll examine how the strengthened analyst sentiment could influence EMCOR’s existing investment narrative.

Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

EMCOR Group Investment Narrative Recap

To own EMCOR Group, you need to believe its record US$15.62 billion Remaining Performance Obligations backlog and capabilities in complex projects can support attractive long term project activity, even as labor costs, industrial cyclicality and large project lumpiness remain key risks. Recent upbeat analyst coverage, modestly higher earnings estimates and strong first quarter results appear to support the near term earnings catalyst, but do not materially change the underlying execution and end market risks.

Among recent developments, Oppenheimer’s new Outperform rating and focus on EMCOR’s exposure to high tech manufacturing and data center work tie directly into that backlog driven earnings story. Combined with Baird’s higher price target and William Blair’s positive stance, this cluster of research reinforces the idea that EMCOR’s scale and specialization in complex construction and services are central to the current catalyst, even as investors weigh ongoing dependence on cyclical end markets.

But while optimism is building, investors should still be aware of how concentrated exposure to large, project based end markets could...

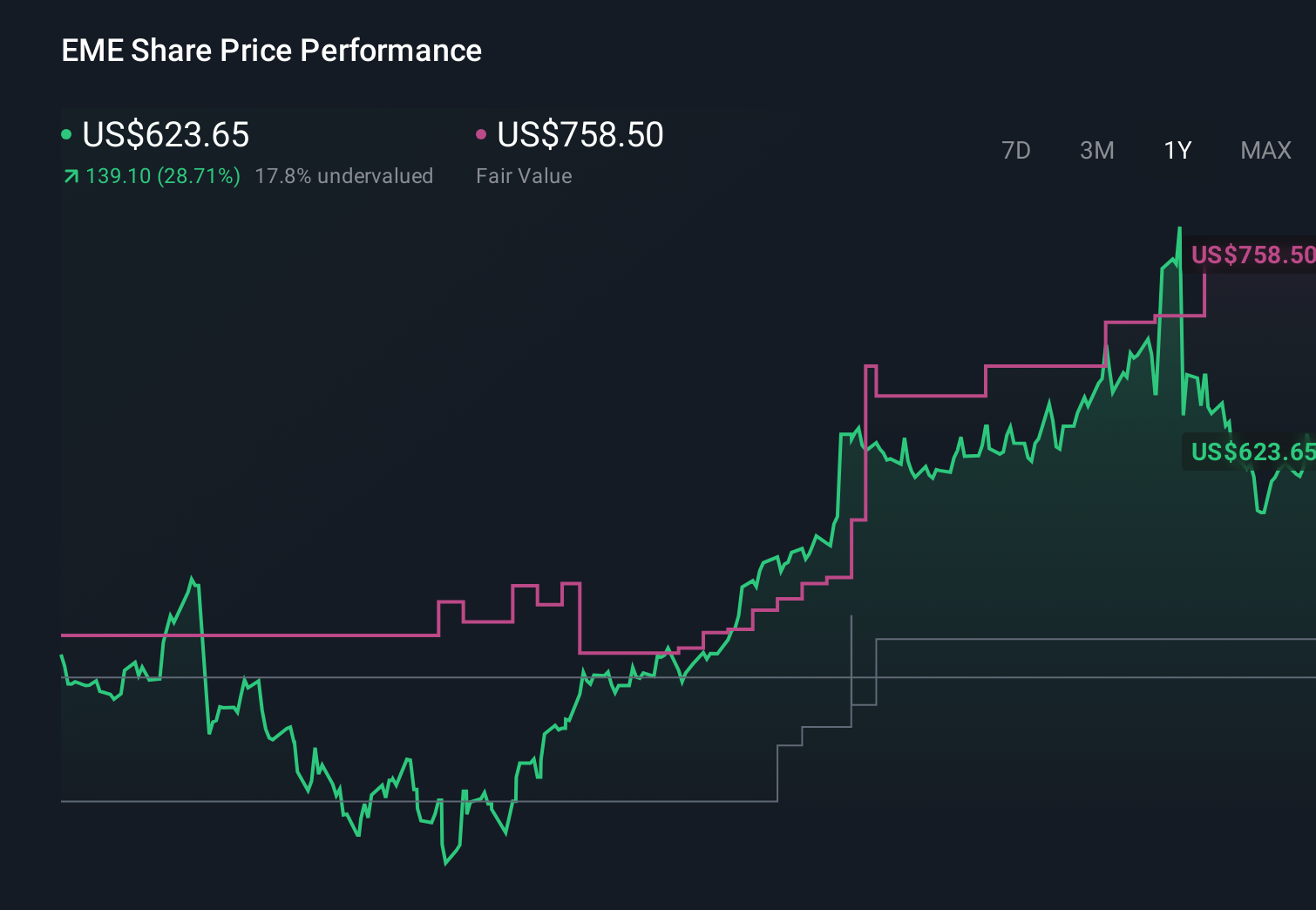

EMCOR Group's narrative projects $21.5 billion revenue and $1.6 billion earnings by 2029.

Uncover how EMCOR Group's forecasts yield a $983.50 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already penciling in about US$21.2 billion of revenue and US$1.4 billion of earnings by 2028, which is far more upbeat than consensus and leans heavily on recurring, higher margin work, yet this new wave of analyst enthusiasm and backlog data could either support that view or prompt a rethink of how much cyclicality and project risk you are really comfortable with.

Explore 5 other fair value estimates on EMCOR Group - why the stock might be worth just $885.00!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your EMCOR Group research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free EMCOR Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate EMCOR Group's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.