What Huntington Bancshares (HBAN)'s Texas Commercial Banking Expansion Means For Shareholders

Huntington Bancshares Incorporated HBAN | 0.00 |

- Huntington National Bank recently expanded its Huntington Commercial Bank operations into Austin and central Texas, building on earlier Texas bank acquisitions and appointing veteran commercial banker Claire Harrison as senior managing director to lead the regional push.

- This move signals Huntington’s intent to deepen its middle-market and corporate banking reach in a fast-growing region, potentially reshaping its commercial mix and geographic balance.

- We’ll now consider how this Texas commercial expansion, and the hiring of Claire Harrison to lead it, may influence Huntington’s investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

Huntington Bancshares Investment Narrative Recap

To own Huntington Bancshares, you have to be comfortable with a regional bank leaning into expansion while managing integration and credit quality risk. The push into Austin and central Texas, led by Claire Harrison, reinforces the current growth catalyst of broadening beyond the Midwest, but it also adds to execution and overexpansion risk in the near term. If integration costs and culture alignment in Texas stay under control, the short term narrative is unlikely to change materially.

Among recent announcements, the closure of the Veritex Holdings merger in late 2025 is most relevant here, as it cemented Huntington’s entry into Texas before this Austin build out. Together, the Veritex deal and the new commercial banking push frame Texas as a key test of whether Huntington can scale efficiently in higher growth markets while preserving net margin and earnings quality.

Yet investors should be aware that integration and overexpansion risk in Texas and the Carolinas could...

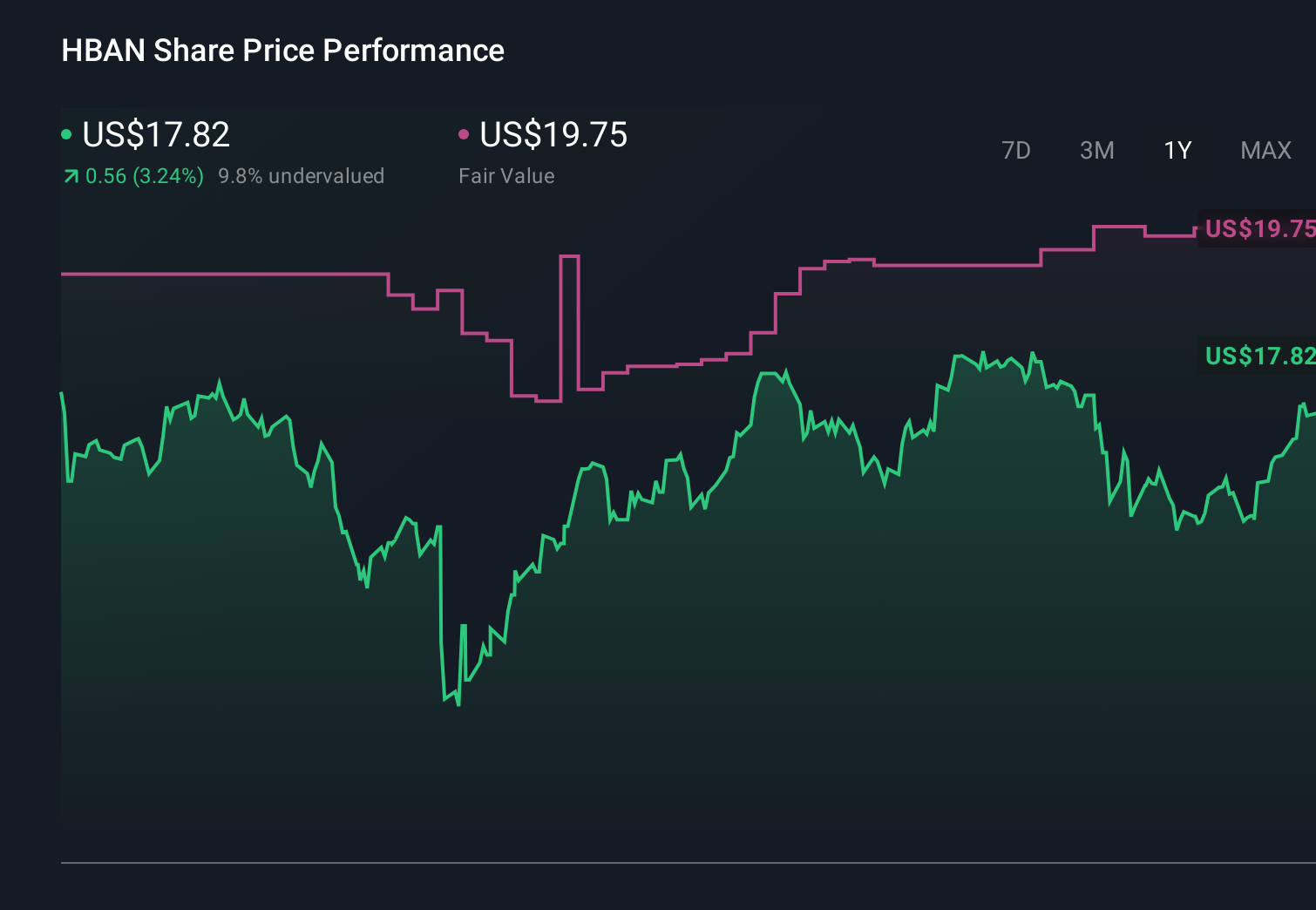

Huntington Bancshares' narrative projects $13.1 billion revenue and $3.7 billion earnings by 2029. This requires 19.6% yearly revenue growth and about a $1.6 billion earnings increase from $2.1 billion today.

Uncover how Huntington Bancshares' forecasts yield a $19.69 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates for Huntington range from US$19.69 to US$35.62, underscoring how widely individual investors can differ. You should weigh those views against the expansion risk that Texas growth and recent acquisitions could raise costs and pressure reported earnings over time, and explore several alternative perspectives before deciding how this fits into your portfolio.

Explore 3 other fair value estimates on Huntington Bancshares - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Huntington Bancshares research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Huntington Bancshares research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Huntington Bancshares' overall financial health at a glance.

Interested In Other Possibilities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Find 58 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.